Honasa Consumer Ltd. got a 'buy' rating as Citi Research initiated coverage on the owner of Mamaearth.

The owner of multiple beauty and personal care brands continues to strengthen its position in Mamaearth, through consumer-centric innovation, distribution expansion (gaining shares in offline channels), and entering fast-growing sub-categories (colour cosmetics), the research firm said in a Feb. 22 note.

Market share gains through distribution expansion, innovation, growth in new brands, and improving financial metrics could keep absolute multiples elevated, the note said.

Strong growth in other brands (The Derma Co., Aqualogica, and Dr. Sheth's) bodes well and helps address specific consumer needs and accelerate growth, it said.

Citi Research has a target price of Rs 550 on the stock, implying an upside return potential of 26.9%. This is the second highest target after Jefferies' Rs 590 apiece.

Financial Performance Improving With Scale

Citi estimates Honasa's consolidated revenue to grow 25% CAGR over FY24-26E, driven by 14% CAGR at Mamaearth—largely led by offline expansion—and 46% CAGR in other brands.

"We estimate Ebitda to grow at a faster clip of 55% CAGR (11% Ebitda margin in FY26E vs 7.1% in FY24E), driven by ad-spend rationalisation, improving channel mix and operating leverage," the note said.

Investment Thesis

Honasa is the leading digital-first BPC company in India, having scaled up to more than 5% market share in the online segment, Citi said.

Since the launch of its flagship brand Mamaearth in 2016, the company has transformed into a portfolio of six brands (a combination of organic and M&A-led expansion) and has even increased its presence in the offline channel, which constituted 36% of the business in FY23, according to the research firm.

"This has resulted in the company capturing 1.6% market share of the overall BPC market in India and has now become the 13th largest BPC brand in India in a relatively short span of time," it said.

Key Downside Risks

Slower-than-expected growth delivery.

Accumulation of slow-moving inventory in the offline channel (at distributors and retailers).

Competitive pressure both from large incumbents (as they get better at innovating for the new-age consumer) and newer D2C players.

Higher discounting across the market could delay profitability expansion.

Limited consumer traction in new products/investments.

Over-dependence on third-party manufacturers.

Risk of excess supply of shares in the market once the lock-ins for pre-IPO players expire.

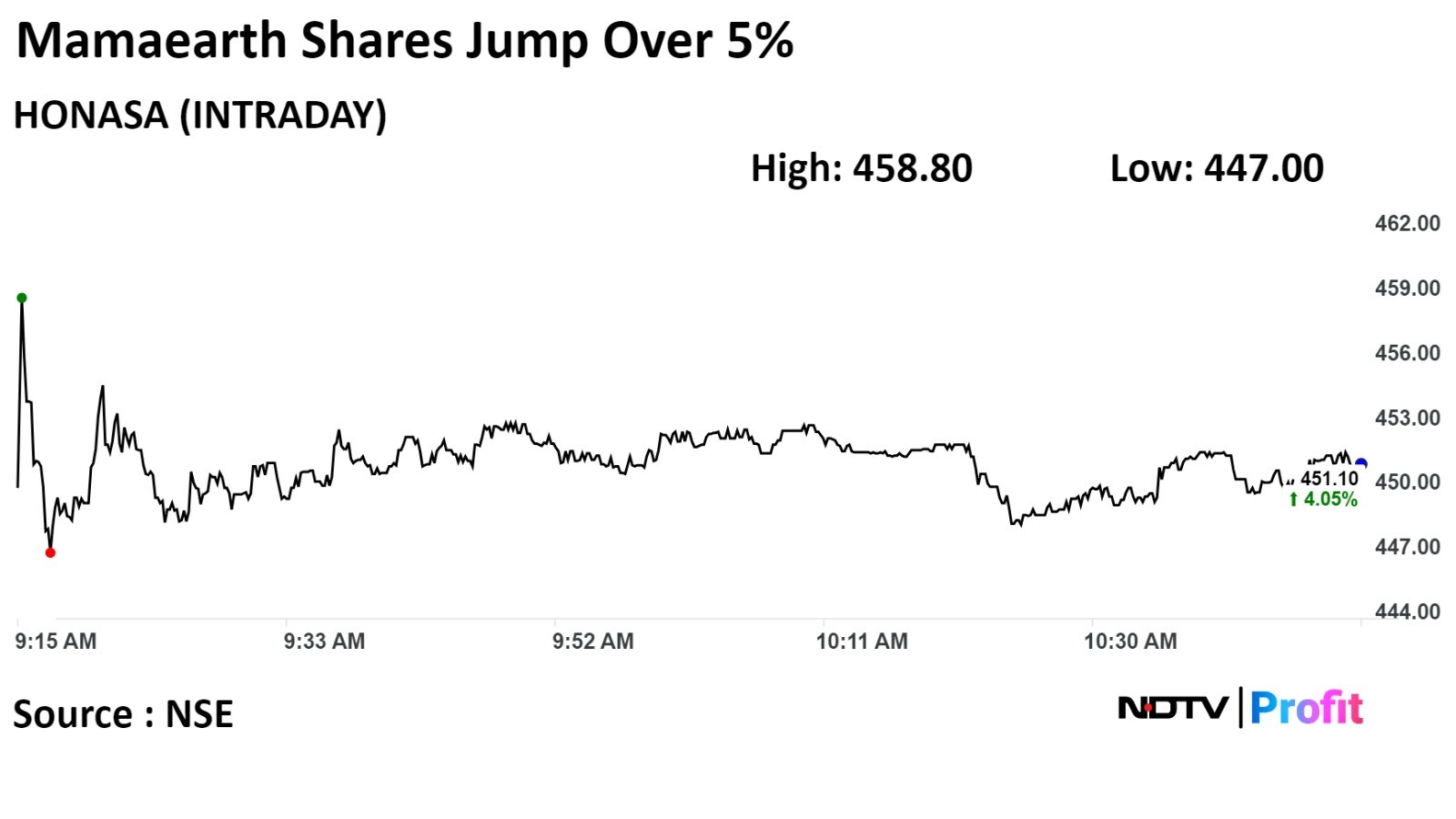

Shares of Honasa Consumer Ltd. rose as much as 5.82%, the most since Feb. 14, before paring gains to trade 4.14% higher at 9:31 a.m. This compares to a 0.12% advance in the benchmark Nifty 50.

The stock risen 33.94% in the past 12 months. The total traded volume so far in the day stood at 1.5 times its 30-day average. The relative strength index was at 53.29

Of the four analysts tracking the company, three maintain a 'buy' rating and one suggests a 'sell', according to Bloomberg data. The average of 12-month analysts' price targets implies a potential upside 13.8%.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.