(Bloomberg) -- The rally in stocks driven by the Federal Reserve's dovish tilt and bets on a soft economic landing lost a bit of steam Thursday amid speculation the market has run too far, too fast.

After a surge that put the S&P 500 within a striking distance of its all-time high, the gauge saw a small gain as valuations and “overbought” levels suggest equities are vulnerable to a pullback. The Nasdaq 100 fell after an over 50% surge in 2023. Wall Street's “fear gauge” — the VIX — pushed further away from an almost four-year low. Piles of derivatives contracts tied to stocks and indexes were due to mature Friday — which could amplify instability.

“We are a little nervous about the weeks ahead,” said Callie Cox at eToro. “Stocks are in need of a serious heat check. We haven't seen a 1% pullback in the S&P 500 since late October. The rate cut trade has been strong, but don't be surprised if we see it cool off. It shouldn't change your views about the favorable environment we're in.”

Treasuries rose, sending the 10-year yield below 4%. The dollar fell against all of its developed-market peers. The move was partly driven by gains in both the euro and the pound after Europe's central bankers signaled they are in no hurry to join the US pivot toward interest-rate cuts.

From stocks to Treasuries, credit to commodities, everything saw big gains in the previous session — when the Fed projected more rate cuts in 2024 and Chair Jerome Powell refrained from pushing back against Wall Street's dovish trade.

The scope and intensity of such rally can be illustrated by a measure that tracks the lowest return of the five major exchange-traded funds following these assets. With gains of at least 1%, the pan-asset advance beat all other Fed days since March 2009.

Matt Maley at Miller Tabak + Co. highlighted the fact that both the bond and stock markets are becoming quite overbought on a short-term basis — and could see some sort of near-term pullback before long.

“Pick any old famous phrase you'd like: ‘Sell the news'….‘too far, too fast'….‘normal/healthy breather after a big rally',” Maley said. “Any one of them might end up describing a pullback over the next few days, so investors will have to stay nimble. No market moves in a straight line, and after such a big rally, we could see some profit taking for a few days.”

Bloomberg's latest Instant Markets Live Pulse survey showed investors expect the S&P 500 to rise to about 4,835 at the end of 2024, an increase compared to the last survey before the Fed decision. Still, such a gain, which amounts to about 2.5% from the current level, reflects skepticism about how much US stocks can rally after this year's advance of over 20%.

Similarly modest gains are seen for the bond market: The median call in the survey was for the 10-year Treasury yield to slide to about 3.8%.

To Fabiana Fedeli at M&G Plc, the biggest data point to watch remains core inflation, how far it's coming down and how central banks reacts to it, “because if inflation doesn't come down enough and to where it should be, the only reason why central banks would cut rates as aggressively as the market expects is because the economy is really degenerating rapidly — and that is not going to be good for risk assets.”

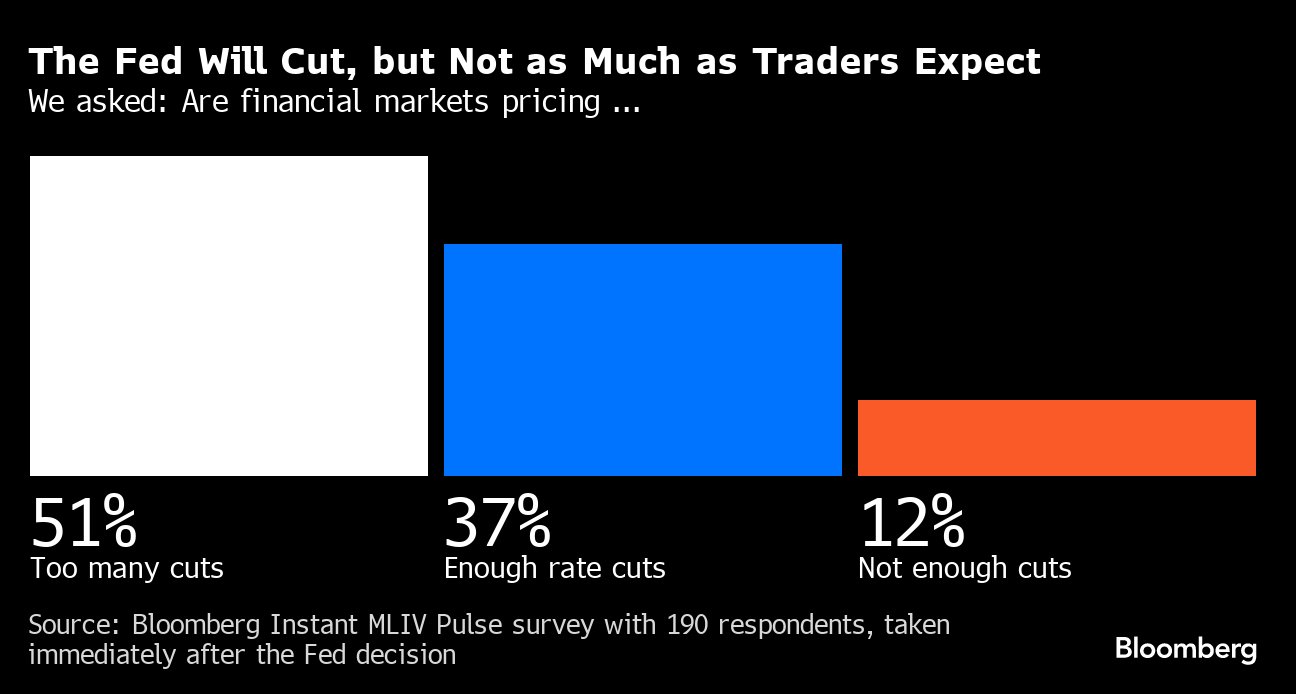

“Our view is that the market is pricing too fast a pace of cuts,” said Solita Marcelli at UBS Global Wealth Management. “We think the experience of this rate cycle is that it pays to listen to the Fed. Our base case forecasts the Fed will refrain from further rate hikes and will start trimming rates by the middle of 2024, delivering 75bps in cuts by the end of next year.”

Some of the biggest names in the bond world are at odds about just how far Treasuries can rally now the Fed has signaled a pivot toward rate cuts.

Jeffrey Gundlach at DoubleLine Capital says US 10-year yields will fall toward the low 3% range as the central bank is likely to slash its cash-rate target by a full two percentage points next year. Former Pacific Investment Management Co. bond king Bill Gross dismissed such euphoria, saying the yield is already about where it should be at just on 4%.

Credit markets face a dramatic repricing in 2024 as higher capital costs slam lower-rated borrowers, according to JPMorgan Asset Management's Oksana Aronov.

“The interest rate reckoning took its time to arrive — I think the credit reckoning will as well,” the chief investment strategist for alternative fixed income said in an interview on Wednesday. “There is going to be a big one, just as there was a big one in interest-rate risk.”

Economists at some of Wall Street's biggest banks are now calling for the Fed to roll out rate cuts earlier and faster next year, emboldened after the central bank's last meeting of 2023 set off fireworks across financial markets.

At Goldman Sachs Group Inc., economists see a steady course of interest-rate cuts that begins in March. Barclays Plc is now calling for three cuts in 2024, from just one seen ahead of this week's Fed meeting. And JPMorgan Chase & Co. bumped its view on the start of the easing cycle to June from July.

Corporate Highlights:

- Intel Corp., the biggest maker of personal computer processors, announced new chips for PCs and data centers that the company hopes will give it a bigger slice of the booming market for artificial intelligence hardware.

- Billionaire activist investor Nelson Peltz has proposed two nominees for the board of Walt Disney Co., himself and the former chief financial officer of the media and entertainment giant.

- Tesla Inc.'s showdown with trade unions across the Nordic region is threatening to spill over to the financial markets after a group of pension funds and asset managers sent a letter to Elon Musk urging him to change course.

- UBS Group AG has stepped up an effort to recoup hundreds of millions in cash bonuses that Credit Suisse paid to retain dealmakers before the lender's collapse.

- Kroger Co. and Albertsons Cos. are bracing for a US Federal Trade Commission lawsuit over their proposed $24.6 billion tie-up as soon as January as opposition builds against the supermarket mega-deal.

- Vivendi SE is considering options for its €1.3 billion ($1.4 billion) stake in former phone monopoly Telecom Italia SpA as billionaire Vincent Bolloré explores a reorganization of the French conglomerate, people familiar with the matter said.

- A personalized vaccine developed by Merck & Co. and Moderna Inc. helped prevent the recurrence of severe skin cancer for three years in promising new results from a study.

Key events this week:

- China 1-yr MLF rate and volume, property prices, retail sales, industrial production, jobless rate, Friday

- Eurozone S&P Global Manufacturing PMI, S&P Global Services PMI, Friday

- US industrial production, Empire manufacturing, S&P Global US Manufacturing PMI, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 rose 0.3% as of 4 p.m. New York time

- The Nasdaq 100 fell 0.1%

- The Dow Jones Industrial Average rose 0.4%

- The MSCI World index rose 1%

Currencies

- The Bloomberg Dollar Spot Index fell 0.8%

- The euro rose 1.1% to $1.0991

- The British pound rose 1.2% to $1.2769

- The Japanese yen rose 0.7% to 141.82 per dollar

Cryptocurrencies

- Bitcoin fell 0.1% to $42,941.6

- Ether rose 1.3% to $2,290.92

Bonds

- The yield on 10-year Treasuries declined 11 basis points to 3.91%

- Germany's 10-year yield declined five basis points to 2.12%

- Britain's 10-year yield declined four basis points to 3.79%

Commodities

- West Texas Intermediate crude rose 3.2% to $71.71 a barrel

- Spot gold rose 0.4% to $2,036.36 an ounce

This story was produced with the assistance of Bloomberg Automation.

--With assistance from Richard Henderson, John Viljoen, Kasia Klimasinska, Lu Wang, Michael Msika, Macarena Muñoz, Sagarika Jaisinghani and Geoffrey Morgan.

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.