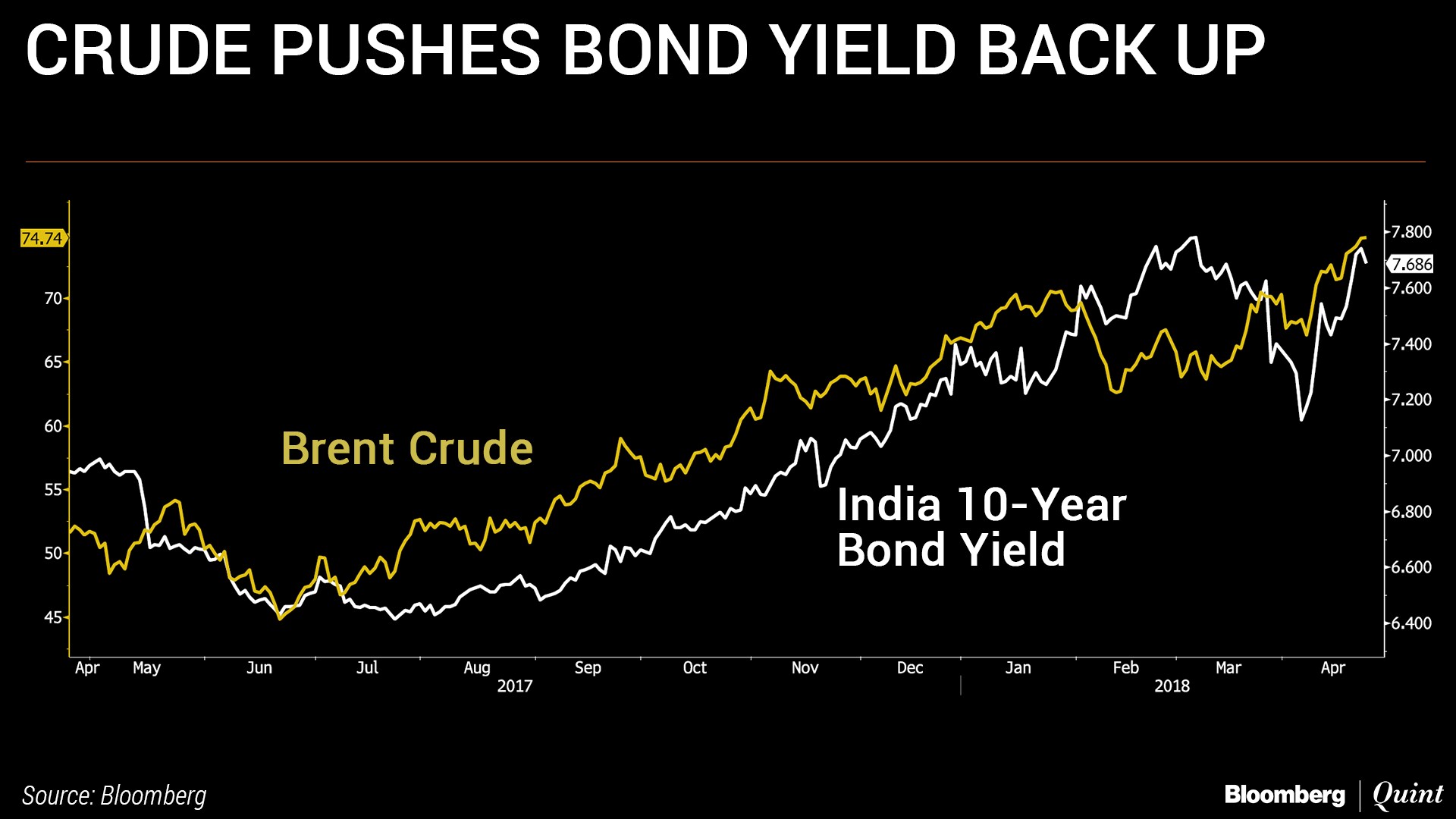

Prices of petroleum products in India are at multi-year highs. In the case of petrol, prices are at their highest in four years. For diesel, now decontrolled, prices are at a record high. Apart from rising global oil prices (Brent crude has hit $75 per barrel), high taxes on petroleum products are feeding into this rise in retail prices.

Earlier this month, Bloomberg News reported that the government has ruled out a cut in excise duties on petroleum products due to pressure on government finances, despite concerns of an increased burden on consumers.

Not unlike the past, higher oil prices present Indian policymakers with tough choices. The government needs to protect its finances, particularly a year after it missed the budgeted fiscal deficit target. But it also needs to be mindful of a rise in inflation, particularly since India is now a flexible inflation targeting economy.

Let's consider government finances first. Between 2014 and 2016, the government raised excise duties on petroleum products a number of times leading to an increase in collections from this one source. According to newswire PTI, this helped the government double its excise mop up to more than Rs 2,42,000 crore in 2016-17 from Rs 99,000 crore in 2014-15.

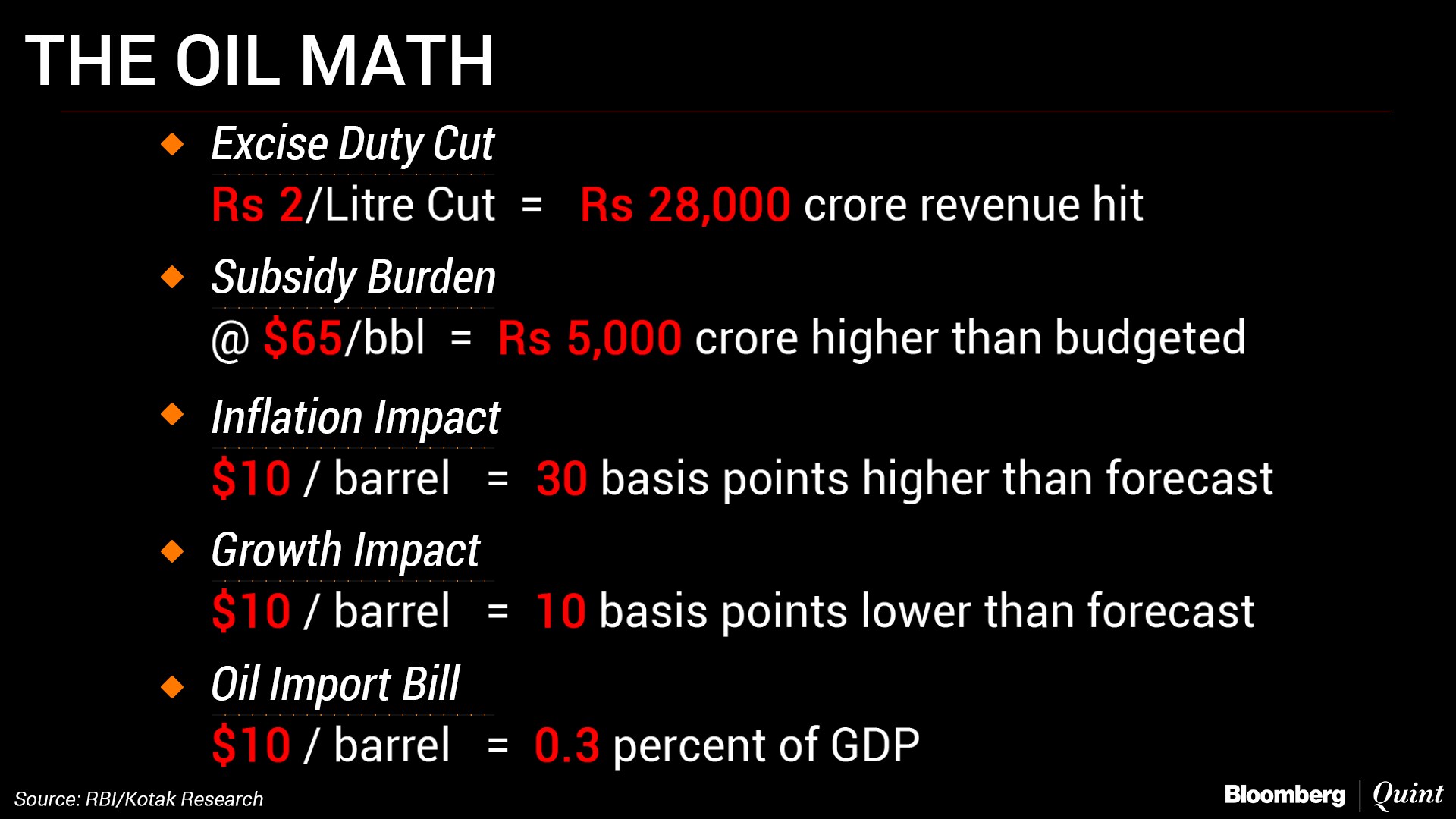

In October 2017, the government cut excise duty by Rs 2 per litre, costing it Rs 26,000 crore in annual revenue. A similar cut now would cost the government Rs 28,000 crore in revenue, said Kotak Economic Research in a report earlier this week.

Unless balanced out, this would mean a slippage of 0.1 percent in the fiscal deficit, which is targeted at 3.3 percent of GDP in 2018-19.

Should the government cut excise duties now, it would be doing so without any great comfort that volatility in government revenues induced by the implementation of GST has settled. As such, it may have to contend with increased nervousness in the bond markets, where yields have already risen and reversed an earlier drop on the promise of lower government borrowings.

The rise in oil prices would also mean a higher subsidy outgo on products like Kerosene and LPG, which are not completely deregulated. The government has budgeted for oil subsidies of Rs 25,000 crore in 2018-19, similar to last year. Some economists believe they have under-budgeted for oil subsidies. At an average crude price of $65 per barrel, the subsidy burden would be Rs 5,000 crore higher than estimated, estimates Kotak Economic Research.

A higher oil subsidy bill and lower revenues from taxes from petroleum products would be a double whammy for the budget.

With the Centre's own finances not at their strongest, the government may be tempted to push states again—at least the ones ruled by the Bharatiya Janata Party— into cutting local taxes on petroleum products. In the weeks following the excise duty cut in October, only four states had followed through with a cut in the state-levied value added tax on auto fuels.

Value added taxes on petroleum products account for nearly 15 percent of the states' self-collected tax revenues, according to an estimate by HSBC Global Research. As prices rise, the collections from this source rise. A 15 percent year-on-year increase in oil prices in FY19 is likely to raise state oil tax revenues by 0.13 percent of GDP, HSBC estimates. States are unlikely to give up on this revenue willingly, even as the Centre tries and protects its own sources of funding.

Choosing to stay focused on managing finances, while laudable, will have a fallout in the form of higher inflation and possibly higher interest rates. It may also eat into growth, which is just recovering.

The RBI is currently estimating CPI inflation between 4.4-5.1 percent during the course of the fiscal year, with higher inflation expected in the first half. For this estimate, the RBI has assumed an average oil price of $68 per barrel. If global prices remain elevated at an average of $78 per barrel, inflation could be higher by 30 basis points, the RBI estimated in its monetary policy report released in April. Unregulated petroleum products form 3.7 percent of the consumer price inflation basket. Higher oil prices impact the index directly but also indirectly by raising transportation costs, which feed into the final price of a range of goods.

The RBI also noted that growth could be lower by 10 basis points compared to its estimate of 7.4 percent in 2018-19, should oil prices average $78 per barrel.

Despite the growth impact, the Monetary Policy Committee may choose to focus on inflation, which remains above the mid-point of its target of 4 (+/- 2) percent. One of the six committee members has already voted for a rate hike and a second is likely to vote for ‘withdrawal of accommodation', showed minutes of the last MPC meet.

While there may be some trade-off between the oil impact on government finances and on inflation, there is no getting away from the hit to India's external finances due to higher oil prices.

India's net oil import bill increases by over 0.3 percent of GDP with every $10 per barrel increase in prices, putting pressure on the trade deficit.

Coming at a time when portfolio flows are sluggish, a rising oil import bill will lead to a deterioration in India's balance of payments position and, hence, weakness in the rupee. The weaker rupee will, in turn, feed back into inflation due to the higher cost of imported goods.

So should the government opt to compromise on its finances to help soften the inflation blow from higher oil? Or should it reinforce the belief that it is a fiscally prudent administration? After four years of calm, the age old policy dilemmas that India faces in times of high oil prices are back to haunt the nation and its government.

Ira Dugal is Editor - Banking, Finance & Economy at BloombergQuint.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.