(Bloomberg Opinion) --Two weeks after a robotaxi event that failed to inspire, Tesla re-pivoted rather more successfully — back to the car business. And yet Wednesday evening's earnings call echoed the vagueness and confusion that marked that earlier event. Altogether, it tees up a high-stakes fourth quarter and, more importantly, 2025.

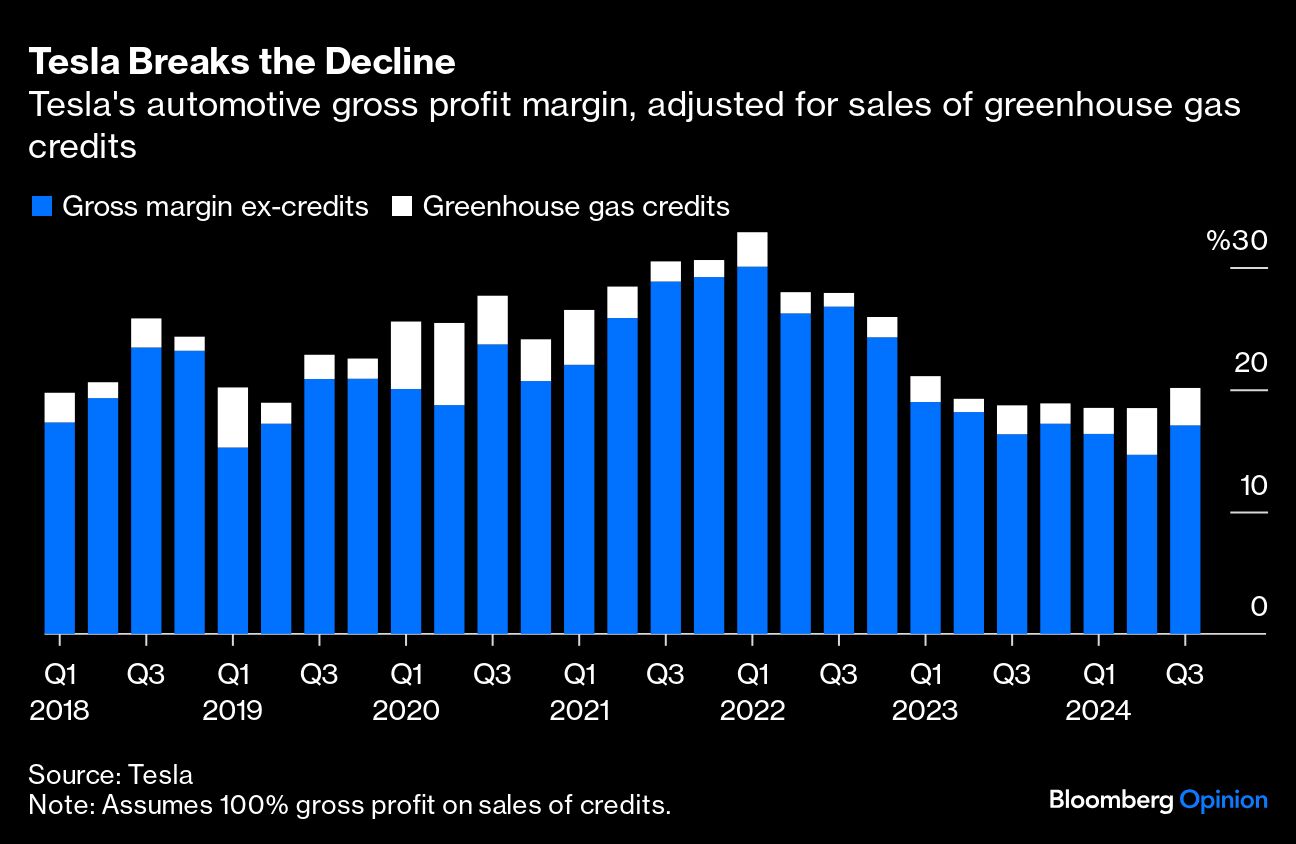

Tesla beat the consensus earnings estimate for the first time in five quarters, albeit an estimate that has roughly halved over the past year. The closely watched gross profit margin for its automotive business, less the impact of selling greenhouse gas credits, halted its slide and ticked back up to its highest level since the end of last year. Free cash flow, meanwhile, was $2.74 billion, the highest in two years. The company also struck a bullish note on vehicle sales, saying it expects to post a “slight” increase in 2024 versus 2023 — in contrast to the current consensus forecast for a decline — implying it will shift more than half a million in a quarter for the first time ever.

Some caveats. Tesla mentioned, without quantifying, the impact of recognizing deferred revenue on its Full Self Driving product, a wildcard for the automotive margin. Moreover, sales of greenhouse gas credits were the second-highest ever, after the prior quarter; indeed, sales through the first three quarters are already higher than for the entirety of 2023. The blowout free cash flow certainly benefited from higher earnings, but almost 60% of it came from ballooning accounts payable — deferred bills, essentially.

The forecast for higher vehicle sales in 2024 is something of a double-edged sword. Tesla was still building inventory in the third quarter and is offering zero-percent financing in the US, potentially meaning a reversal on margins this quarter.

Strikingly, Chief Executive Elon Musk doubled down on the growth theme, throwing out a figure of 20%-30% for vehicle deliveries in 2025, well ahead of the consensus forecast. This will presumably be fueled by “new vehicles, including more affordable models” that the company says will begin production in the first half of next year.

Tesla's valuation duly jumped by around 12% after market, worth a notional extra $80 billion — two Ford Motor Co.'s, give or take — erasing the drop after the robotaxi event disappointed. Which is odd, to say the least.

Investors took fright two weeks ago because, after months of build-up, Tesla revealed few real details about a robotaxi strategy that is central to its valuation and was supposed to step in for a cheap EV strategy that unraveled at the start of the year. Now, investors are seemingly jazzed about a better-than-expected performance in the core EV business, with the caveats noted above, and new growth targets. The latter is predicated on “affordable models” that, mere months away from when they are supposed to be launched, we are yet to see.

Meanwhile, Musk reiterated the messaging about cybercabs in 2026, unsupervised FSD vehicles in Texas and California next year (regulators permitting, you understand) and the Optimus robot that he gave, to widespread disappointment, two weeks ago. The one notable thing he added was that he felt there should be federal approval for autonomous vehicles and that “if there's a department of government efficiency, I'll try to make that happen” — teasing how victory for a certain presidential campaign into which he is pouring millions might benefit his interests (see this).

In other words, the only real addition to the narrative is that the EV business, which isn't the main pillar of Tesla's valuation anyway, reversed its margin decline for one quarter and, according to another of Musk's don't-quote-me projections, might notch decent growth next year.

Over the past two years or so, we have seen Tesla's stock generally trend downward from the bubble of 2021. Gathering evidence of a slowdown in EV sales, and falling margins — plus Musk's own selling in 2022 — have fueled repeated sell offs, only for Musk's increasingly AI-inflected visions and targets to re-fortify animal spirits.

While it's curious that Wednesday's revival rested mostly on EVs, it does set up an interesting near-term test for Tesla. Musk has now pledged new (if unseen) models, a big reacceleration in EV sales growth and actual self-driving cars in at least one state, all within roughly the next 9-12 months. The narrative continues to be rolled forward but Tesla is nearing multiple, and verifiable, deadlines at speed.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.