Recently, three very relevant reports for pharmaceutical companies focussing on the US Generics market were published. Two reports, that were from FDA and the US Pharmacopeial Convention respectively, talked about the shortage of drugs in United States in 2023. The third highlighted an interesting statistic—In 2022, Americans filled 6.7 billion prescriptions, and more than 90% of these were for generics. Further, as per the report, US generics market amounts to ~32% of global generics market.

A congregation of the above highlights a crucial unfulfilled demand for generics in the US market, a very important ingredient of overall US healthcare system.

In this article, we explore the US Generics Market—what has led to shortage of drugs, particularly generics, how the industry is set for a turnaround and strategies Indian players can use to take advantage of it.

What Led To Drug Shortages?

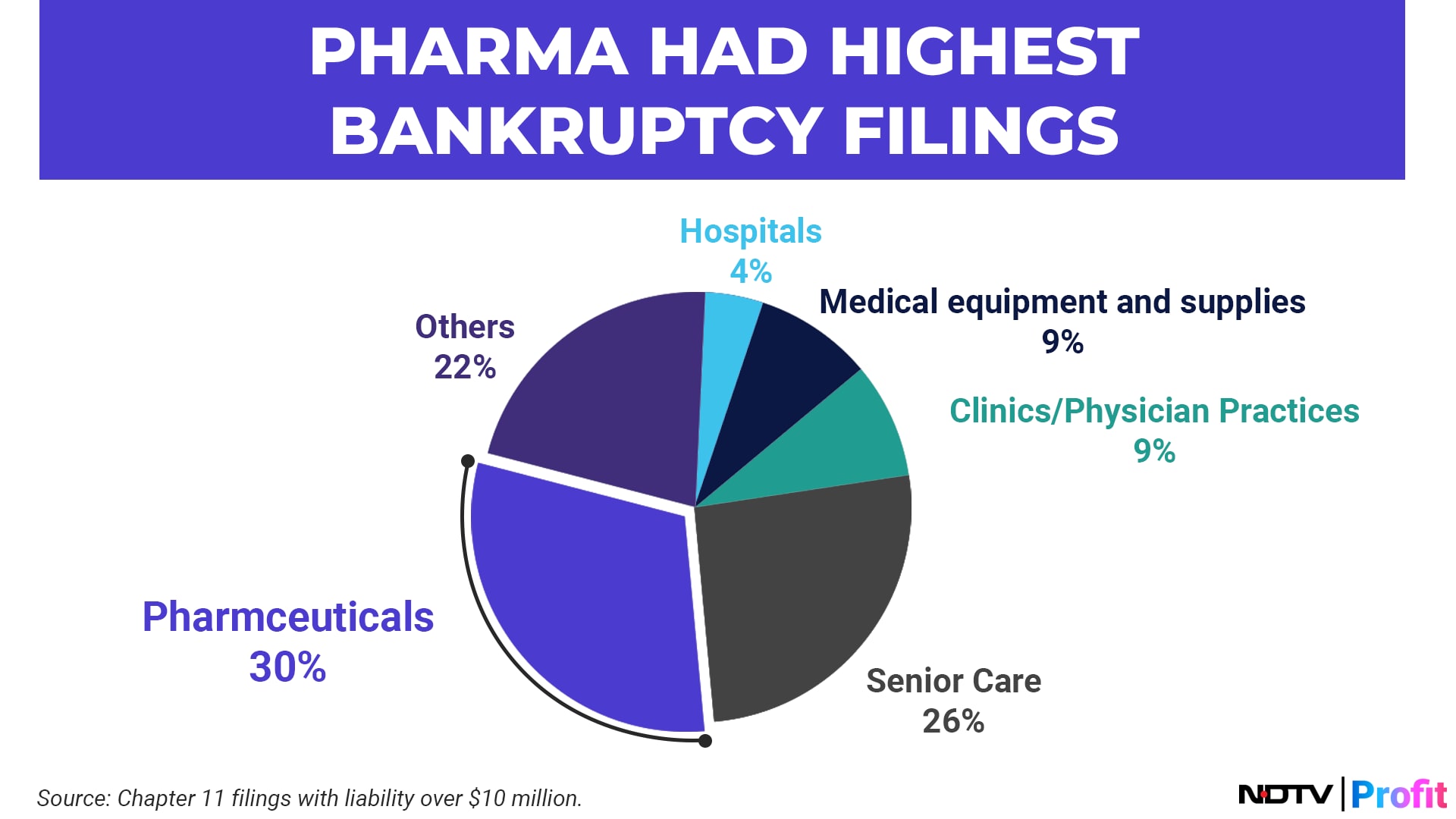

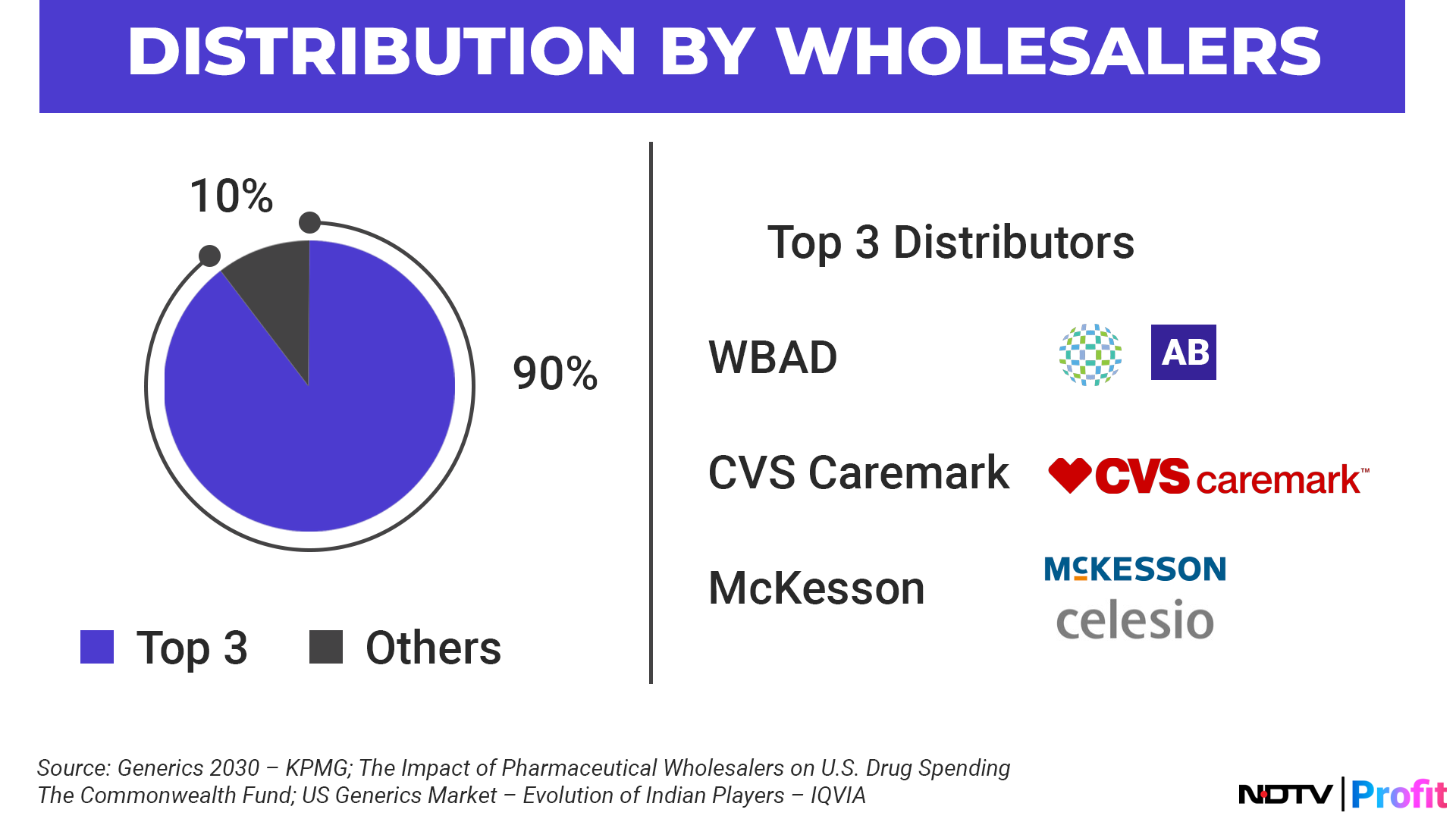

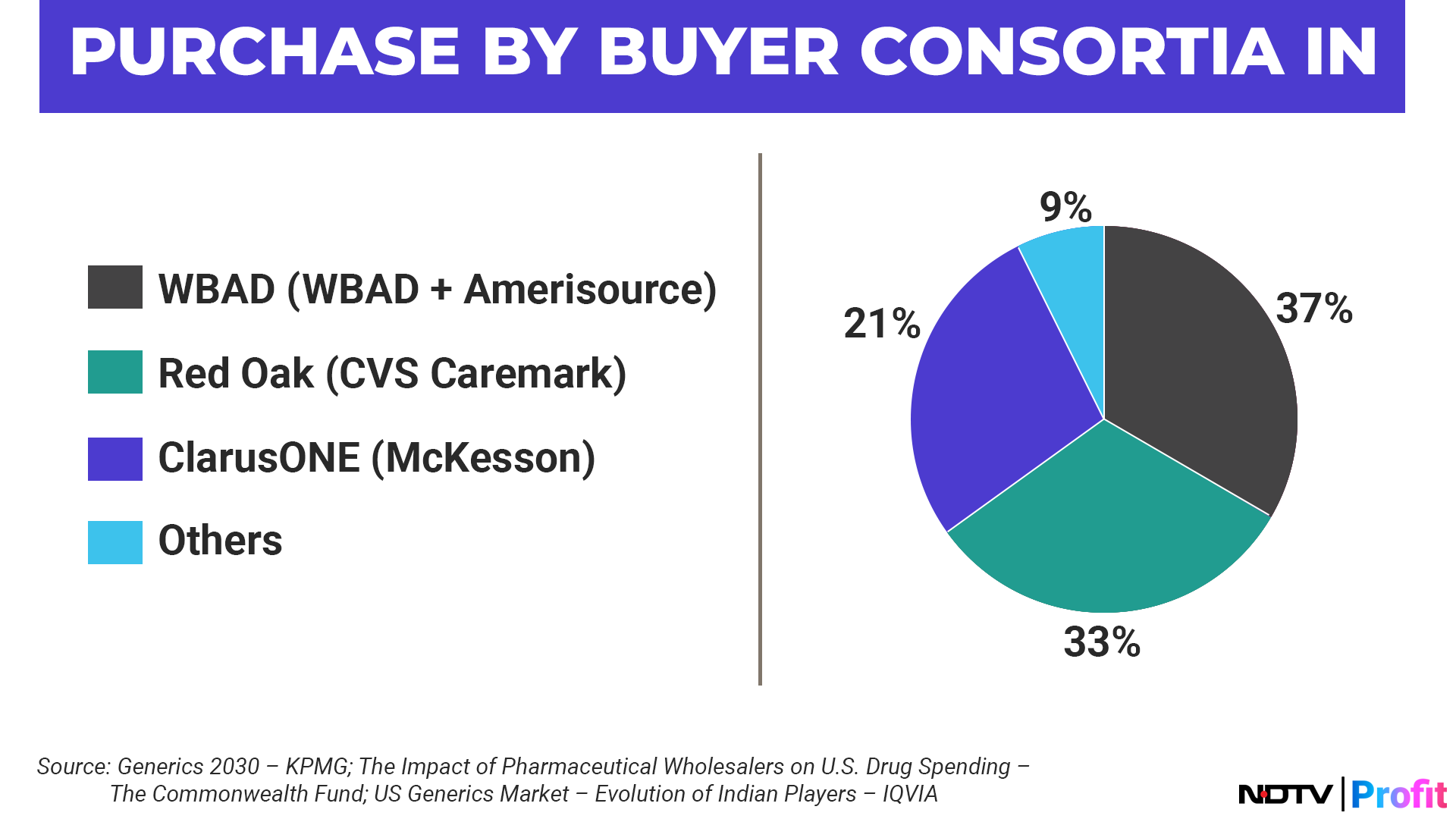

One of the key reasons behind drug shortages is a lack of consistent supply, spurred by an increase in bankruptcy filings amongst the suppliers. Several supplier-side players have been eliminated from the US generics market, resulting in supply distortions, in turn leading to drug shortages.

.png)

Supply side companies have faced multiple headwinds such as rising interest rates, high debt burdens, regulatory issues with the FDA and pricing pressures.

Whereas regulatory burden is part and parcel of this industry, what actually brought the suppliers down was the acute pricing pressure. Drugs were sold at lower price in order to remain competitive, and this constraint of providing price reductions led to constant price erosion for suppliers. Combined with other factors, such as debt burdens and regulatory issues, several supply-side companies became financially unsustainable and filed for bankruptcy.

These bankruptcy filings reduced the number of suppliers and with the Covid-19 pandemic putting further pressure on supply chains, a bottleneck has formed on the supply side.

FIGURES

US Generics Market At Cusp Of Turnaround

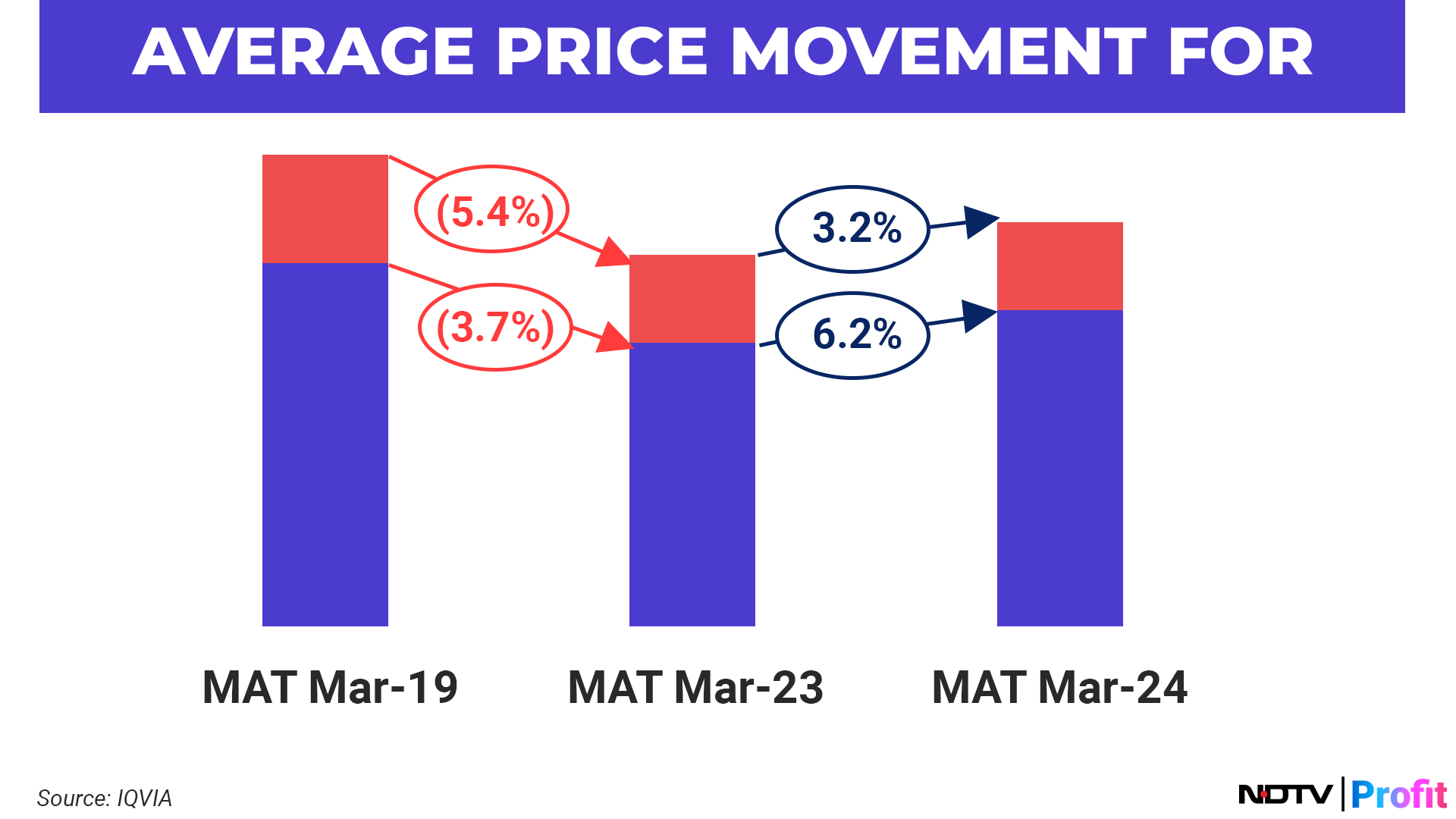

To cater to the unmet demand, demand-side companies have started to prioritise the reliability of supplies over low prices. This shift in focus is evident through the average price movement of generic drugs, which after a steady decline through the years owing to increased consolidation, has seen a general uptick.

There are several macro tailwinds that make the US generics market a favourable proposition for suppliers:

Several bestseller drugs are expected to go off-patent in the US. Thus, increasing the potential for generic alternatives.

The market for specialty generics is poised to grow at 7.7% CAGR till 2027.

FDA has expedited the ANDA approval processes. An ANDA approval helps companies to sell generic medicines in the US.

Several government authorities in the US have increasingly questioned the supply chain issues and have asked relevant stakeholders to resolve the bottlenecks.

Amidst the favourable tailwinds, Indian players are in a strong position to take advantage of them:

The top five Indian companies taken together have more than 10% of the generics market share. Moreover, Indian ANDA approvals accounted for 47.1% of the total ANDA approvals in 2023.

Indian generic drugs are responsible for $1.3 trillion in savings for US customers. Thus, helping the companies earn a favorable outlook toward them from them.

Indian companies play a crucial role in the supply of affordable generic drugs, with 47% of generic prescriptions being supplied by them. Specially for some therapy areas such as mental health, Indian players' share in prescriptions is at 62%.

With favourable tailwinds and a strong positioning, Indian players need the right approach to take advantage of them.

Indian Players' Right-To-Win

There are three different approaches that can help/have helped companies succeed in US Generics market, that is, backward integration to APIs, front-end US presence and focus on innovation.

Backward Integration

Companies can integrate backwards to include key molecules production to shield themselves from pricing pressure. Such an approach helps companies to have better control over their pricing and availability by removing the dependency on players they source from. Integrating with low-cost Indian API production players provides such an avenue for companies to boost their margin profile.

One such company is Kalintis Healthcare, US-focused niche and complex APIs and intermediates player, who have their own 300 MT API manufacturing facility in Baroda. With five commercial APIs in the US (with seven more in the pipeline), they have stronger ability to withstand any undue pricing pressure.

Front-End US Presence

Companies, in order to regain healthy bargaining power, have integrated forward into distribution by either acquiring a distributor or building in-house distribution capabilities that allow them to capture additional revenue along the value chain.

An example of such a company is Rubicon Research. A complex generics player, it has focused on creating its front-end distribution channel with US FDA and UK MHRA approvals and research and development centres in India and Canada.

Focus On Innovation

Some players in the industry have invested in R&D to differentiate themselves from the competition and mitigate price pressure. Focusing on modifying the strength, indication, or route of administration of an off-patent drug have been some of the focus areas. Other areas of innovation include developing complex generic capabilities.

One Indian player that has focussed on innovation is Apothecon Pharmaceuticals. They have an API manufacturing facility in India with US FDA, UK MHRA and ANVISA approvals and possessing strong R&D capabilities with 15 molecules in pipeline.

Summary

US Generics market offers a great opportunity, and Indian players must respond to it. The past few years have seen players on the demand side getting consolidated and thus getting the bigger share of bargaining power. Though lack of supply has led the demand-side companies to recalibrate their strategy, inclusion of supply assurance in their decision criteria has gradually led to improved pricing for pharma players, which they can further build on by integrating across the supply chain and focusing on innovation.

Shiraz Bugwadia is senior managing director at O3 Capital and focuses on the firm's life sciences and healthcare practices. He has more than 23 years of experience.

Prasanna Bora is a managing director at O3 Capital and focuses on the firm's life sciences practice. He has more than 18 years of experience.

The views expressed here are those of the author, and do not necessarily represent the views of NDTV Profit or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.