Emkay Global Financial Services Ltd., for the second time in 10 weeks, has upgraded Petronet LNG Ltd. to "buy" from "add," citing a steady outlook and attractive valuation. The broking has increased its target price for the stock by 16% to Rs 425, implying a potential upside of 23.4% from the current market price of Rs 344.1 apiece.

According to Bloomberg, investors who followed Emkay's recommendation received a 50% return in the past year, the same as the company's performance. Just 10 weeks ago, Emkay Global upgraded Petronet LNG to 'add', during which the stock fell an average 5.8%. It rose 5.2% in the periods rated buy.

Reasoning For Upgrade

Emkay Global upgraded Petronet LNG to "buy" based on a steady outlook and attractive valuation. The brokerage noted that while Dahej terminal utilisation fell from over 110% in the first quarter of fiscal year 2025, it expects utilisation to stay close to 100% for the remainder of the fiscal year.

Additionally, the Kochi terminal is likely to benefit from a ramp-up in supply to Mangalore customers. The commencement of Exxon's second 1.2 million metric tonnes per annum term contract from fiscal year 2026 and the expansion of Dahej's capacity by 5 mmtpa are expected to drive future growth. Emkay increased its fiscal year 2026/27 earnings per share estimates by 7-9%.

Outlook & Valuation

Despite concerns about Dahej tariff adjustments and the renewal of the QatarGas contract in commercial year 2028, Emkay Global remains optimistic about Petronet LNG's long-term outlook. The brokerage highlighted that any tariff adjustments would likely be minor and would not impact minority shareholder interests.

Emkay also sees positive triggers from LNG retail and C2-C3 opportunities. Given the company's contracts and projected growth, Emkay has shifted to a price-to-earnings valuation approach, valuing the stock at 15 times its estimated earnings for September 2026 to arrive at a target price of Rs 425.

Dahej Terminal

Petronet LNG's Dahej terminal saw utilisation above 110% in the first quarter of fiscal year 2025, driven by power sector demand, but Emkay expects the utilisation rate to stabilise around 100% for the remainder of the current fiscal. The Dahej terminal expansion, expected to add 5 mmtpa of capacity, is likely to support continued volume growth.

Exxon Contract

Exxon's second-term contract for 1.2 mmtpa is set to commence in fiscal 2026, contributing to higher utilisation at the Kochi terminal. Emkay expects this to drive a 7-9% increase in earnings-per-share for fiscal year 2026-27, given the higher tariffs associated with Exxon volumes.

Additionally, the brokerage sees value in the stock under reasonably conservative assumptions, even factoring in potential tariff cuts for Kochi and Dahej terminals.

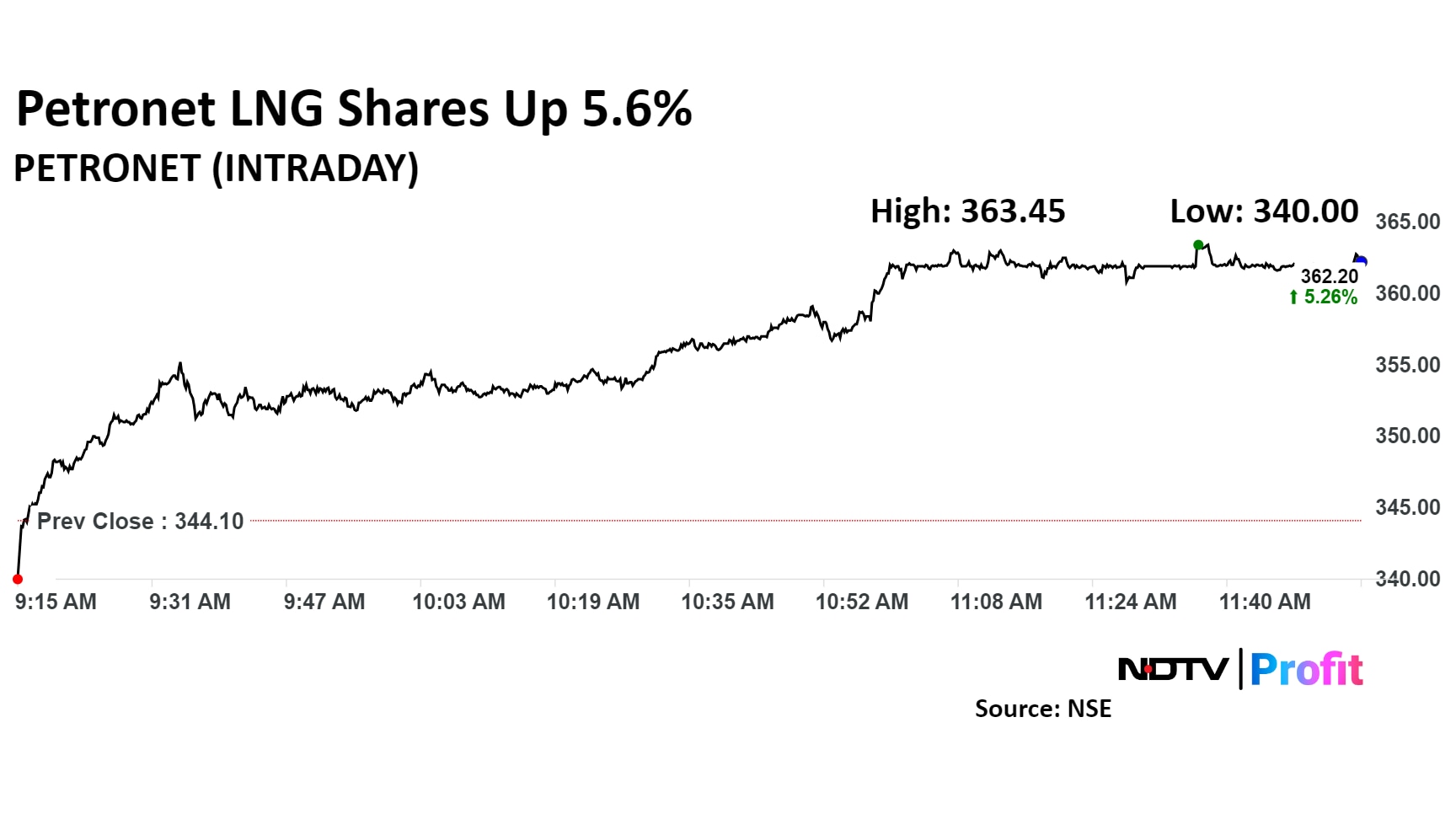

Petronet LNG Shares Today

Shares of Petronet LNG rose as much as 5.62% during the day to Rs 363.45 apiece on the NSE. It was trading 5.17% higher at Rs 361.90 apiece, compared to a 1.56% decline in the benchmark Nifty 50 as of 11:52 a.m.

The stock has risen 51.20% in the last 12 months and 62.54% on a year-to-date basis. The total traded volume so far in the day stood at 6.2 times its 30-day average. The relative strength index was at 63.14.

Eight out of the thirty-five analysts tracking Petronet LNG have a 'buy' rating on the stock, 11 recommend a 'hold' and 16 suggest a 'sell,' according to Bloomberg data. The average of 12-month analyst price targets implies a potential downside of 8.9%.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.