(Bloomberg) -- Treasury yields surged after stronger-than-anticipated January employment data strengthened the case for the Federal Reserve to defer cutting interest rates until at least the second quarter.

Short-dated Treasuries, more sensitive to monetary policy shifts, led the move, with two- to five-year yields rising 20 basis points. The 10-year rose as much as 17 basis points. Yields remained just shy of their session highs late in New York trading, with those for two- and 10-year tenors poised for their steepest daily climbs since March and May respectively. The dollar strengthened.

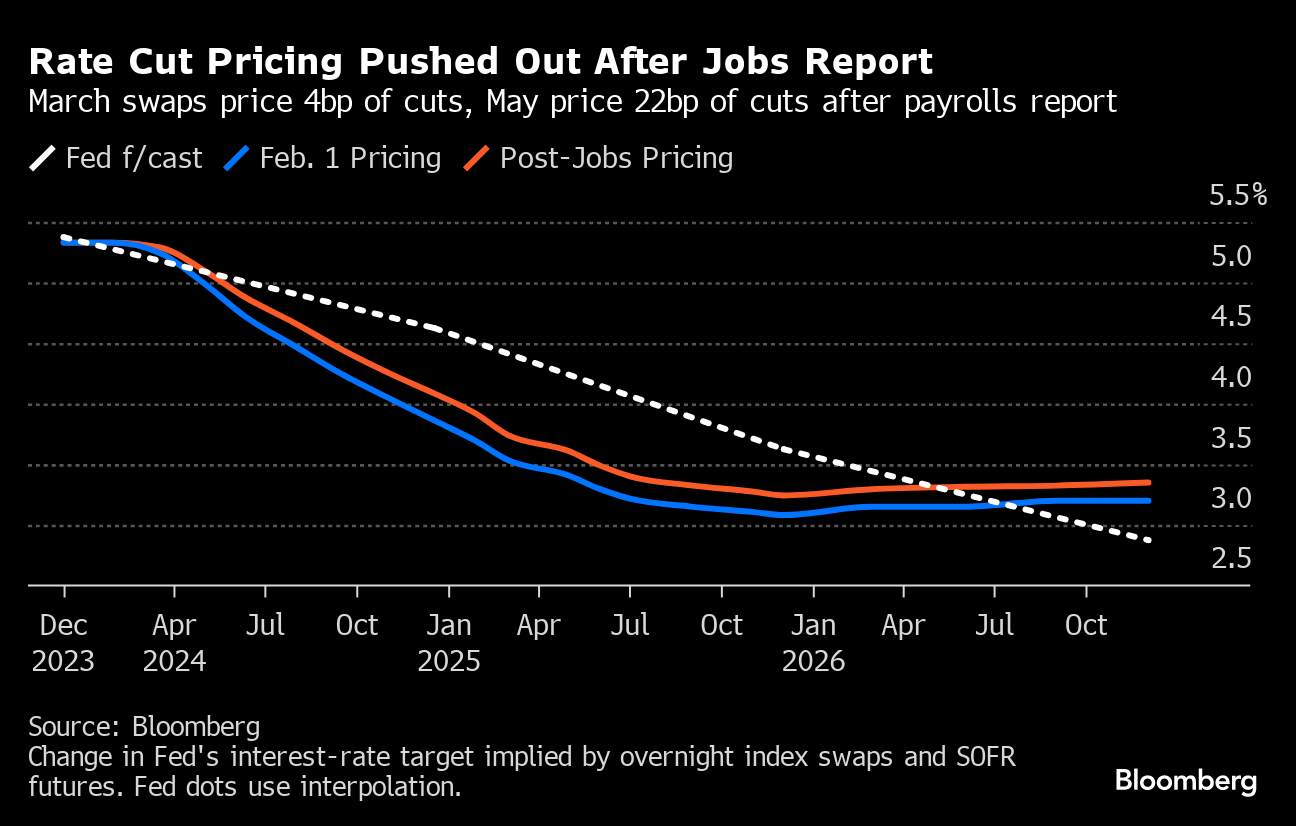

Swap contracts referencing the March Fed meeting date cut the odds of a quarter-point rate cut in half, to about 15%, while the May contract no longer fully priced in a cut, which it had for more than a month. The jobs report included an increase in nonfarm payrolls nearly double the median estimate in Bloomberg's survey of economists and much stronger-than-expected wage growth.

“This means March is off the table,” Mohamed El-Erian, president of Queens' College, Cambridge, and a Bloomberg Opinion columnist, said Friday in an interview on Bloomberg Television. Investors are “more likely to get the three cuts” that the Fed has been signaling, fewer than traders have been pricing in.

Declines in US inflation — the Fed's objective in raising interest rates 11 times over the past two years — have led investors to expect rate cuts this year, even as the labor market has remained strong. Indications that high rates are restraining some types of economic activity and policy makers' own forecasts in December reinforced the expectation.

Cuts beginning in March was considered likelier than not, with several major Wall Street banks forecasting it, until around mid-January, when Fed Governor Christopher Waller said the central bank had no reason “to move as quickly or cut as rapidly as in the past.”

The January employment data highlight the other main risk the Fed is trying to manage — that inflation will stall at unacceptably high levels.

“You have to ask yourself if this is a game changer,” said Glen Capelo, a managing director at Mischler Financial. “Should the Fed be still talking about tightening as opposed to cuts is going to be the question now.”

The odds of rate cuts beginning in March have taken center stage over the past week — zooming back and forth between about one-in-three to two-in-three in response to economic data, declines in US bank stocks and comments by Fed Chair Jerome Powell.

A strong gauge of December job openings on Tuesday left the market pricing in only about a third of a March rate cut. It briefly came back into favor the next day after a measure of January private-sector payroll growth fell short of expectations and regional bank shares fell. Then, Powell in comments after the latest Fed policy meeting said he considered a March rate cut unlikely at this point, and the market-implied odds fell back toward their lows.

Price action in bank stocks, especially regional banks, which are reckoning with losses on loans linked to US commercial real estate, reemerged this week as an intraday driver of Treasury yields. For bond investors it's reminiscent of last March, when several regional banks failed and the Treasury market became the beneficiary of demand for havens.

The KBW Regional Banking Index rose Friday for the first day in four, leaving one less impediment to a bond selloff.

The bond market still expects rate cuts to begin later this year. Powell in Wednesday's comments said policy makers were mindful of the risk of keeping rates at their current 20-year high for too long, and were encouraged by the progress on inflation.

The December swap contract priced in about 125 basis points of rate cuts this year, about 20 basis points fewer than before the jobs data.

“Whether the Fed goes in March or May, the pivot has happened and monetary policy will be wind at the sails of fixed-income investors in this strong economic environment,” said Lindsay Rosner, head of multi-sector fixed income investing at Goldman Sachs Asset Management.

--With assistance from Edward Bolingbroke and Elizabeth Stanton.

(Updates yield levels second paragraph)

More stories like this are available on bloomberg.com

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.