Yuan's Fallout for Markets Means No Summer Lull for Traders

Chinese yuan’s tumble to one-year low is putting traders on alert during a sleepy Northern hemisphere summer.

(Bloomberg) -- The market turmoil spurred by the Chinese yuan’s tumble to a one-year low is putting traders on alert during the normally sleepy Northern hemisphere summer.

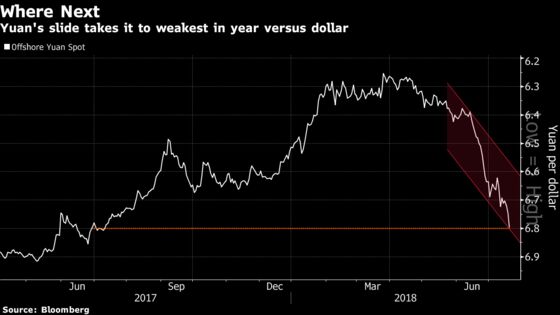

The onshore yuan was set for a weekly decline of 1.3 percent, extending a losing streak to six straight weeks. The plunge took most Asian currencies along for the ride amid broad dollar strength, with copper sliding below $6,000 a metric ton for the first time in a year on Thursday. While the yuan was supported on Friday amid speculation of intervention, the central bank’s seeming indifference earlier caught investors off guard.

The People’s Bank of China weakened its fixing beyond 6.7000 per dollar Thursday for the first time since August 2017. With trade tensions between the Washington and Beijing simmering -- and possibly providing motivation for the Asian nation to let the yuan drop further -- the volatility may continue.

“The line in the sand may have shifted higher, causing the market to pay up,” said Neil Jones, the head of hedge fund sales at Mizuho Bank Ltd. in London, who added that a drop to 7 per dollar would be a major concern. “It’s not shaping up to be a summer lull.”

The yuan’s weakness is already drawing the ire of U.S. President Donald Trump, who said to CNBC that the currency is “dropping like a rock,” putting America at a disadvantage. Still, he PBOC was undeterred, weakening the daily reference rate by the most in two years Friday.

The slide in China’s currency this week had multiple drivers, including Federal Reserve Chairman Jerome Powell’s upbeat assessment of the U.S. economy, a view that’s likely to keep the central bank on a gradual policy-tightening path. It’s also been punished by growing pessimism about the outlook for Chinese economic expansion amid the nation’s deleveraging drive, as well as concern about the fallout from a possible trade war between the world’s two largest economies.

Investors are also trying to gauge the impact of China’s efforts to bolster growth by loosening monetary policy. Banks are being offered cash and given instructions to boost lending, according to the banking and insurance regulator, adding to evidence of a shift toward greater official support for the economy.

“It certainly does have traders sitting up, even if not fully engaging yet,” said Oliver Jackson, the global head of sales trading at Saxo Bank A/S. The slump in the yuan “did catch most by surprise, but it seems the market is now buying the lack of intervention as a positive note towards a shift in fiscal policy.”

Along with Mizuho, strategists at Nomura International Plc also raised the possibility of the yuan falling to 7 per dollar, a level it hasn’t seen since 2008. TD Securities analysts see commodity-linked currencies from Australia, New Zealand and Canada as “collateral damage.” Societe Generale said the yuan will be a factor that “drives the dollar.”

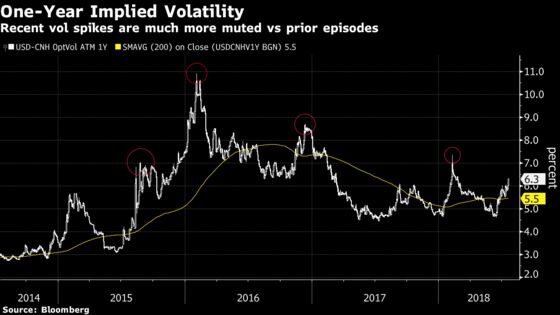

Options markets haven’t priced in significant fluctuations in the months to come. One-year implied volatility for the offshore yuan has climbed above 6 percent after the recent spot selloff. Still, that’s far lower than this year’s high of more than 7 percent reached in February, not to mention spikes in 2015 and 2016 that pushed double digits.

Strategists, however, are showing considerably more pessimism, citing policy makers’ hands-off approach to the slide. The central bank may see the yuan’s drop as beneficial to exporters, the companies in the cross-hairs of the U.S.’s increasingly aggressive trade stance.

“Don’t underestimate the geopolitics,” said Viraj Patel, a strategist at ING Groep NV in London. The “PBOC letting market forces work and not intervening is a signal -- Washington can’t have its cake and eat it, can’t call out China for manipulating currency markets -- and then have a go at them for letting market forces prevail.”

But it doesn’t mean the PBOC can turn a blind eye if the weakness in the yuan accelerates. Authorities will keep in mind what happened a few years back, when a rapid depreciation drove capital outflow and policy makers were compelled to tighten financial conditions.

“Authorities have deep scars from the 2015-2016 experience,” said Calvin Tse, the North American head of G-10 FX strategy at Citigroup Inc. Still, so far, “all the signs we’ve seen from China have shown a favoring of fine-tuning measures.”

--With assistance from George Lei, Lananh Nguyen and Katherine Greifeld.

To contact the reporter on this story: Anooja Debnath in London at adebnath@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Brendan Walsh, Boris Korby

©2018 Bloomberg L.P.