(Bloomberg) -- Just a day before the Federal Reserve decision, a hotter-than-estimated reading on the labor market spurred a slide in bonds, with traders dialing back their projections for interest-rate cuts.

Treasuries dropped across the US curve after a report known as JOLTS showed US job openings unexpectedly rose to a three-month high. Fed swaps trimmed the odds of a March rate reduction to 35%. Stocks lost steam after hitting another record as investors awaited results from two of the tech behemoths that have powered the rally from the bottom amid the artificial-intelligence excitement: Microsoft Corp. and Alphabet Inc.

“The job market holds the keys to future Fed policy,” said Jeffrey Roach at LPL Financial. “In addition to the solid job market, uncertainty over the impact from Red Sea shipping disruption adds pressure to the Fed as they prepare markets for rate cuts.”

Treasury two-year yields rose six basis points to 4.38%. The S&P 500 edged lower. As the earnings season rolls in, traders are also wading through results from an economic barometer — United Parcel Service Inc. — which tumbled on a disappointing guidance. The courier also plans to cut 12,000 jobs.

Besides Microsoft and Alphabet, three other big tech companies with a combined market value of more than $10 trillion report results this week.

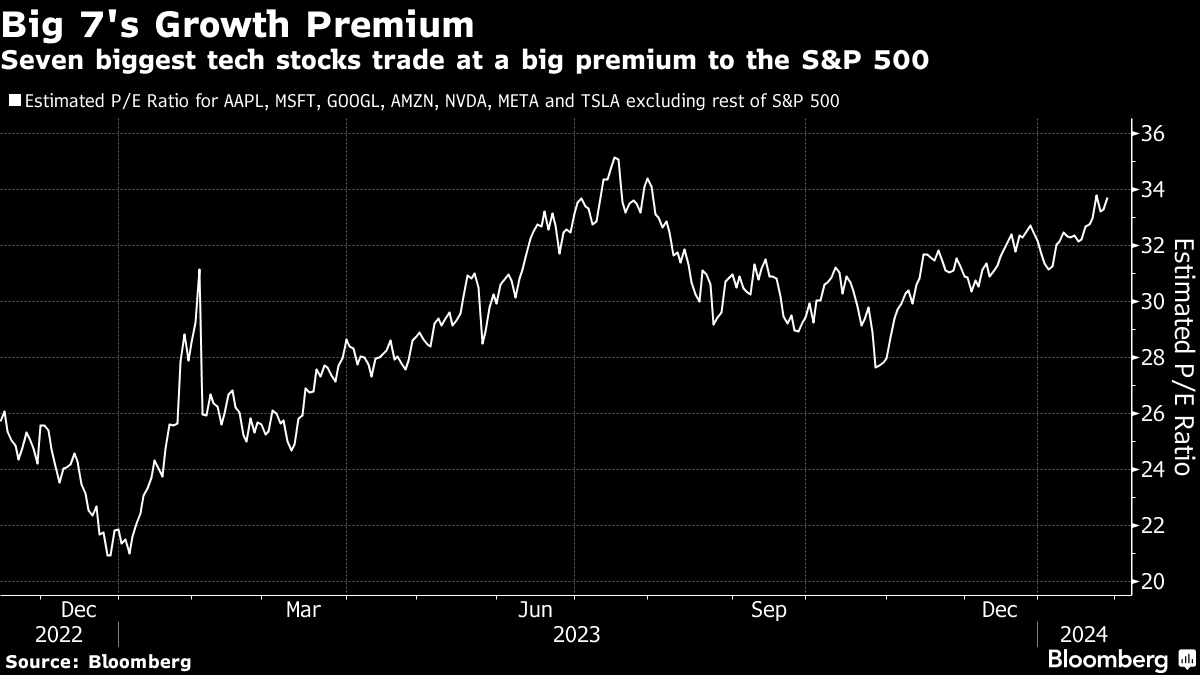

Those firms, along with the other members of the so-called Magnificent Seven growth companies in the S&P 500, carry a nearly 34% premium to the index in terms of forward price-to-earnings, according to data compiled by Bloomberg.

Recent trading has shown that big tech continued to drive the market, with the heavy concentration being cited by some as a warning flag. The dominance of the 10 biggest stocks is increasingly drawing similarities with the dot-com bubble, raising the risk of a selloff, according to JPMorgan Chase & Co. quantitative strategists.

“If we don't get any shockingly negative news from the large-cap tech earnings this week and (especially) if the Fed sticks with its current (much more) dovish rhetoric, it's going to give investors the kind of green light that could push the stock market higher into February —just like the market rallied strongly into February in 2020,” said Matt Maley at Miller Tabak + Co.

Stocks and bonds finished higher on Monday, with the Treasury surprising several traders after cutting its quarterly borrowing estimate to $760 billion. The move helped ease some of the supply concerns ahead of Wednesday's quarterly refunding announcement, with traders shifting their attention to the latest economic readings ahead of the Fed decision.

“We expect Wednesday's Federal Reserve meeting to be much ado about nothing,” said Jerry Klein at Treasury Partners, “The Fed is not quite ready to start cutting interest rates, since inflation has only very recently started to decelerate towards the Fed's target, and the central bank also wants to squash any risk of a reacceleration of inflation, which remains a possibility.”

Klein says that while it's tempting to purchase bonds with shorter maturities of three months or oneyear — given their high yields— investors will face reinvestment risk once the Fed starts cutting rates, where proceeds from these short-term bonds are reinvested at lower yields.

“It's prudent for investors to lock in yields that still remain well above what has been available for most of the past 20 years,” he noted.

Corporate Highlights:

- Whirlpool Corp., the owner of the Maytag and KitchenAid brands, projects 2024 sales will be weaker than Wall Street expectations as consumers forgo appliance upgrades.

- Boeing Co. withdrew a request for a key safety exemption that would have helped speed approval of its coming 737 Max 7 aircraft, bending to rising pressure to prioritize safety in the wake of a near-catastrophe on one of its planes.

- General Motors Co. beat Wall Street expectations for the fourth quarter and expects profits this year to grow on improved sales as the US economy chugs along.

- Carnival Corp. has rerouted cruise itineraries for 12 ships that were scheduled to go through the Red Sea in May after two months of missile, drone and hijacking attacks by Houthi militants.

- JetBlue Airways Corp. is evaluating deeper cost cuts, delaying aircraft and reworking its flight network in an effort to return to profitability in the wake of the near-collapse of its planned purchase of Spirit Airlines Inc.

- Pfizer Inc. reported fourth-quarter profit that beat analysts' estimates as the US government returned fewer doses of its Covid-19 treatment than predicted.

- Tire firms including Continental AG and Nokian Renkaat Oyj were raided by European Union antitrust watchdogs amid concerns they plotted to fix prices in a move that could pave the way for potentially hefty fines.

- Saudi Aramco abandoned a plan to boost its oil output capacity, a huge reversal that will raise questions about the kingdom's view on future demand.

Key events this week:

- China non-manufacturing PMI, manufacturing PMI, Wednesday

- Japan industrial production, retail sales, housing starts, Wednesday

- Bank of Japan issues summary of opinions from January policy meeting, Wednesday

- Boeing announces earnings amid US government safety probe, Wednesday

- Federal Reserve interest rate decision and Fed Chair Jerome Powell's news conference, Wednesday.

- US Treasury quarterly refunding, Wednesday.

- China Caixin manufacturing PMI, Thursday

- Eurozone S&P Global Manufacturing PMI, CPI, unemployment, Thursday

- US productivity, construction spending, ISM Manufacturing, initial jobless claims, Thursday

- Apple, Amazon, Meta, Deutsche Bank, BNP Paribas earnings, Thursday

- Bank of England interest rate decision, Thursday

- US employment report, University of Michigan consumer sentiment, factory orders, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 fell 0.1% as of 10:51 a.m. New York time

- The Nasdaq 100 fell 0.4%

- The Dow Jones Industrial Average fell 0.1%

- The Stoxx Europe 600 was little changed

- The MSCI World index fell 0.2%

Currencies

- The Bloomberg Dollar Spot Index was little changed

- The euro was little changed at $1.0836

- The British pound fell 0.4% to $1.2658

- The Japanese yen fell 0.2% to 147.85 per dollar

Cryptocurrencies

- Bitcoin rose 0.7% to $43,486.2

- Ether rose 1.5% to $2,340.93

Bonds

- The yield on 10-year Treasuries advanced two basis points to 4.10%

- Germany's 10-year yield advanced six basis points to 2.29%

- Britain's 10-year yield advanced four basis points to 3.91%

Commodities

- West Texas Intermediate crude rose 0.9% to $77.49 a barrel

- Spot gold was little changed

This story was produced with the assistance of Bloomberg Automation.

--With assistance from John Viljoen, Ryan Vlastelica and Jessica Menton.

More stories like this are available on bloomberg.com

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.