(Bloomberg Opinion) -- To many in the petroleum industry, natural gas is the unsung hero of the energy transition.

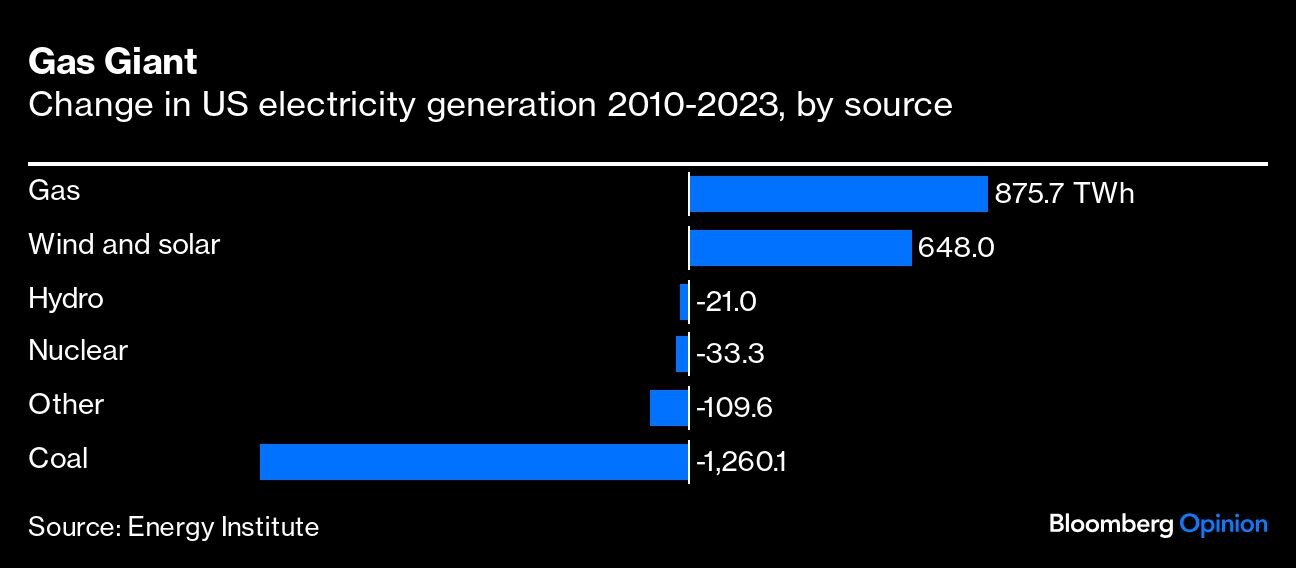

It may not be a clean fuel, but it's nowhere near as dirty as coal, which it has been pushing out of grids in Japan, South Korea, Canada, and Poland over the past decade. In the US, which produces nearly 30% of the world's gas-fired electricity, generation increased by 876 terawatt-hours between 2010 and 2023 — more than the 648 TWh pick-up in wind and solar — and enough to explain three-quarters of the 63% decline in coal power.

That's led to expectations it might repeat the trick in the big developing Asian markets still hooked on solid fuel, such as China, India, Indonesia, Pakistan, and Vietnam. It's not going to happen — but that doesn't mean that gas is done causing damage to its fellow fossil fuels. In Asia, it's oil that will be in the firing line instead.

The reason is price. Though we often count fossil fuels in tons, barrels, and cubic meters, the thing that really matters is almost always their energy content. If you're a serious energy consumer, the really important measure is not how much coal, oil or gas you are buying, but what you're paying for the megajoules or kilowatt-hours of energy it's going to give you when burned.

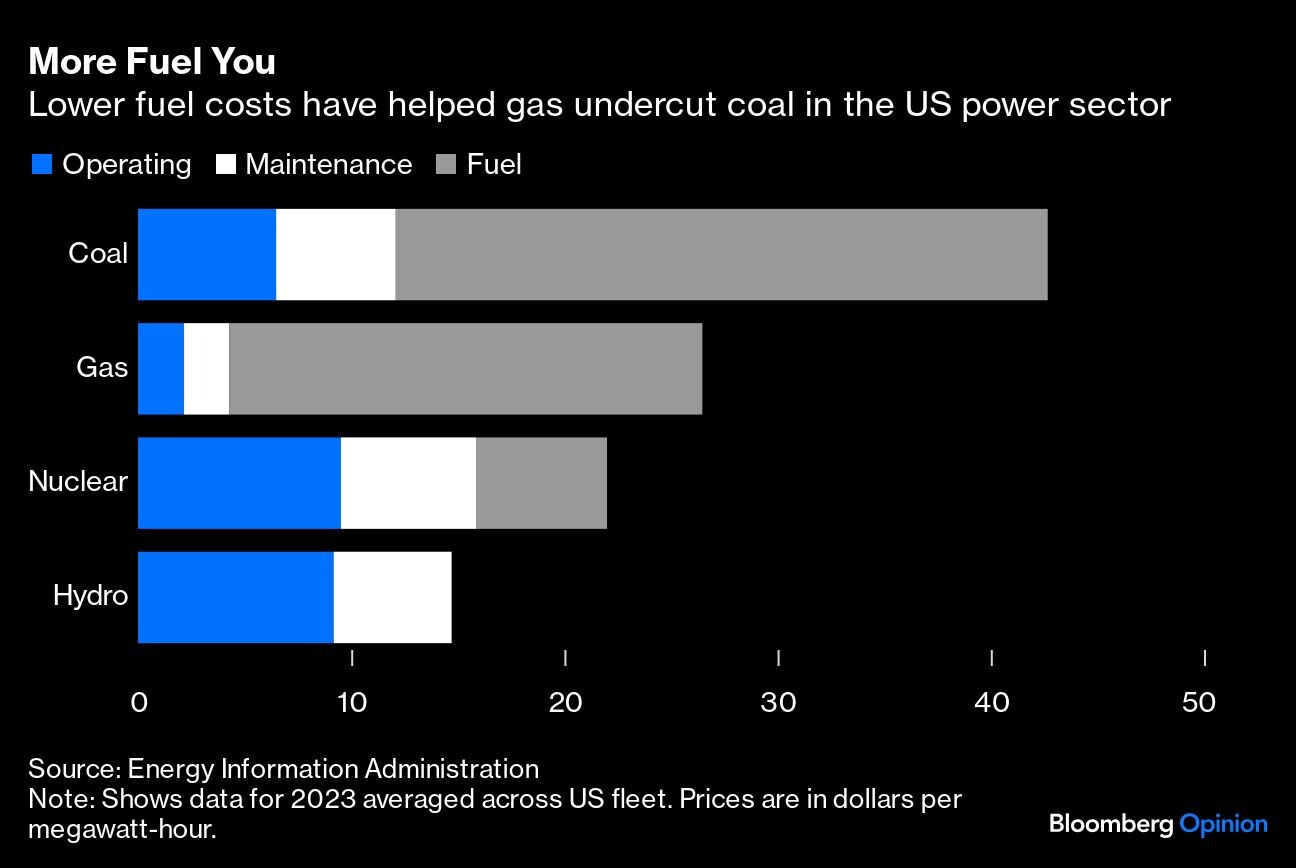

That's why gas has been such a potent competitor to coal in the US. About a quarter of domestic production is a byproduct from oil wells, and as a result it's often more or less given away. At the Waha Hub, a pricing point in the fracking-rich Permian Basin in western Texas, it's averaged minus 11 cents per million British thermal units all year.

There's no way to compete with that. Overheads at a typical US gas generator last year were about 38% lower than those at a coal plant. Faced with a pincer movement from this negative-cost gas and zero-cost wind and solar, coal didn't stand a chance. A similar pattern played out in Europe over the past decade, and even the Ukraine war and disappearance of cheap Russian gas hasn't been enough to revive solid fuel.

Things are different in developing Asia, a region with scant gas reserves but substantial domestic coal deposits. Liquefying natural gas and shipping it across the world is an expensive business, and as a result benchmark Asian LNG costs more than five times what you'd pay at Henry Hub, the main US pricing point.

That's left gas largely absent from the major grids, despite the hopes of LNG exporters. In China and India, it accounts for only 3% or so of electric power, far below levels around 40% in the US and Russia, 70% in the Middle East, and 30% in wealthier Asian import markets such as Japan, South Korea and Taiwan. Generation has actually been falling in India over the past decade, and barely growing even in Indonesia, historically one of the world's biggest producers.

There's one place where it's making real inroads, though: vehicle engines. As compressed natural gas or CNG, gas offers compelling value: a kilogram contains more energy than the same mass of diesel or gasoline, and engines are also more efficient at converting that energy into motion. You'll spend about 9.75 rupees (12 cents) for each megajoule of useful power from Indian diesel at current prices, and 12.28 rupees when buying gasoline. CNG is drastically cheaper, at around 4.66 rupees per megajoule.

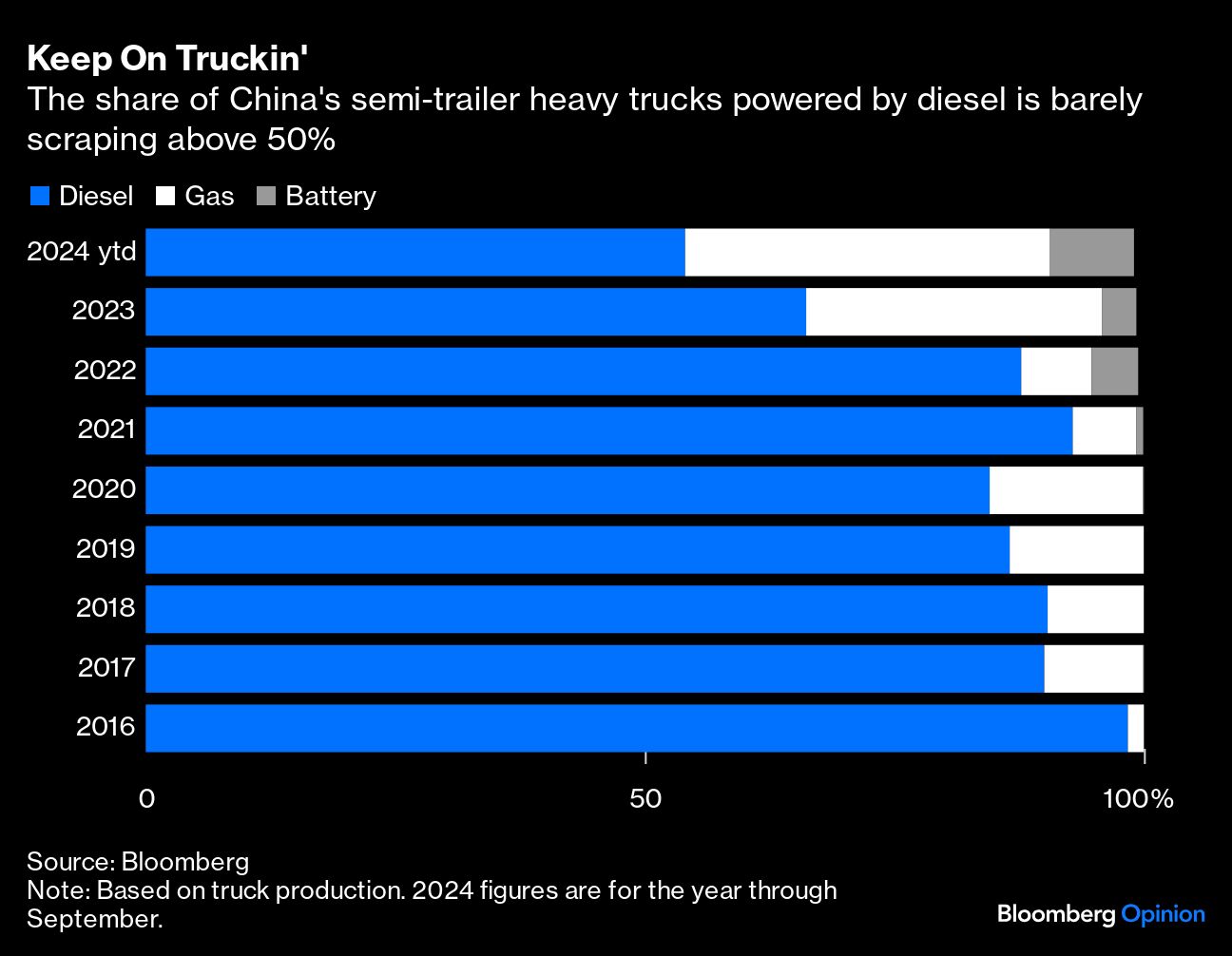

Batteries are still usually the cheapest way to provide energy to small vehicles such as scooters, three-wheelers and cars — but heavier trucks and buses, which command an outsized share of road fuel demand, have lavish power needs that make it easier to convert to CNG. In China, the share of the biggest semi-tractor haul trucks produced with diesel engines has fallen from 93% in the first nine months of 2021 to 54% in the same period this year. A cash-for-clunkers program introduced in July, offering as much as 80,000 yuan ($11,200) for scrapping old dirty trucks, will accelerate that replacement cycle.

Even the seas aren't immune. The world's shipyards are increasingly turning to LNG to power vessels due to its cost advantage over crude-derived marine fuel oil. About 6% of the world's operating and under-construction fleet is powered by the fuel at present. Typically the world's shipyards receive orders for a thousand or so new vessels each year. Through October, 464 of those orders were powered by alternative fuels, including 177 LNG ships and 162 using methanol, according to maritime data service DNV. With the tanker and container fleets rapidly ageing, the scrappage already under way in China's truck market will soon spread to the oceans.

The damage gas has wrought to US and European coal over the past decade is testament to the way it can work hand-in-hand with carbon-free energy to wreak havoc on the dirtiest sources of power. The same game is set to play out in the crude market over the coming decade.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.