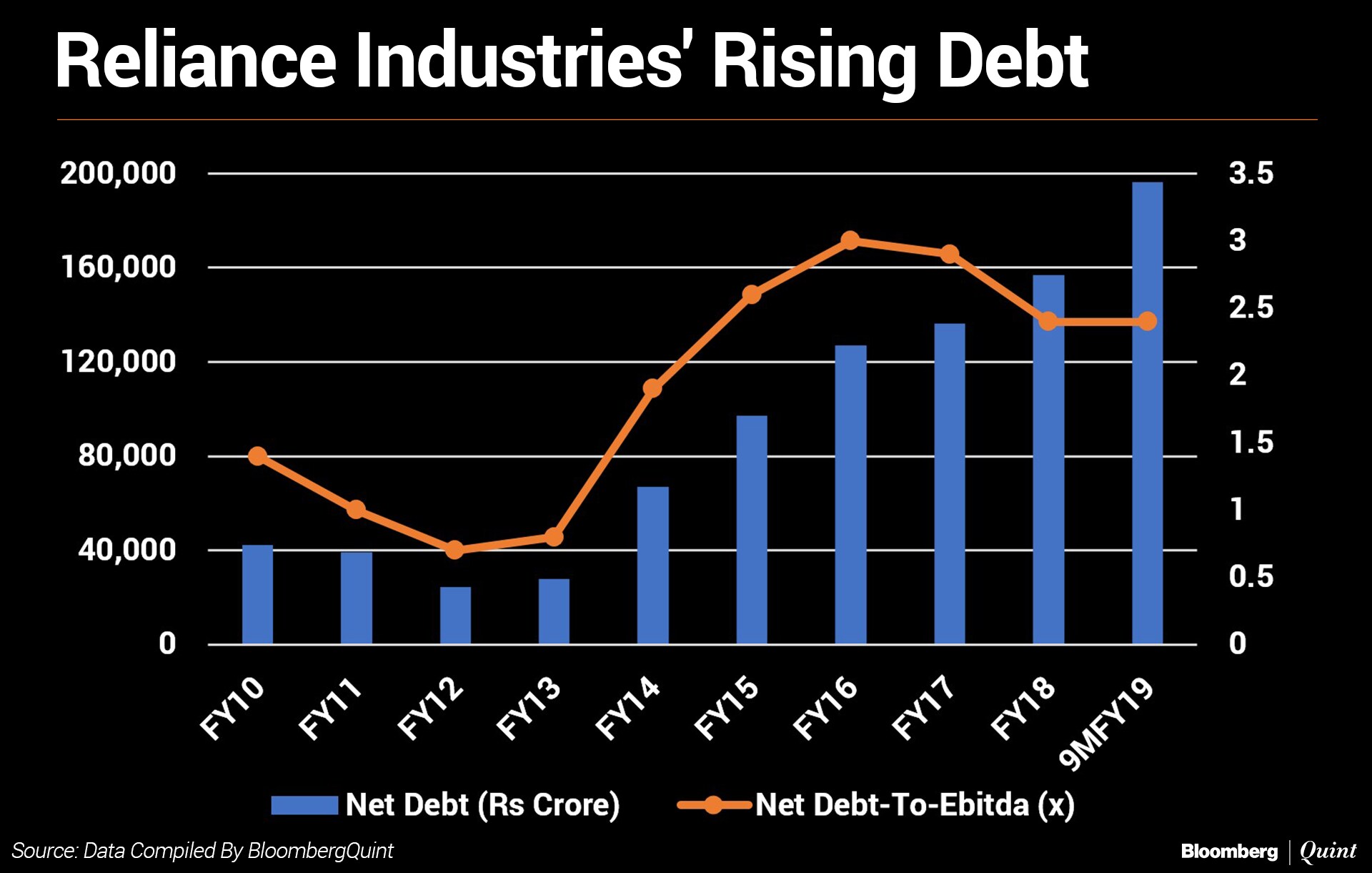

Reliance Industries Ltd. plans to monetise its tower and fibre assets to reduce a debt of more than Rs 1.7 lakh crore.

The oil-to-telecom conglomerate, in an analyst meet after announcing December-quarter results, said its telecom arm will look to monetise the assets through a special purpose vehicle where cash flows are predictable. Also, Reliance Jio Infocomm Ltd. is open to sharing towers and fibre assets with other telecom operators, it said.

Reliance Jio has 2.20 lakh towers and nearly 3 lakh kilometres of optical fibre assets. The company's decision to sell its non-core telecom assets is a “game changer”, according to Edelweiss Securities. “It is likely that Reliance Industries has lined up strategic buyers for monetisation,” it said. “A sale would lead to a 33 percent dip in debt.”

CLSA expects the monetisation to be completed in the first half of 2019. It will deleverage a large portion of the company's debt and allay a key concern, the research firm said.

Rising debt has been an overhang for the company led by India's richest man. Since the launch of Reliance Jio, the parent's consolidated debt has been rising due to higher capital expenditure. The Mukesh Ambani-led company, however, was able to maintain its leverage ratio due to higher contribution from consumer and petrochemicals businesses.

Moody's Investor Service and Fitch Ratings Inc. have kept their long-term ratings on Reliance Industries same as that of India at BAA2 and BBB-, respectively, according to Bloomberg.

Reliance Jio earlier this month said it had filed a scheme of arrangement with the National Company Law Tribunal to demerge its tower and fiber assets into separate entities. The move is subject to regulatory approvals.

Brokerages remain upbeat on Reliance Industries as it managed to beat estimates in a seasonally weak quarter. The company's gross refining margin fell to $8.8 a barrel due to global weakness but was higher than the $8.3-per-barrel estimate. Its consolidated net profit was aided by a strong performance of the retail and telecom segments.

Shares of Reliance Industries jumped as much as 2 percent—the highest in over a month—after the company's third-quarter earnings beat estimates.

Here's what the brokerages have to say:

Morgan Stanley

- Maintains ‘Overweight' with a target price of Rs 1,230—potential upside of 8.4 percent from last closing price.

- Third-quarter earnings slightly ahead of estimates, thanks to higher-than-expected production.

- Cost inflation and demand challenges are unwinding.

- Signs of tightening chemical and refining markets in the second half to lower investor concerns on margin.

Citi

- Maintains ‘Buy' with a target price of Rs 1,300—potential upside of 14.6 percent from last closing price.

- Resilient performance in a tough quarter.

- Telecom and retail segments remain strong.

- Planned asset monetisations to address balance sheet concerns.

UBS

- Maintains ‘Sell' with a target price of Rs 1,070—potential downside of 5.7 percent from last closing price.

- Petchem better-than-expectations; other income helped to beat estimates.

- Expects investors to look positively at increasing contribution from Reliance Industries' consumer businesses, robust performance in petchem and gross refining margin.

Macquarie

- Maintains ‘Outperform' with a target price of Rs 1,315—potential upside of 16 percent from last closing price.

- Petchem was the key positive surprise, while refining, Reliance Jio and retail were in line.

- Expects Reliance Industries' refining margin to strengthen to $15/$20/$18 a barrel in FY20-22.

- Sees upside risk to consensus earnings estimates.

Edelweiss

- Maintains ‘Buy' with a target price of Rs 1,415—potential upside of 25 percent from last closing price.

- Consumer and petchem shine; lower operating expenditure offsets lower gross refining margin.

- Multiple triggers: petcoke gasifier on schedule for March 2019 and an imminent fibre-to-home rollout.

Prabhudas Lilladher

- Maintains ‘Accumulate' with a target price of Rs 1,238—potential upside of 9 percent from last closing price.

- Stellar petrochemicals performance makes up for weak refining earnings.

- Reliance Industries with high complexity well placed to capitalise benefits of International Maritime Organization's new regulations, including low-sulphur fuel oil to be used in ships, effective 2020.

- Maintains rating as it awaits clarity on petcoke commercialisation.

Antique Stock Broking

- Maintains ‘Hold' and hikes target price to Rs 1,245 from Rs 1,180—potential upside of 10 percent from last closing price.

- Higher petrochemicals production drives marginal beat.

- Refining impacted by weaker margin.

- Proposed demerger to remain asset light and focus on core operations.

Emkay

- Maintains ‘Buy' with a target price of Rs 1,335—potential upside of 17.7 percent from last closing price.

- Ebitda ahead of estimates on slightly better-than-expected segmental core earnings.

- Consumer businesses continue to scale up.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.