IDBI Bank, a lender that dates back to the days of development finance institutions in the country, has seen more than a quarter of its loan book turn bad. The unabated surge in bad loans has prompted the bank to halt corporate lending and shrink its international presence.

The bank reported a net loss of Rs 5,662.70 crore for the quarter ended March 2018 compared to a net loss of Rs 3,199.70 crore in the same quarter last year. The bank has now reported losses for the sixth consecutive quarter.

- Gross non performing assets at the bank rose to 27.95 percent compared to 24.72 percent at the end of the December quarter.

- Net NPAs rose to 16.69 percent from 16.02 percent in December.

- Slippages during the quarter stood at Rs 12,800 crore.

- Rs 9,800 crore in slippages were on account of the RBI's new stressed asset framework.

- The bank has placed loans worth Rs 14,000 crore under the watchlist for FY19.

- Provisions more than doubled to Rs 10,773 crore compared to Rs 3,637.5 crore at the end of the December quarter. In the March 2017 quarter, the bank had set aside Rs 6,209 crore as provisions.

- The bank took a tax write-back of Rs 2,519.66 crore during the quarter.

The bank's performance may have been worse if it had not used special dispensations permitted by the regulator. IDBI Bank has reduced provisions by Rs 1,496 crore after the RBI allowed banks to reduce mandatory provisions against accounts referred to the NCLT to 40 percent from 50 percent earlier. The bank has also chosen to spread the provision for mark-to-market losses incurred on it bond portfolio.

In addition to the asset quality pain in the current financial year, the bank reported a large divergence in the assessment of NPAs between the lender and the regulator in FY2017. The divergence in gross NPAs stood at Rs 10,281.9 crore or 23 percent of the gross NPAs reported by the bank at the end of March 2017. It also reported a divergence in provisions of Rs 4,464 crore for FY17.

Operational Performance

IDBI Bank has been under the RBI's prompt corrective action framework since May 2017 due to the high level of bad loans and negative return on assets (RoA) reported by the bank. Since then, it has shifted to a ‘capital light' model and focused on retail lending. This has resulted in a reduction in risk weighted assets, said MK Jain, chief executive officer of the bank.

- For the quarter ended March, the bank reported a sharp decline of 44 percent in its net interest income.

- It's advances book showed a de-growth of 10 percent between March 2017 and March 2018

- Net interest margin stood at 1.81 percent in the March quarter

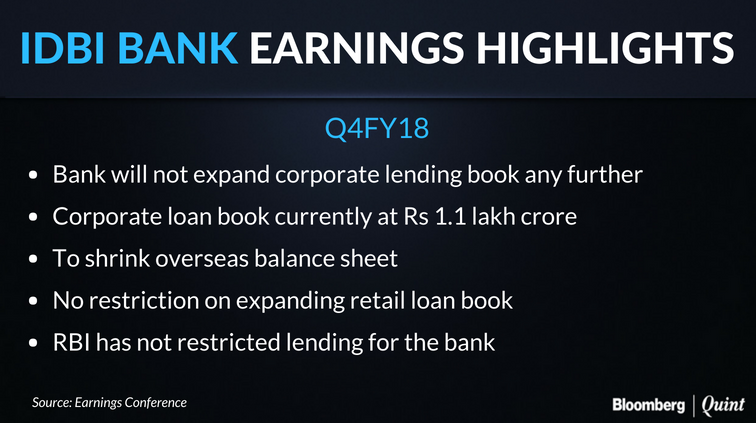

The bank will not expand its corporate loan book for now, said the top management. It will also shrink the international loan book. Even as it focuses on retail lending, the bank has shut 25 loss making branches in FY18 and has identified another 31 for closure. The aim is to convert IDBI into a digital bank, said Jain.

The bank has also tried to release capital through the sale of various non-core assets. The management of IDBI Bank said that such asset sales had helped the bank release close to Rs 4500 crore through financial year 2017-18. More such asset sales would continue, Jain said. In particular, the bank is looking to sell up to 30 percent stake in IDBI Mutual Fund.

Candidate For Stricter Corrective Action?

Given its current financial position, IDBI Bank could face stricter corrective action from the Reserve Bank of India. Under the new PCA framework, weak banks are put in three buckets based on the level of capital adequacy, net NPAs and return on assets (RoA).

While IDBI Bank has the minimum level of regulatory capital, its high net NPAs and consistently negative RoA could prompt the RBI to recommend stricter corrective action on the bank.

IDBI's net NPA ratio puts it in the highest risk threshold. The bank has also reported a negative RoA for three consecutive years. A bank in the third risk threshold could draw restrictions ranging from branch expansion to discretionary actions such as lending restrictions.

Watch this interview with IDBI Bank's MD and CEO MK Jain.

Also read: What Happens When A Bank Stops Lending?

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.