A decision by Franklin Templeton Mutual Fund to wind-up six yield-oriented, managed credit funds, may ripple through India's corporate debt markets, with fixed income managers fearing lower liquidity and higher yields for all but top-rated bonds.

On Thursday, Franklin Templeton informed investors that it would be winding-up six of its debt schemes due to large redemption pressure at a time when liquidity in Indian bond markets has dried up.

The combined assets under management of the six debt fund schemes stands at a little over Rs 30,850 crore as of March 31, 2020, according to Value Research. The majority of holdings across the debt funds are rated AA and below.

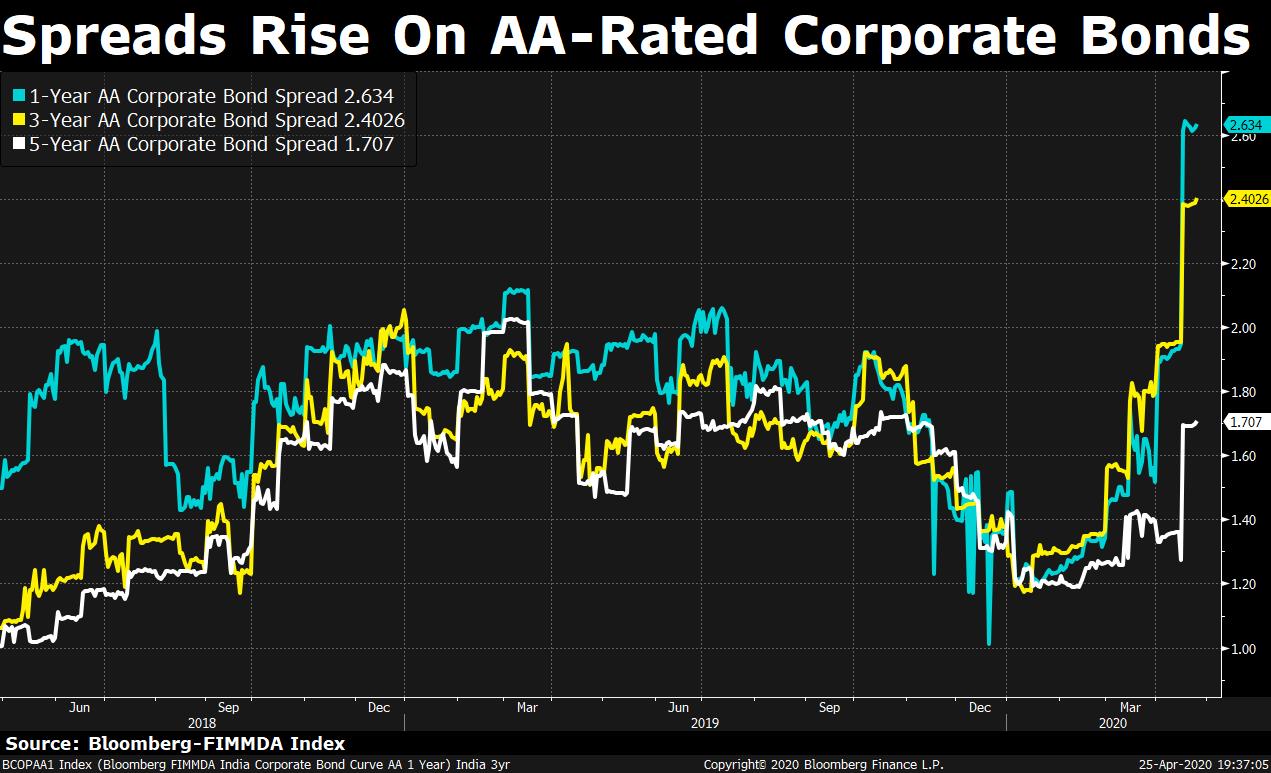

Yields On AA-Rated Bonds Rise

The impact of Franklin Templeton's decision may be first felt on bonds rated AA and below. Yields on AA-rated bonds had spiked even before the announcement.

Data from Bloomberg shows a jump in spreads, or the additional interest sought by investors over government bonds of comparable tenor, ahead of the announcement by Franklin Templeton. On Friday, spreads remained stable at those elevated levels.

As of Friday, AA-rated corporate bonds for a three-year duration were trading at 240 basis points over the comparable government bond yields. Shorter dated one-year bonds saw an even wider spread of 263 basis points.

Volume of trades on Friday was low but the handful of trades that took place in securities held by Franklin Templeton mutual funds took place at elevated levels, according to data from the National Stock Exchange.

Vedanta Ltd.'s bond, with a coupon rate of 8.75 percent maturing in 2022, traded at a yield of 11 percent. Uttar Pradesh Power Corporation's bond, with a coupon rate of 8.97 percent maturing in 2022, traded at a yield of 10.6 percent. Shriram Transport Finance Corporation's bond, with a coupon rate of 10.25 percent maturing in 2024, traded at a yield of 12.5 percent.

All three bonds have a credit rating of AA.

Credit Risk vs Liquidity Risk

The debate among market participants is whether the troubles faced by Franklin Templeton are a consequence of credit and liquidity risk in its own portfolio or a market-wide phenomenon.

A report by B&K Securities showed that Franklin Templeton was the sole lender to 26 of the 88 securities in its portfolio. Forty three securities had 50 percent or more of their borrowings from the fund house.

In the case of such securities, Franklin Templeton may bear a larger share of the risk than other funds in the industry. The large share of securities held by one fund house would also make these securities less liquid.

However, the broader corporate debt market is also plagued by illiquidity.

Ajay Manglunia, managing director and head of institutional fixed income at JM Financial Products Ltd., said that over the last two years, liquidity in the secondary markets has been very low for AA-rated and A-rated bonds.

“Since these bonds are thinly traded, in an event like this, the spreads are usually likely to widen as bidders know the compulsions that someone else has to sell,” he said.

Lakshmi Iyer, chief investment officer for debt at Kotak Asset Management Co. Ltd., said that the key issue facing corporate bonds right now is liquidity and not credit risk.

“It is important to understand that the credit rating is not the only indicator predicting whether a bond is good or bad. While some bonds may not have a high rating, they are good businesses at the end of the day. There is a liquidity issue for corporate bonds in secondary market and not a credit risk issue facing the industry,” Iyer said.

Still, rising credit risk can't be ignored.

Analysis of recent actions by rating agencies indicates an increasing trend of corporate downgrades even before the nationwide lockdown was imposed to curb the spread of Covid-19.

Rating agencies downgraded 1,579 corporates in FY20 until February compared to 892 downgrades in FY19, according to a report by KR Choksey Research on Friday. “This clearly indicates that corporate financial strength is deteriorating lately and more stress pockets are expected to emerge in the present situation,” the report said.

Also Read: BQ Big Decisions: As A Crisis Hits Debt Funds, Is Your Money Safe?

Regulatory Intervention

In the current environment, investor sentiment has taken a big knock and portfolios have seen a flight to safety, said Arvind Chari, head of fixed-income and alternatives at Quantum Advisors.

“Despite all the actions taken by the Reserve Bank of India, the financial system remains frozen but for government bonds, public sector undertakings bonds and strong AAA rated corporates. The rest of the players still find it difficult to access the bond market and that acts as a feedback loop which further increases risk aversion amongst investors,” he said in a recent note.

In 2008 and then again in 2013, the RBI opened a special window through which banks could access short term funds to provide liquidity to mutual funds. On Friday, the central bank did not announce any such step, adding to the nervousness.

Also Read: A Star Franklin Manager Gets Burned in Market He Helped Create

Former finance minister P. Chidambaram urged regulators to announce such a window to prevent the build-up of a system crisis. “I expect that the government will act promptly,” Chidambaram said.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.