Bond markets were in a sulk on Tuesday. Quite literally so. The evening before, at the annual dinner of the Fixed Income, Money Market and Derivatives Association (FIMMDA), Reserve Bank of India Deputy Governor Viral Acharya had read out the riot act to the country's top treasury managers. The press was not invited but the tone and tenor of the speech (put out on the central bank's website) suggested that Acharya was in no mood for pleasantries.

Before we get into what Acharya had to say, let's remind you of the context.

The bond markets have been whiplashed time and again over the last 14 odd months.

First, demonetisation sent yields tumbling. Then an unanticipated change in the central bank's monetary policy stance sent yields soaring. But inflation underperformed the central bank's expectations and yields slipped again. It wasn't to last. Inflation picked up. The government's finances looked shaky. Yields soared again. The end result is that yields on the 6.79 percent 2027 bond (the old 10-year benchmark) are up more than 100 basis points in the last one year. Even the new 10-year bond yield (which was issued at a coupon of 7.17 percent) has moved up 20 basis points in less than 2 weeks. Yields fell on Wednesday after the government decided to cut the quantum of additional borrowings for the year.

All this volatility has led bankers to suggest that the RBI should allow them to spread out mark-to-market losses on their treasury portfolio over two quarters. Perhaps it was this suggestion (reported by Business Standard on Jan. 6) which irked Deputy Governor Acharya.

“Interest rate risk of banks cannot be managed over and over again by their regulator,” Acharya said in his speech at the FIMMDA dinner. The trend of seeking regulatory dispensation is not desirable either from the point of view of effective price discovery or market discipline, Acharya added.

Acharya didn't stop there. He went on to lay out a list of practices that banks should adopt to manage treasury risk.

- Bank boards should discuss and approve risk strategy.

- Banks should conduct stress tests on treasury portfolio.

- Banks should adopt robust risk controls, dynamic stop loss limits.

Stuff of basic hygiene that, one assumes, banks do in any case. But apparently Acharya believes they don't.

Acharya also pointed out that India has, on paper, the best government securities market infrastructure in the world. Yet banks and their treasury managers appear to follow ‘hope' as their primary trading strategy, Acharya said.

Is Acharya's criticism justified? And are banks entirely at fault? Yes and No.

As Acharya explained, the value of a bond investment portfolio is a factor of the size of the portfolio, the duration of the portfolio and the increase in yields. The first point to note is that the investment portfolio of government securities held by banks has increased over the last three years. Weak demand for credit and bouts of surplus liquidity have pushed banks to park funds in government securities. Also, since the RBI has limited the amount of funds that can be parked at the central bank's reverse repo window, banks have few options but to buy government securities.

According to RBI data, 82 percent of the total investment pool of banks was parked in government securities as of 2016-17. For public sector banks, this proportion was even higher at 84 percent.

“As a result, the size of banking sector's balance-sheet exposure to G-Secs, and hence, its interest rate risk, is high in an absolute sense, and is relatively elevated,” said Acharya.

While banks may not have much control over this high exposure to government bonds and interest rate risk, the question is whether they can manage it better. Here, Acharya's contention is that they can.

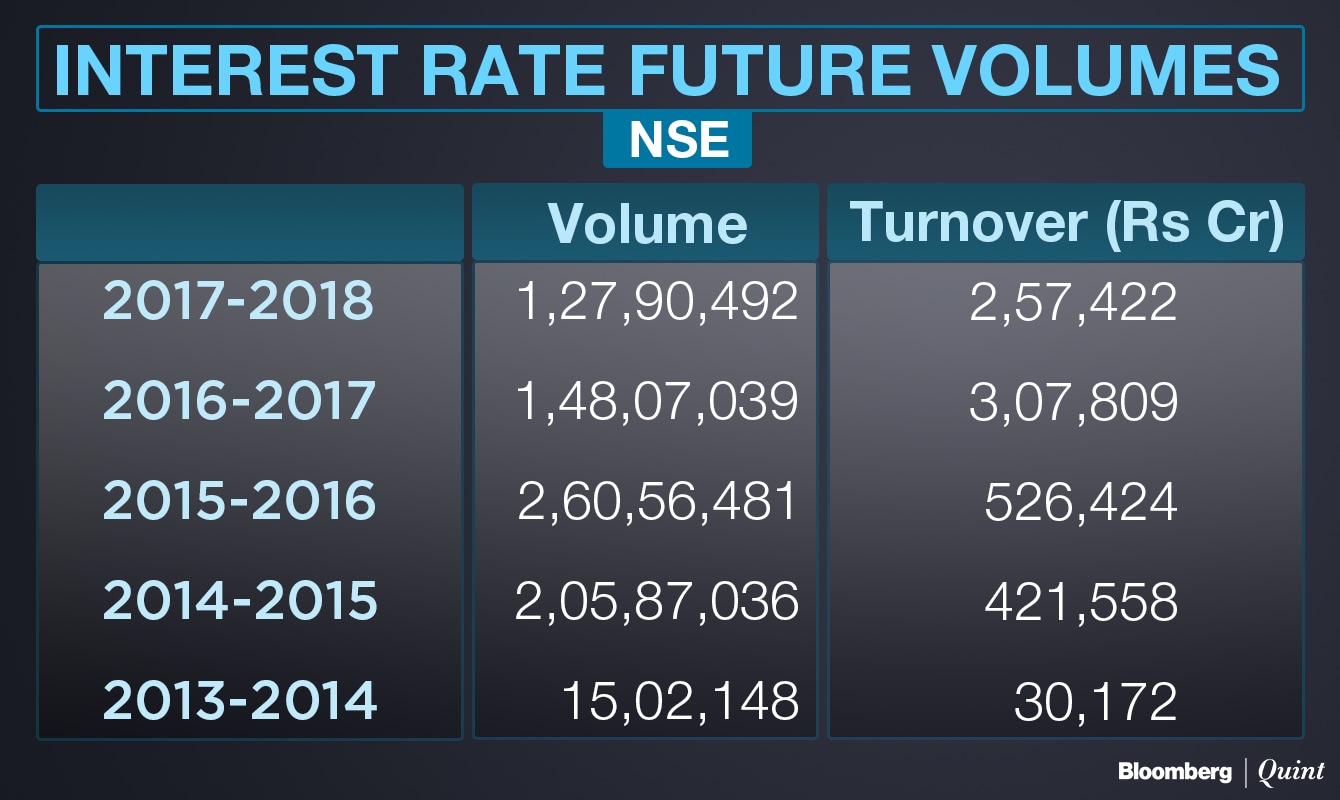

His view may be justified. For instance, if you look at the interest rate futures market, which is one route to manage risk, banks have done little to increase their participation in this market. Data from the National Stock Exchange, which is dominant in the bond futures segment, shows that volumes have only declined over the past few years. This, despite the fact, that interest rate futures were relaunched for a third time in 2014.

There is no liquidity in the interest rate futures market, said Lakshmi Iyer, head of fixed income at Kotak Mahindra Asset Management. Iyer noted that not enough banks are participating in the segment, which is essential to creating liquidity.

The lack of interest and liquidity in the interest rate futures market is a consequence of the fact that the market has few ‘traders' and mostly ‘investors', added Soumyajit Niyogi, associate director at India Ratings & Research. The absence of pure trading interest is not letting the market develop, Niyogi said while adding that the prevailing interest rate environment has also played a role.

“You have to remember that since 2015, until recently, we were in a secular bull market with yields coming down from 8.5 percent to 6.5 percent. In this scenario, everyone had the same view and there were few taking the opposing position,” said Niyogi while adding that volumes may pick up now that the direction of interest rates is at the cusp of turning.

Will that alone be enough to ensure that banks manage their interest rate risk better? Unlikely.

A veteran banker who ran treasury operations for a large public sector bank said that its unfair to say that banks don't manage their treasury risk based on a recent request from lenders that they be allowed to spread mark to market losses over two quarters. Speaking on the condition of anonymity, the former bankers said that the current bout of treasury losses are a consequence of abrupt policy changes that banks had nothing to do with. He pointed to sharp movements in yields following the government's decision to first raise borrowings and then cut borrowings. You will rarely see much yield movements in developed markets, this banker said.

When the whole system is bleeding, the regulator has to understand what the systemic issues are and show some empathy, said this banker.

Ira Dugal is Editor - Banking, Finance & Economy at BloombergQuint.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.