(Bloomberg) -- Jonathan Hoffman, John Bonello and Jonathan Tipermas share more than just similar first names. They're the driving force behind a gigantic wager on government debt that's been giving regulators sleepless nights.

They and their teams are top players in the “basis trade,” a bet by a few of the world's biggest hedge funds that profits from the tiny price gaps between Treasuries and derivatives known as futures, people active in the market say. That makes them some of the most important individuals in finance today.

As part of a core group of 10 or so firms, they rely on vast sums of money borrowed from Wall Street banks — often 50 times what they invest themselves — to pump tens of billions of dollars into the trade and supercharge returns. So colossal are their bets that some say they've become central to the buying and selling of Treasuries, itself the cornerstone of global capital markets.

Hoffman, 51, of ExodusPoint Capital Management, Bonello, 52, at Millennium Management and Tipermas, 41, at Citadel have used the wager for years to produce gains that run into the billions, according to several people familiar with the traders who requested anonymity as the details aren't public.

Others also do the trade at a vast size, the same people say, including Yan Huo and Ryan Letchworth at Capula Investment Management, Citadel's Ivan Chalbaud, founder of Symmetry Investments Feng Guo and Steve Brown at Balyasny Asset Management. Lorenzo Rossi of Kedalion Capital Management is active, too, as is Alexander Phillips at Tudor Investment Corp.

This group is rarely in public view. But interviews with more than a dozen market participants and documents reviewed by Bloomberg point to their dominance of a wager that's roared back to life this year. A senior Wall Street figure who's worked for years with the core players estimates they account for roughly 70% of hedge fund basis-trade bets.

The firms and traders named in this piece all declined to comment.

Now regulators have the hedge funds in their sights, fearing a repeat of March 2020 when the bet blew up spectacularly — just before the Federal Reserve had to jump in to resuscitate the Treasury market. Last week the Securities and Exchange Commission, alarmed by the sheer scale of borrowing involved, voted in new rules that may make the economics of the trade less enticing.

But regulators are in a bind. Crack down too hard and they could threaten the orderly running of a US Treasuries market that's ballooned to $26 trillion since the pandemic. Go too easy and there's the threat of too much financial leverage building up at these hedge funds. The size of the traders' positions means the Fed may have to intervene if they hit trouble again.

“There are only a couple of players and these players have made themselves too big to fail,” says Kathryn Kaminski, chief research strategist at AlphaSimplex Group, a Treasury investor. “If you limit this arbitrage, you weaken market liquidity.”

Read More: Hedge Funds Get SEC Mandate to Clear Treasuries Trades

Market Makers

Unlike other vaunted hedge fund traders who make splashy bets on the direction of currencies or interest rates or wage high-profile campaigns against companies, Hoffman, Bonello and others quietly target differences in price between Treasuries and Treasury futures — closely linked derivatives that give investors the right to buy or sell the debt in the future.

For a mix of reasons the futures price is often higher than the bond's, so the trader sells the former, buys the latter and pockets the difference. Because the gap is usually mere fractions of a penny this is only worth doing at scale, ramping up returns through the use of leverage. That largely limits the activity to a few trusted individuals at hedge funds with enough clout to borrow big from banks in overnight money markets.

What's the Basis Trade? Why Does It Worry Regulators?: QuickTake

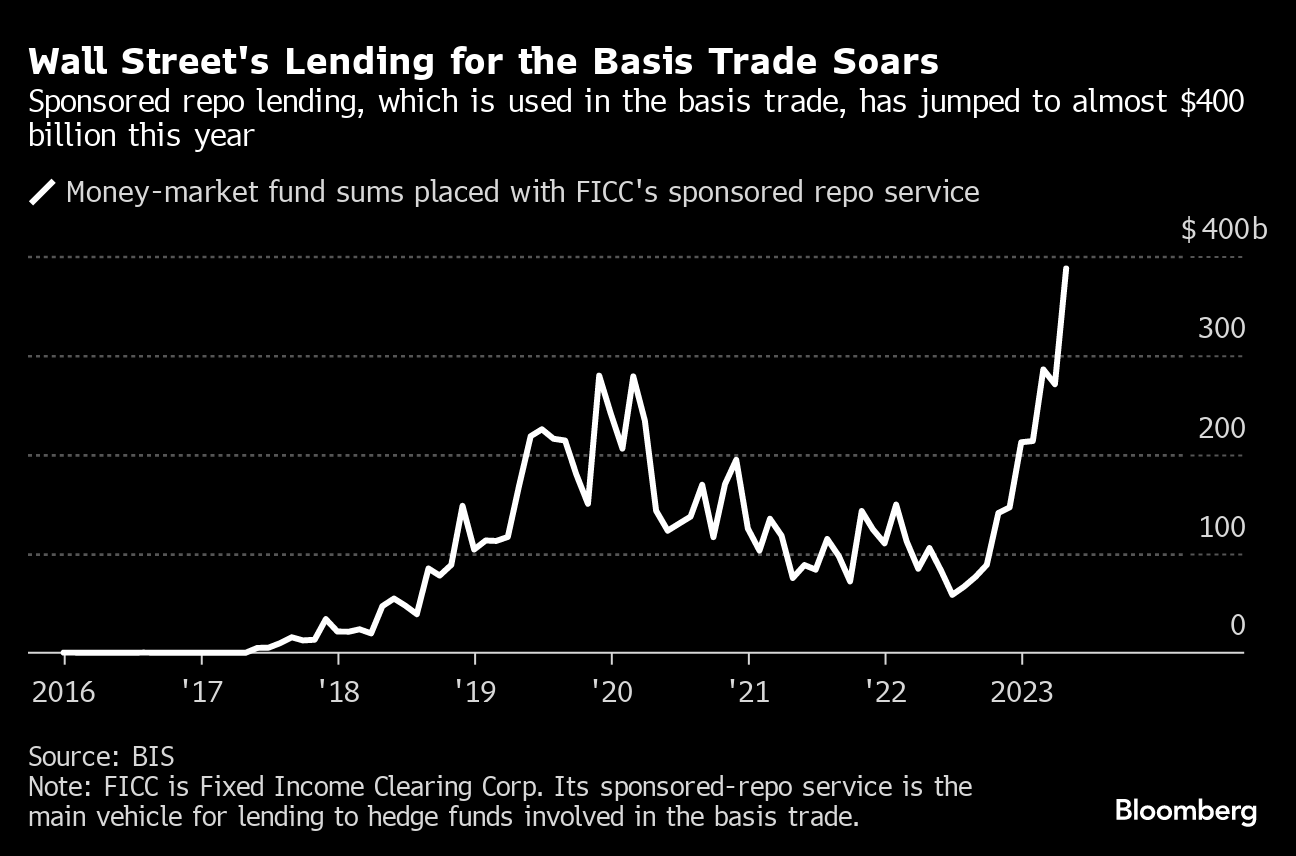

As the availability of this short-term lending has surged this year, the basis trade has boomed. The net short position on Treasury futures, a reasonable proxy for the wager's popularity, has spiked to $800 billion from $650 billion in July, the Bank of England said on Dec. 6.

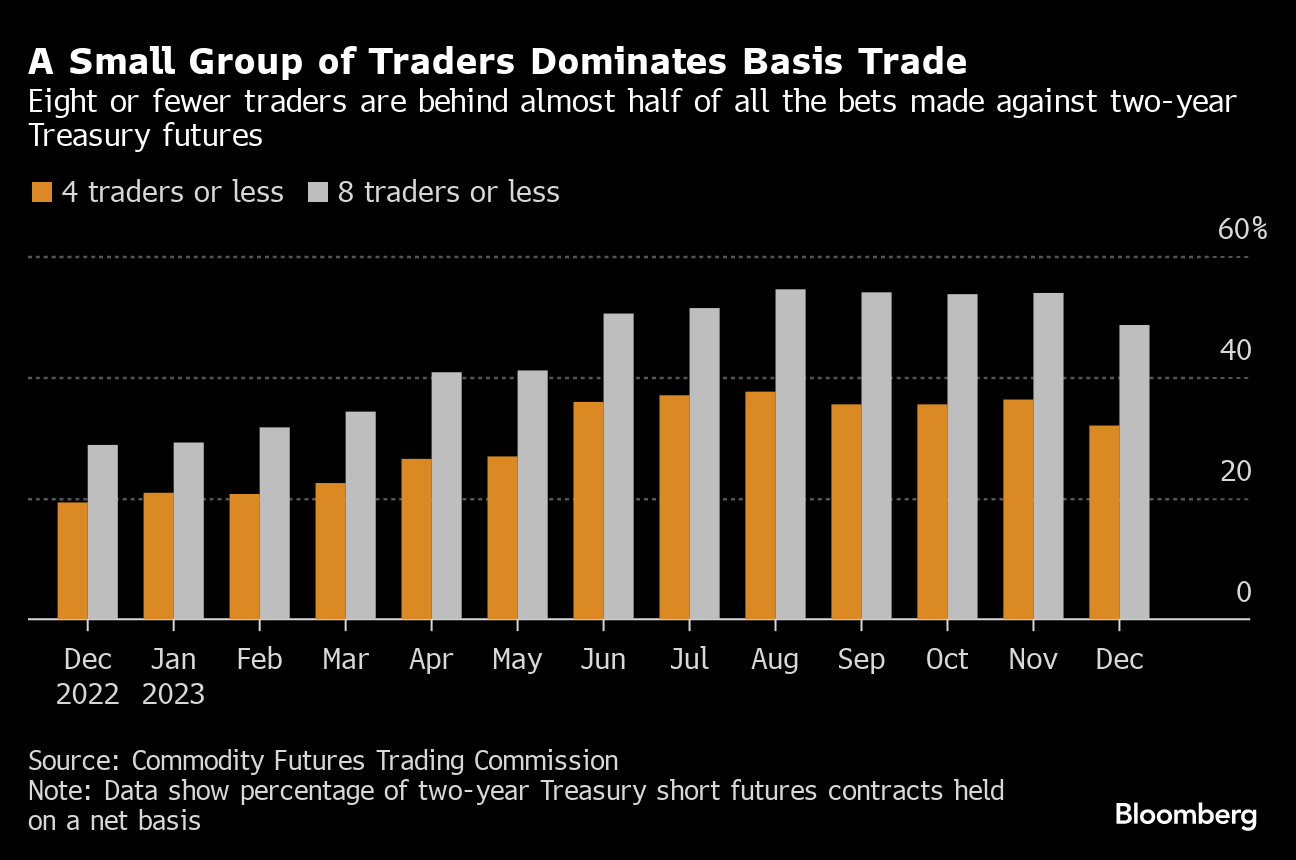

While it's difficult to tell how much of this is held by the core trader group, the wager has become more concentrated this year. Eight or fewer traders are behind almost half of all bets against two-year Treasury futures, compared with 29% a year ago, data from the Commodity Futures Trading Commission shows.

Defenders of the trade such as Citadel's Ken Griffin say the enormous volume of buying and selling by hedge funds means they're helping to make the Treasury market efficient. Wall Street banks used to perform this critical “market making” role but have retreated because of new leverage rules imposed after the financial crisis.

Critics ask whether it's wise to lean so heavily on a few hedge funds, pointing to Covid's early days in March 2020 when market turmoil forced them to rapidly unwind their positions. That may have added to a sudden drying up of Treasury liquidity, and it left the basis traders staring at huge losses. The Fed had to intervene to keep markets running, pledging trillions of taxpayer dollars.

The Fed's rescue mission calmed the Treasury market and helped the traders recover. Bonello's team at Millennium generated nearly $1.5 billion of profit in 2020, a record, and that year's basis trade contributed to the $1 billion Hoffman has generated since joining ExodusPoint in mid-2018. Rossi, then at LMR Partners, turned millions of losses during that March into profit.

The 2020 episode may have fed a belief among some in the group that the central bank will always ride to the rescue, market participants say. “There's an implicit ‘Fed put',” says Eric Rosenfeld, formerly of Salomon Brothers' government-arbitrage desk in the 1980s and a cofounder of Long-Term Capital Management, a hedge fund that imploded in 1998. But it's not a question of “too big to fail,” he asserts, more that the “Fed is responsible for maintaining a liquid, free-flowing Treasury market.”

Gary Gensler, the SEC chair, told Bloomberg in October that if another meltdown happens, “It's going to be the public that bears the risk.”

Lehman Roots

The group traces its roots to the same Wall Street banks that dominated the trade before the financial crisis. Some overlapped at the same firms and learned the wager from each other or the same mentors, people familiar say.

Hoffman joined Lehman Brothers in 1994 after studying at the University of Pennsylvania and rose the ranks as a Treasury trader. An old colleague recalls how he grasped the importance of the “repo” team — the bank unit that makes short-term loans in the overnight money markets — and was often seen standing next to the desk's boss, peppering him with questions.

By the 2000s, Hoffman, known to colleagues as “H,” had moved to Lehman's Miami office and was one of its best-paid employees. His trades could be volatile but always seemed to pay off. In early 2008, fixed-income trading head Andrew Morton told the board that a team had lost $157 million in March, adding a single word to his presentation: “Hoffman.” By year end, “H” had turned the losses around and generated $550 million of revenue, filings show.

Bonello started as a Merrill Lynch salesman and became a trader after moving to Deutsche Bank AG in 2003. He joined Millennium three years later. Before 2020, he and his team of five to seven people had several years of making hundreds of millions of dollars in profit. The team has grown since.

Tipermas was a competitive wrestler at the Massachusetts Institute of Technology and a dollar-swaps trader at Goldman Sachs Group Inc. before joining Citadel in 2014. His team of more than 20 makes on average hundreds of million of dollars yearly, people familiar say. Not all of these profits come from the basis trade. Most of the teams make other wagers as well, such as bond auctions and different punts on price gaps.

The core trader group has little online profile. But they have occasionally stepped into the public realm.

Hoffman sued Lehman in 2014, claiming the now-defunct bank owed him $83 million in pay. It emerged that Barclays Plc had already paid him $83 million to get him to join the UK bank and then awarded him $100 million for 2008 through 2010, filings show. A judge dismissed his claim. A private figure, he's largely based in Pennsylvania, where he owns a $5 million house outside Philadelphia. He has plowed some of his fortune into a high-end property-lending business in Miami.

The more gregarious Bonello has since 2020 bought a $20 million Manhattan apartment next to Central Park and a $34 million Los Angeles mansion overlooking the Pacific, filings show. In 2006, while at Deutsche Bank, he was fined $20,000 to settle allegations by the Chicago Board of Trade that he'd engaged in “pre-execution conversations.” He didn't admit any wrongdoing.

Tipermas has a $5.6 million property in Connecticut and keeps a lower profile.

Some see Hoffman as the trade's guiding light but its history goes back further. He learned the transaction at Lehman from Munir Dauhajre, a Wall Street veteran who also worked with Bonello and other basis traders, people familiar say. Dauhajre, in turn, picked it up from Suresh Sundaresan, a professor at Columbia University who also worked at Lehman for a time in the 1980s.

One market participant describes Sundaresan as the true intellectual godfather of the basis trade. In an interview with Bloomberg, the finance professor warned that the industry has become “more levered than ever before with the possible exception” of just before the financial crisis.

“Regulators' concerns are fully justified,” he says. “My worry is that an exogenous shock may lead to margin calls, which may result in insolvencies or big losses for the hedge funds.”

March Mayhem

Unlike other investors who bet on US debt, basis traders don't have to form a view on the economy or fret over the Fed's plan for rates. They just need to wait for the price of the futures to drop to the level of the linked Treasury, something that almost always happens at the time the derivatives contract expires, and they can book a profit.

Matt Levine's Money Stuff: People Worry About Basis Trade

But things go wrong. Borrowing costs can spike overnight. Hedge funds can get demands for more collateral from banks. Even a small change can lead to “large cash outlays and in the worst-case scenario could lead to outright failure,” the US Office of Financial Research wrote in 2020.

All of this played out four years ago. Bonello's team suffered more than $100 million in losses at one point in March 2020. Millennium, which has had just one losing year in more than three decades, was down as much as 5% at one stage.

ExodusPoint also faced heavy losses, the same people say. Tipermas' Citadel suffered declines, too. Others faced similar trouble. Rossi, then just 33, made more than $250 million for LMR in 2019, according to a person with knowledge of the matter, but as the March meltdown hit, his losses soared.

After the Fed stepped in, the basis trades bounced back. Citadel ended the month making money, while Millennium almost fully recovered. By the end of March, Rossi was profitable again. He left LMR last year and founded Kedalion, a fund backed by Millennium.

Paul Tudor Jones, owner of the Tudor hedge fund, said recently that the Fed had “bailed out” his firm's trades, which were under “extreme duress.” Tudor remains active today through Phillips, a onetime basketball star at MIT who joined last year.

Should a repeat happen, some hedge fund executives point to their large cash reserves, which can be used in emergencies.

Levered Up

Basis-trade bets can take days to complete, according to Howard Finkel, an industry veteran whose decades in finance included a stint at Millennium. This demands secrecy to stop rivals guessing what you're up to, he says — one reason why the group is so private.

“It's not like basis traders are one big happy family,” Finkel adds. “When you have a huge trade on, if somebody gets wind of that, the wrong person, and they try to squeeze you, that's your biggest fear.”

Enabling all this is the group's abundant access to the magic ingredient that lets it happen: leverage. Wall Street giants such as JPMorgan Chase & Co. and Bank of America Corp. lend to them in massive volumes in exchange for fees.

Banks have only a fixed amount of leverage to dole out, so they tend to favor their best clients. Multi-strategy hedge funds such as Millennium, Citadel and ExodusPoint are a perfect match because they have other high-turnover businesses attractive to Wall Street lenders.

The trade is “dominated by a few large hedge funds that have more balance sheet allocated to them based on how important they are,” says Martin Malloy, a professor at North Carolina's Wake Forest University who helped lead businesses at Citigroup Inc. and Barclays that financed some of the funds.

For hedge funds, part of basis trading's beauty is that they often borrow at “zero margin” from banks, meaning no extra collateral has to be put up and they can take more profit. The new SEC rules state that from 2026 repo deals will have to go through central clearing, increasing the margin requirement.

Whether this dims the wager's allure is uncertain but some analysts say Treasuries will become harder to trade and more expensive. This may create greater opportunities for the group even if they have to pursue them with less borrowed money, one person familiar with the industry's workings says.

“Central clearing will mean higher costs for hedge funds,” UBS Group AG strategists wrote this month, “suggesting they'll need price dislocations to be larger before they put on trades that provide liquidity to the market.”

The difficulty for policymakers, analysts say, will be fixing this faultline without causing tremors in US Treasuries, the world's most important bond market.

“If we don't allow regulated entities to make markets, then we set up this scenario, it's evolution,” says Kaminski at AlphaSimplex, referring to the emergence of the basis traders on finance's center stage. “And if they do it in a systemically important market, they're naturally going to have that too-big-to-fail angle.”

--With assistance from James Hirai and Liz Capo McCormick.

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.