(Bloomberg) -- The dollar will surprise by getting stronger next year as the US economy outperforms, according to some of the world's biggest money managers.

Fidelity International, JPMorgan Chase & Co., and HSBC Holdings Plc. are going against consensus by warning of dollar strength, while Loomis Sayles & Co. says a global economic slowdown will see traders flock to the world's reserve currency.

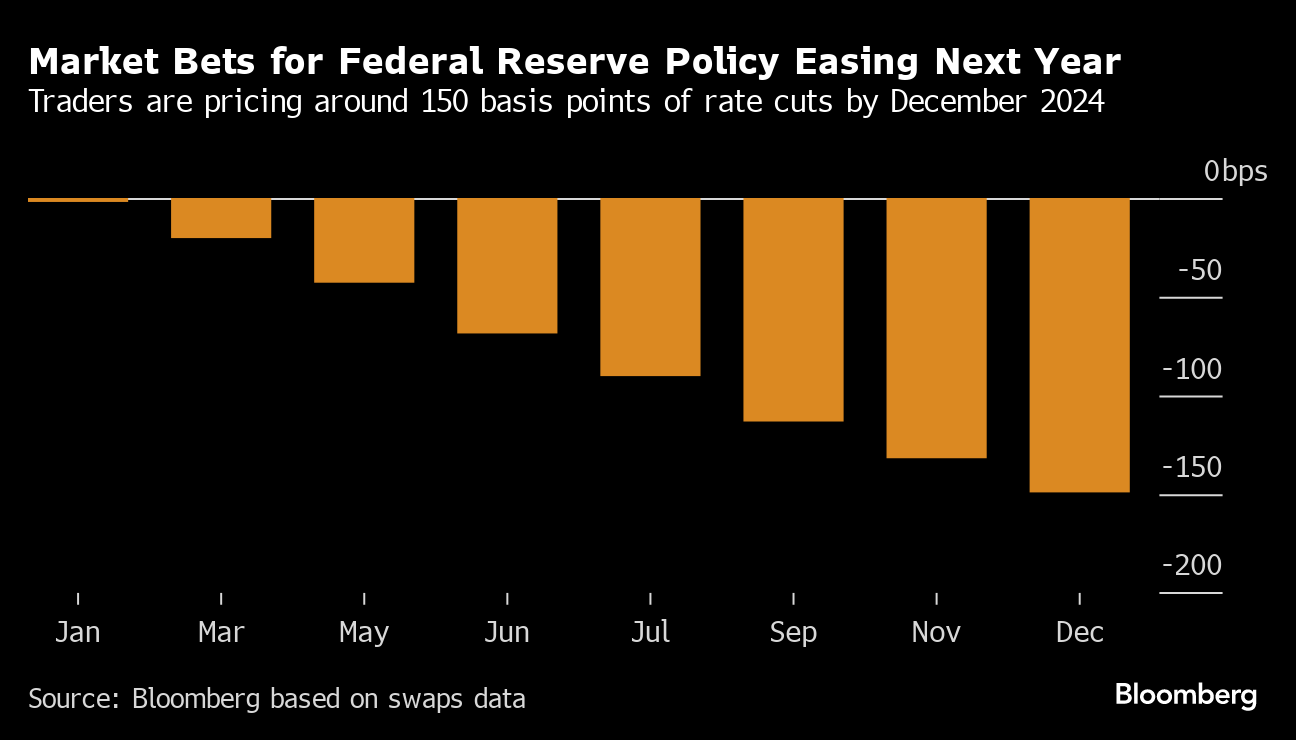

The handful of contrarian views are based on expectations that the rest of the world will struggle more with higher interest rates than the US and lurch closer to a recession. While the Federal Reserve has indicated its plans to cut interest rates by 75 basis points in 2024, dollar bulls expect similar or even quicker reductions in other major economies from Europe to emerging markets leading to wider rate differentials.

“It is peculiar that the consensus thinks the US dollar will be the loser in 2024,” said Paul Mackel, global head of FX research at HSBC. “A number of scenarios point to dollar resilience but only a global soft landing delivers a clear dollar bear case.”

A weaker dollar in 2024 is the majority view among analysts surveyed by Bloomberg across the Group-of-10 nations and emerging markets. All but one currency in the Dollar Index and the broader Bloomberg Dollar Spot Index, which includes EM, is expected to gain.

Those expectations may be missing how the dollar typically benefits from flight to safety flows, and the relative weaker growth dynamics outside of the US.

“We do think that Europe and the UK are closer to recession,” said George Efstathopoulos, a Fidelity money manager who is positioned for further greenback strength against the euro and sterling. “It's clear that the dollar always get a bid when this happens” as it becomes a haven, he said.

Some Wall Street banks also agree, with Morgan Stanley predicting that the Dollar Index — which measures it against six Group-of-10 peers — will climb to 111 by spring from around 102 now. JPMorgan strategists including Meera Chandan see the gauge rising 3% in the first half.

“The ‘stronger for longer' USD path incorporates US outperformance across a variety of metrics,” strategists including David Adams, Morgan Stanley's head of G-10 FX strategy, wrote in a report published Nov. 13. These include the prospect of earlier and faster European Central Bank easing, which would keep rate differentials in the dollar's favor, he added.

To be sure, market expectations for US rate cuts have surged following the Fed's signaling of a pivot on Wednesday. Traders are pricing in 131 basis points of US rate cuts over the next year, up from under 100 basis points before the policy meeting. That's currently in line with the 137 basis points of cuts seen for the ECB but trails emerging-market central banks from Mexico to Brazil.

ECB officials indicated on Thursday they're still concerned about inflation and aren't thinking of easing.

Loomis's Lynda Schweitzer favors the US currency as a hedge. “It's just on a relative basis and on our view that a global slowdown is coming, we feel better about being slightly long the dollar versus other currencies,” said the money manager, who is shorting the yuan, sterling and euro. Still, in the near term, the firm has reduced its long dollar positions, she said, citing the continued resilience of the US economy.

For Efstathopoulos, the dollar is also attractive as a diversification given the elevated correlation between bond and equities.

Risk Premium

JPMorgan contends geopolitical tensions will support the dollar as the US election takes center stage in 2024. If current polling holds, risks for the currency will be skewed to the upside given the possibility of new trade tariffs.

Any future expansion of US tariffs on nations and trading blocs beyond China would have an outsized effect, strategists including Chandan wrote in a Nov. 27 note. A universal 10% tariff may boost its trade-weighted value by 4% to 6% as a widening trade war weighs on pro-cyclical, growth-sensitive currencies.

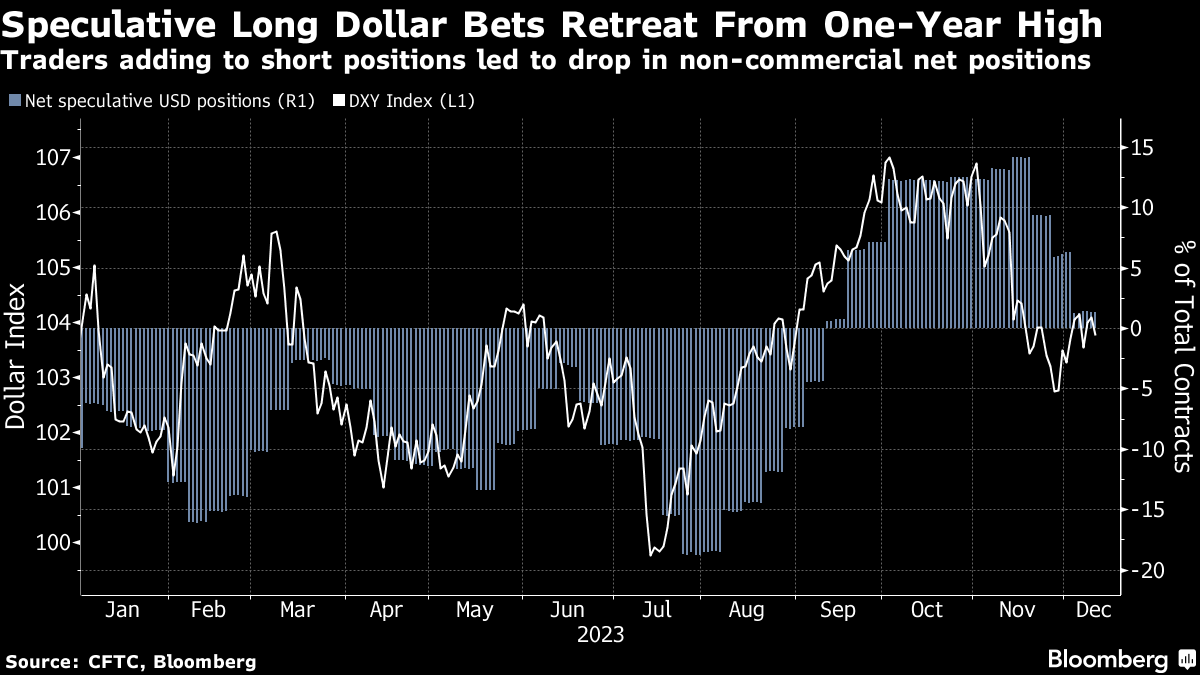

While non-commercial net positions in the dollar — a proxy for speculative positioning — retreated from a one-year high, market participants are still overall long, according to data from the Commodity Futures Trading Commission.

Read more: US Election Risk Is Starting to Build in Global Currency Markets

Others though expect the greenback to decline more — it gained in 2021 and 2022 and is set to end this year slightly weaker — as the Fed begins cutting interest rates.

“The game changer top down would be a US recession,” said Monica Defend, head of Amundi Institute, part of Europe's largest asset manager, who expects the yen to climb to 135 per dollar by year-end. “The dollar would be vulnerable to pullbacks as the Fed moves from policy tightening to policy easing,” she said.

It's a view echoed by Bhanu Baweja, who forecasts that the euro could rally to at least as high as 1.15 by year-end from around 1.09 now. “Interest-rate differentials contracting against the US is probably going to be the primary force,” said the UBS Investment Bank strategist who has priced in 275 basis points of Fed rate cuts next year.

A rate increase in Japan — a prospect that markets are pricing in for next year — will boost the yen as higher yields increase the appeal of Japanese assets. The yen is at around 142 per dollar.

Meanwhile, BlackRock Inc., the world's largest asset manager, is braced for the dollar to stay range-bound from here.

“We are fairly neutral in our dollar allocation and are not positioning for a big move in either direction,” said Russ Koesterich portfolio manager for BlackRock's global allocation fund. “Our base case is a modest slowdown in US growth and a further deceleration in inflation. We also expect that the Fed is done hiking and will begin cutting rates sometime in Q2 or Q3.”

What Bloomberg Strategists Say...

With global borrowing costs set to stay elevated for some time, it appears problematic to restrict the focus just to the expected rate of change in yields. Differentials will need to narrow a lot more to lead to a sustained dollar pivot.

Mary Nicola, Markets Live strategist

Even so, calls that the dollar has peaked were premature earlier in the year. It put on an unexpected run from July to October when cooler-than-expected US inflation data fueled hopes the Fed would soon wrap up its rate-hike cycle. The Bloomberg dollar gauge then tumbled almost 3% last month as Fed officials signaled they're probably done with raising rates.

Yet, the speed and magnitude of the dollar's recent fall isn't a guarantee for further dramatic weakening ahead, according to Goldman Sachs and Vanguard Asset Management Ltd, who forecast only a shallow decline ahead. Before the Fed meeting, Goldman had forecast a 3% drop in the dollar index over the next twelve months, while Vanguard projects a decline of just over 1%.

“Next year, it's more about what the other side of the equation — what Europe, the UK, China and Japan — are doing,” said Richard Benson, co-chief investment officer at Millennium Global Investments, who predicted at the start of this year that the dollar would weaken. “I don't think one big thing is going to move from the beginning of the year to the end.”

--With assistance from Edward Bolingbroke.

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.