(Bloomberg) -- Bond traders are turning to the short-dated maturity Treasury options market to hedge potential for soaring Treasury yields over the coming days, ahead of key risk events including Thursday's December inflation report.

The theme has been prominent since the start of the year, as open interest, or the amount of new risk, has soared in put options targeting a Treasuries selloff over call options. Activity has picked up again this week, with demand continuing to emerge before December CPI and PPI as well as auction event risk.

Traders Target Weekly US Options to Hedge Near-Term Event Risks

To be sure, an underlying long position remains in the Treasury market and it could be the case that the aggressive buying is more a reflection of this positioning, rather than outright bets on higher yields. The bullish stance has been sustained from the back-end of last year, albeit with diminishing conviction. “Tactical positioning is now only mildly long, with short profits offset by long losses with risk now balanced,” Citigroup strategists Ed Acton and Bill O'Donnell note in a Monday paper.

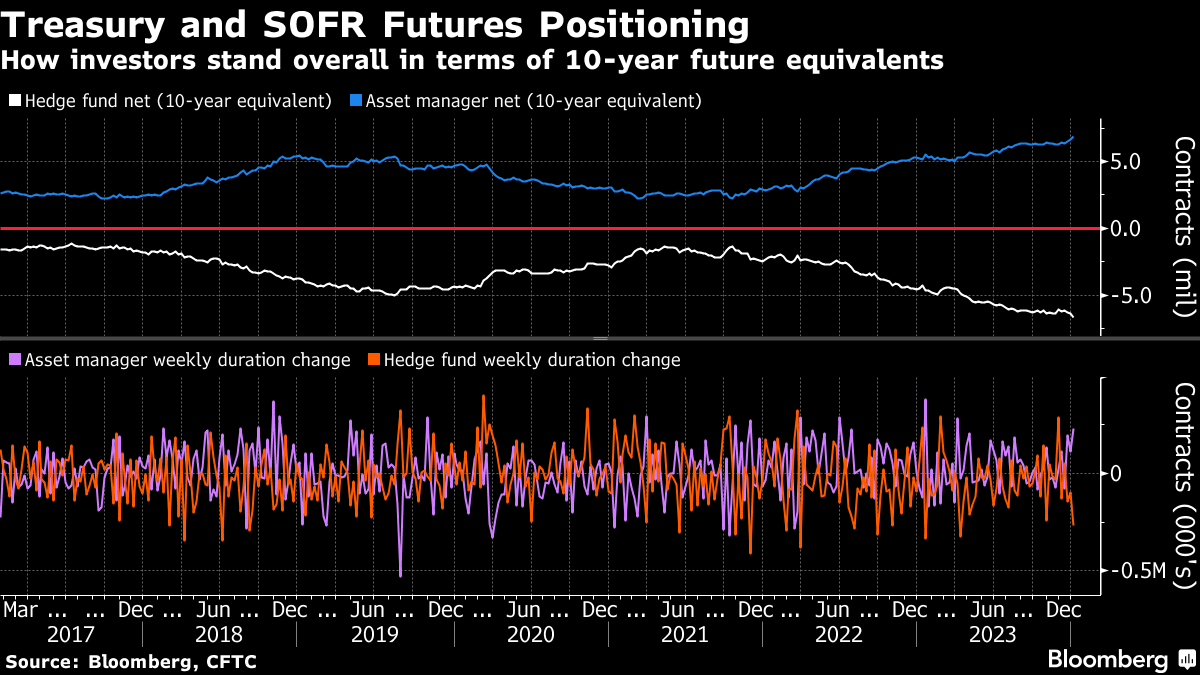

Meanwhile in the futures market linked to the Secured Overnight Financing Rate, hedge funds have now cut net longs for a third straight week, according to CFTC data up to Jan. 2. In the cash market, investors have shown a more balanced directional view since the start of the year with neutral positions rising to the most in around four months, according to a JPMorgan Treasury client survey in the week through Jan. 8.

Here's a rundown of the latest positioning in various corners of the market:

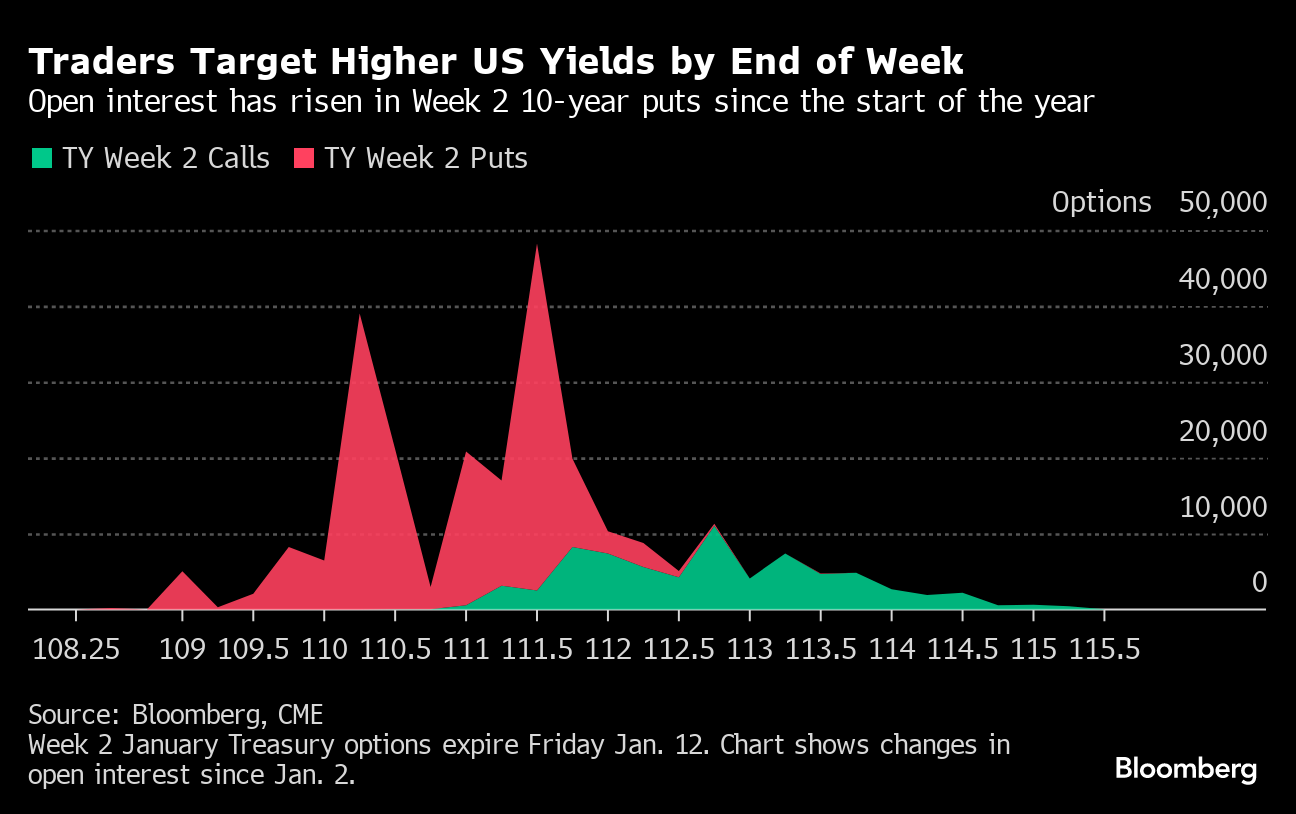

Weekly Options Surge

Since the start of the year, demand for protection on a Treasuries selloff via the Week 2 10-year options, which expire Friday Jan. 12, has risen sharply. These types of short-dated expiry options act as hedges against event risk; this week, the event risks include bond auctions, CPI and PPI data. Largest demand over the week has been at the 111.50 put strike, which equates to roughly 4.10% 10-year yield.

Hedge Funds Cut Long SOFR Futures

For the third week in a row, hedge fund net long SOFR futures positioning has been reduced, this week by around $4.2 million per basis point in risk, per CFTC data up to Jan. 2. Further out, the divergence between asset manager and hedge fund positioning rose sharply, with asset managers extending duration long from 2-year out to ultra-long by $14.5m per basis point and hedge funds adding to duration short across same tenors by net $14.8m per basis point risk.

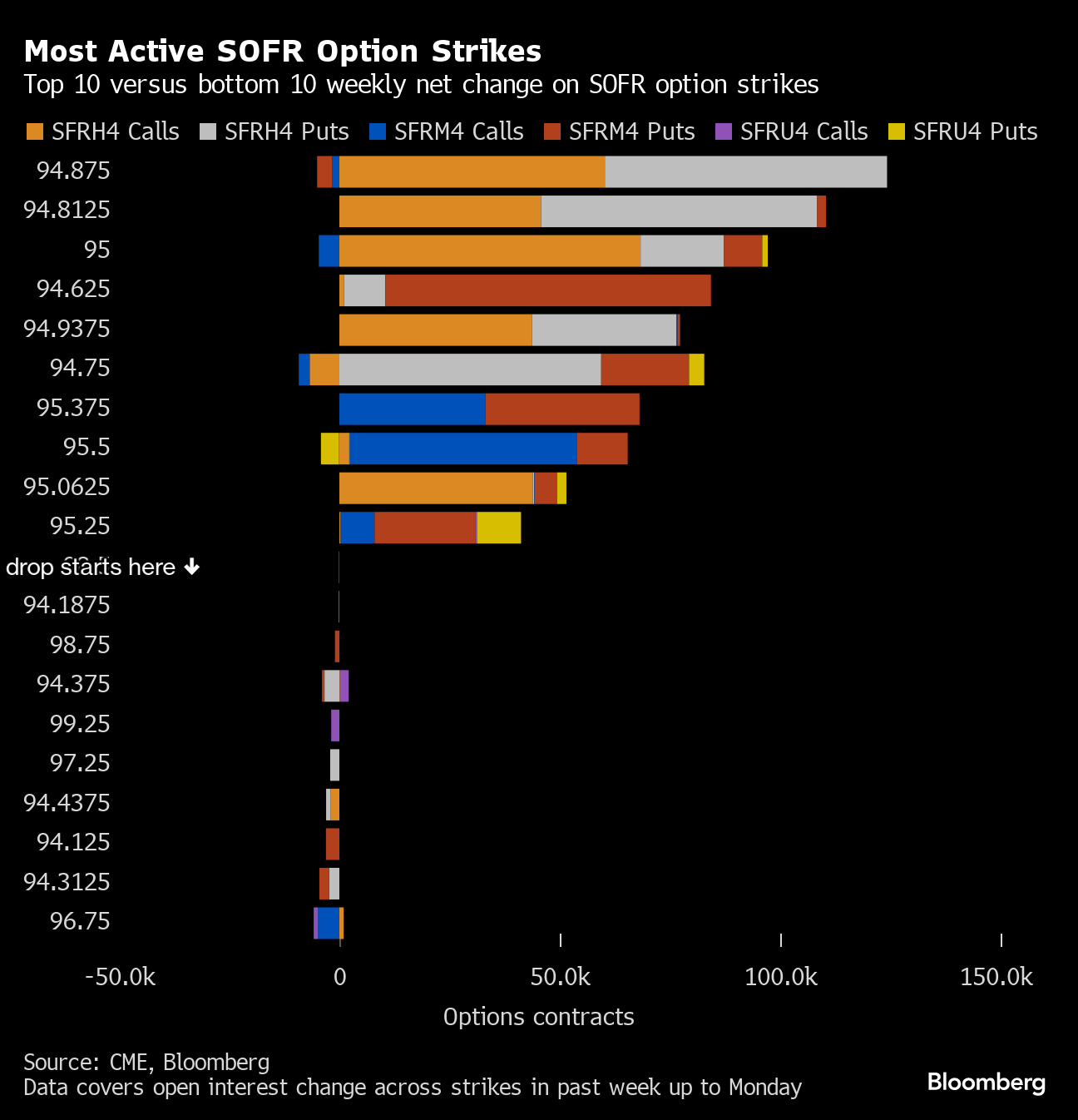

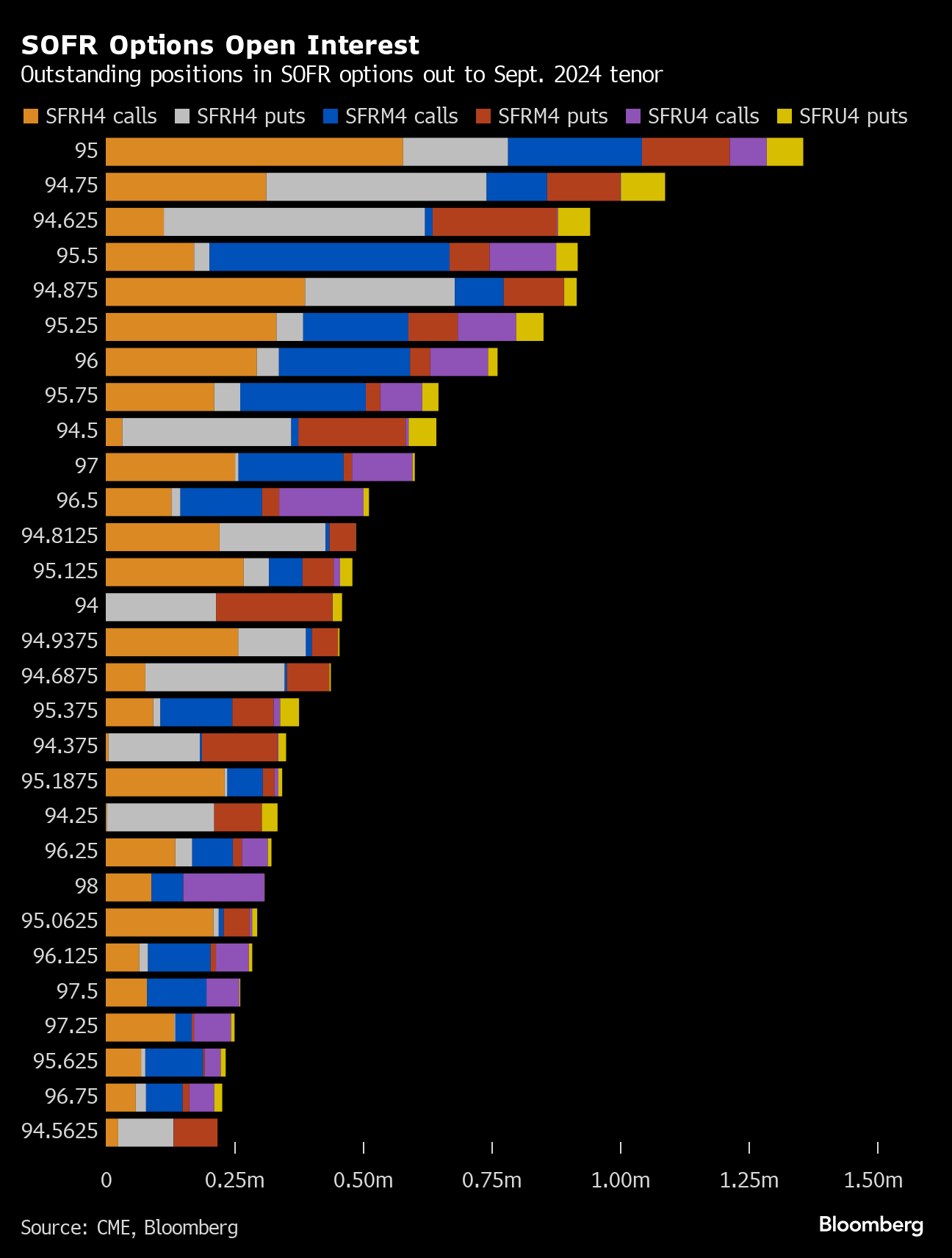

SOFR Option Actives

Over the past week, changes in open interest have been dominated by March 2024 SOFR options, where risk has climbed across a number of call and put strikes. The activity is consistent with traders looking to pin down pricing for the March policy meeting.

Overall options positioning across Mar24, Jun24 and Sep24 tenors remains most elevated in the 95.00 strikes, where a strong presence of Mar24 calls sits. Large portion of the outstanding open interest in the Mar24 95.00 strike sits with a large dovish postion targeting a full 25bp of cuts priced into the March policy meeting via SFRH4 94.875/95.00/95.125 call fly where overall exposure has now risen to around 135,000.

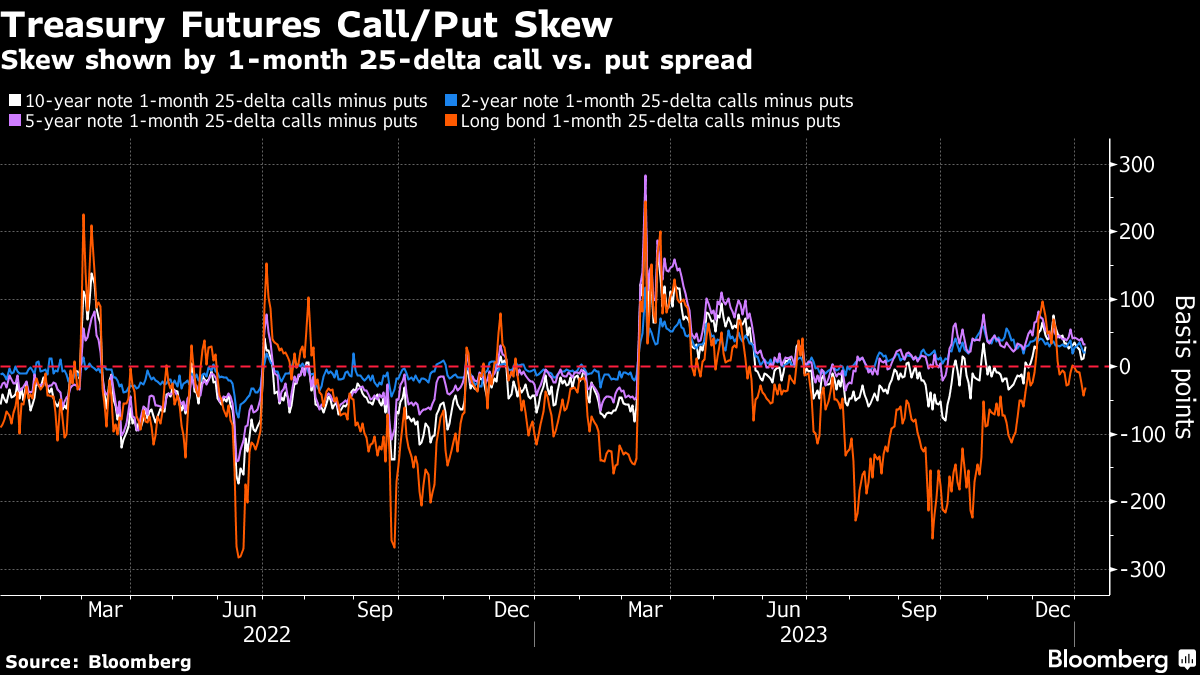

Skew Back to Neutral

After favoring call options towards the end of last year, skew has eased back to neutral over the first few sessions of this year. In long-end, premium is again favoring hedging a selloff in Treasuries over a rally, in line with the back-up in yields from as low as near 4% in 30-year on Jan. 3 to current 4.17%.

More stories like this are available on bloomberg.com

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.