(Bloomberg) -- Global fund giant Loomis Sayles & Co. is turning more positive on China's battered real estate sector, saying recent debt restructuring arrangements are bearing fruit and improved sentiment may result in a faster-than-expected bounceback.

Investors who wait too long may miss out on the rebound, according to Matt Eagan, a fund manager at Boston-based Loomis Sayles, which oversees $303 billion. Fellow asset manager Fidelity International also senses an opportunity, saying history shows investing in the surviving developers of a housing downturn can be very profitable.

Both Loomis Sayles and Fidelity are backing up their views with cold hard cash. Eagan's fund has been buying more bonds of distressed developer Sunac China Holdings Ltd., while one of Fidelity's multi-asset funds managed in Singapore recently added a small position in China state-owned developer shares.

“It's bottomed here but it's still got a long way to go to recover,” Egan said in an interview last month. “Before it was easy to say: ‘I'm not even going to pay attention to it because it's just a one-way bet down,'” but that's no longer the case, he said.

China can't afford a complete meltdown in property markets so officials are going to take further steps to revive the sector, said Eagan, who jointly manages the Loomis Sayles Global Allocation Fund that beat 97% of its peers last year.

Read more: China's Shattered Property Bond Market Finds Hope in Sunac Deal

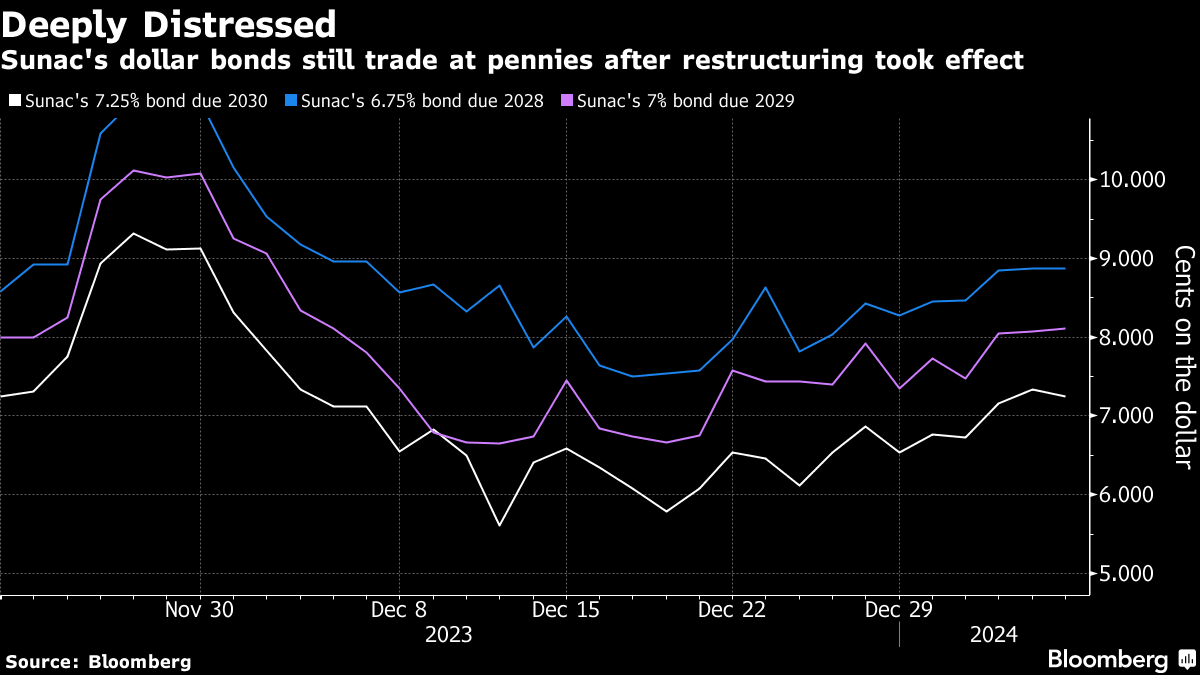

His current top pick is Sunac, which restructured its debt in November after defaulting on its dollar bonds in May 2022. “Sunac is trading at pennies on the dollar after the restructuring,” he said. “There's a danger to not owning that because it could triple or could even go up much higher.”

Another attractive opportunity is Yuzhou Group Holdings Co., which said in late December it's close to reaching an agreement with a group of creditors, he said.

The stocks and bonds of Chinese real estate companies have been pummeled over the past four years due to a toxic cocktail of unsustainable debt levels, slowing long-term economic growth, and spreading disinflation. A Bloomberg index of real estate owners and developer shares has tumbled almost 80% since the end of 2019, while a gauge of high-yield China dollar bonds dominated by developers slumped 45% over the same period.

There have recently been a number of positive signs. This month alone, two major property developers and a large car dealer unveiled repayment plans for maturing debt.

“The surviving firms will end up benefiting from industry consolidation and eventually thrive when the cycle turns, with stock performance typically front-running the upwards turn,” said George Efstathopoulos, a money manager at Fidelity International in Singapore. “State-owned enterprise developers will eventually be well placed to benefit.”

The Fidelity Global Multi Asset Growth & Income Fund holds a number of shares of Chinese developers including Longfor Group Holdings Ltd., China Resources Land Ltd. and China Overseas Land & Investment Ltd., data compiled by Bloomberg show.

There are still plenty of reasons to be wary.

While policymakers have offered up support including easing some mortgage rates to issuing more debt to finance infrastructure projects, the economy remains fragile. The value of new-home sale among the 100 biggest developers slumped about 35% in December from a year earlier.

Bulls argue the debt market is already reflecting all of that bad news. About 35% of the bonds in the ICE BAML China Property High-Yield Index are priced below 30 cents on the dollar, while Chinese developers account for just 5% of Asia's high-yield debt market.

“A lot of the negative views are well priced,” said Julio Callegari, chief investment officer for Asia fixed income at JPMorgan Asset Management in Hong Kong. “Home sales we think we're very close to the bottom here, and it's quite possible that in 2025 we are already in a slightly positive figure.”

More stories like this are available on bloomberg.com

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.