Chinese lawmakers are gathering in the shadow of the US election to sign off on a fiscal package that's set to run into the trillions of yuan yet is unlikely to put the market fully at ease.

The stakes have grown for this week's conclave of the Standing Committee of the National People's Congress, the executive body of the nation's top legislature, as it's expected to round out China's largest effort to lift growth since the pandemic.

The session in Beijing on Nov. 4-8 will probably unlock additional resources meant to take the pressure off local governments and recapitalize major state lenders, according to banks such as Goldman Sachs Group Inc. and HSBC Holdings Plc.

But with the US presidential race still tight and Chinese policymakers putting priority on the more immediate challenges facing the $18 trillion economy, it may be months before detailed plans to support consumption come into focus. Policy-setting meetings in December or March are the next key dates to watch for clues about measures to prop up consumer spending power, which will be crucial to turning around sentiment.

“They don't want to come up with a big number and then not be able to get it done,” said Nicholas Yeo, head of China equities at abrdn. “The government is very cautious about spending.”

The lingering suspense over the pacing and targets of fiscal support will complicate investment decisions for traders already whipsawed by the volatility stalking Chinese markets since a stimulus blitz in September sought to encourage lending and offered support for the stocks and property markets.

The outcome of the US election could also force Beijing to strengthen efforts to bolster domestic demand, given the threat by Republican nominee Donald Trump to impose hefty tariffs on Chinese goods if elected.

Economists at Goldman Sachs, Macquarie Group, and Nomura Holdings Inc. predict lawmakers this week will back at least 1 trillion yuan ($140 billion) in quota of special sovereign bond issuance to replenish bank capital. They also expect approval for an increase in local government bond sales either this week or in the coming months to swap so-called hidden debt over several years, with forecasts ranging from about 6 trillion yuan to 10 trillion yuan.

Nomura anticipates the eventual scale of China's fiscal stimulus package to reach 2%-3% of gross domestic product annually over the next several years, with a Trump win to push its size toward the higher end.

“For us, the specific size of the stimulus package is less important than the area of focus for the package to be deployed,” said Herald van der Linde, head of Asia-Pacific equity strategy at HSBC. “Property is important to stabilize sentiment and growth. And China could focus on stimulating consumption.”

The capital injection will aim to improve the capacity of state-owned banks to extend credit as they heed the government's call to lend more at lower interest rates to help the economy. It's an approach that's narrowed margins to record lows and undermined their ability to boost capital with profits.

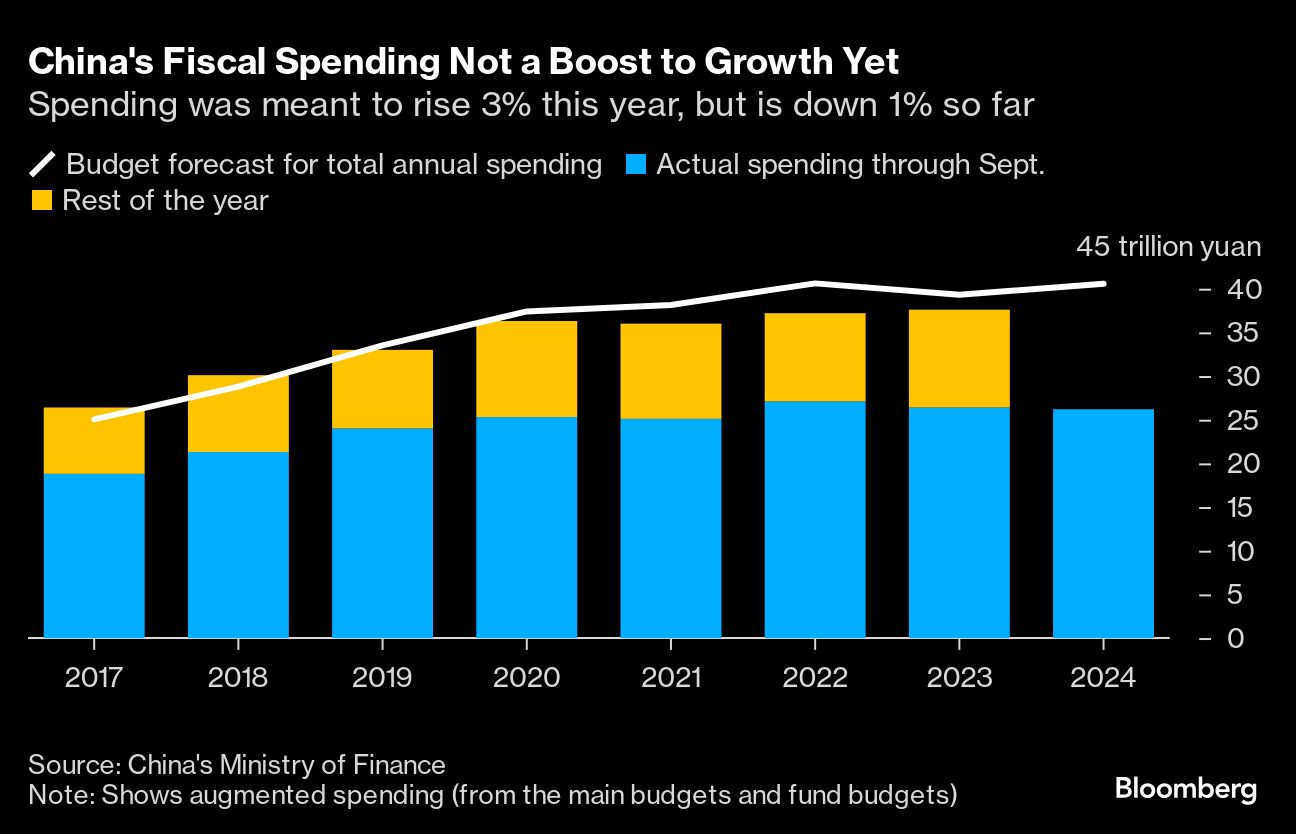

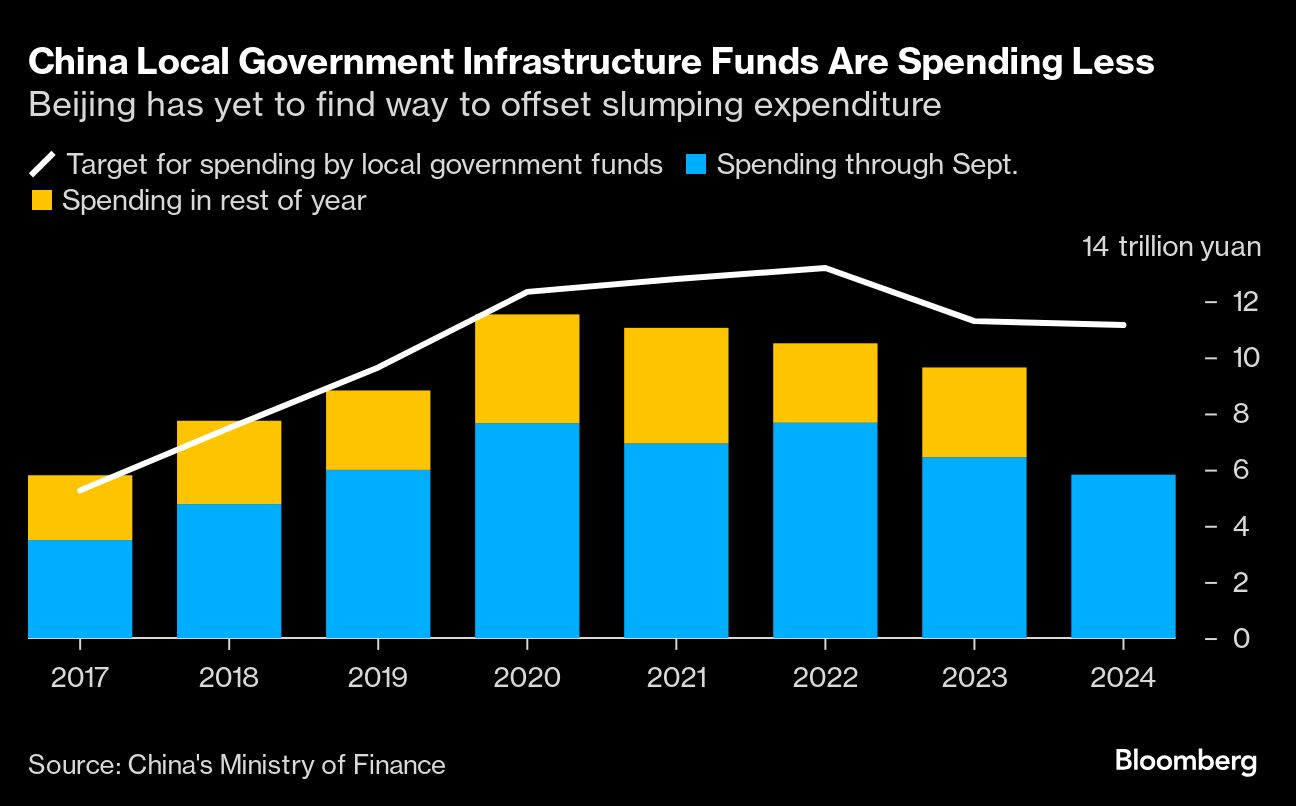

China's local governments have meanwhile been scaling back spending as the economic downturn and a years-long property slump erode revenues from taxes and land sales. Many are also cautious about taking on new borrowing to finance investment amid falling returns and as they scramble to comply with President Xi Jinping's crackdown on hidden liabilities.

The debt swap program will bring local governments' off-balance-sheet borrowing onto their books, lowering the interest costs and giving the authorities more time to repay, which in turn will free up resources for regions to ramp up spending.

What Bloomberg Economics Says...“The NPC standing committee might provide more information on fiscal resources the government will devote to stimulus. In our view, the meeting is unlikely to increase the budget for 2024. But given the strong hints by the government on potentially stronger fiscal support, the committee is likely to give some topline figures on resources for debt resolution and support for households and companies.” — Chang Shu, Eric Zhu and David Qu. For full analysis, click here

While a swap of 1 trillion yuan may add just 2 basis points directly to GDP growth, the boost would be “larger” if some proceeds from refinancing bond issuance can be used to repay overdue wages to civil servants and arrears to businesses, according to estimates by Goldman economists including Lisheng Wang.

An additional 1-2 trillion yuan in government borrowing per year may also be put in place to ease local fiscal stress, with the relevant “extra budget” to be passed by the legislators this week, Nomura economists led by Lu Ting wrote in an Oct. 28 note.

The government could announce additional spending programs worth up to 4 trillion yuan — probably financed mainly through more bond sales — at the annual full session of the NPC in March or even later to strengthen the social safety net for low-income groups, encourage childbirth, and ensure the delivery of pre-sold homes, they said.

“The old playbook that they have always used is infrastructure and real estate — but there's a need for domestic consumption to do some of the lifting,” said abrdn's Yeo. “That shift has to happen at some point. That is the one thing that we want to see.”

But Beijing has been hesitant to hand out massive, direct subsidies to consumers. A main factor behind the reluctance is the potential cost of such programs in a nation of 1.4 billion people where GDP per capita is less than $13,000, or just 15% of that in the US, along with a greater propensity to save.

Another concern centers on the effectiveness of consumption stimulus given the lack of a proper system to identify those most in need and therefore more likely to actually spend the money.

That said, analysts broadly anticipate Beijing would open the fiscal taps to support consumption if the US slaps more tariffs on China's exports after the election, a scenario likely to put the brakes on growth.

This week's legislative huddle may not be the “deadline” for raising the government debt limit, according to Goldman economists. A later meeting by lawmakers around year-end and the NPC's full session in March are also “possible windows” to watch, they said.

Investors may get a glimpse of what may be on the government's planning board even before that. The Politburo, made up of the ruling Communist party's top 24 officials including Xi, usually holds a meeting with a focus on the economy in early December, days before the Central Economic Work Conference takes place to set the agenda for the coming year.

“The good thing is that investors are more afraid to short now given that we don't really know the number that will come out and there is more room to get the next meeting ‘right,'” said Ivy Ng, chief investment officer for Asia Pacific at DWS Investments Hong Kong Ltd. “The consumption part is the wildcard.”

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.