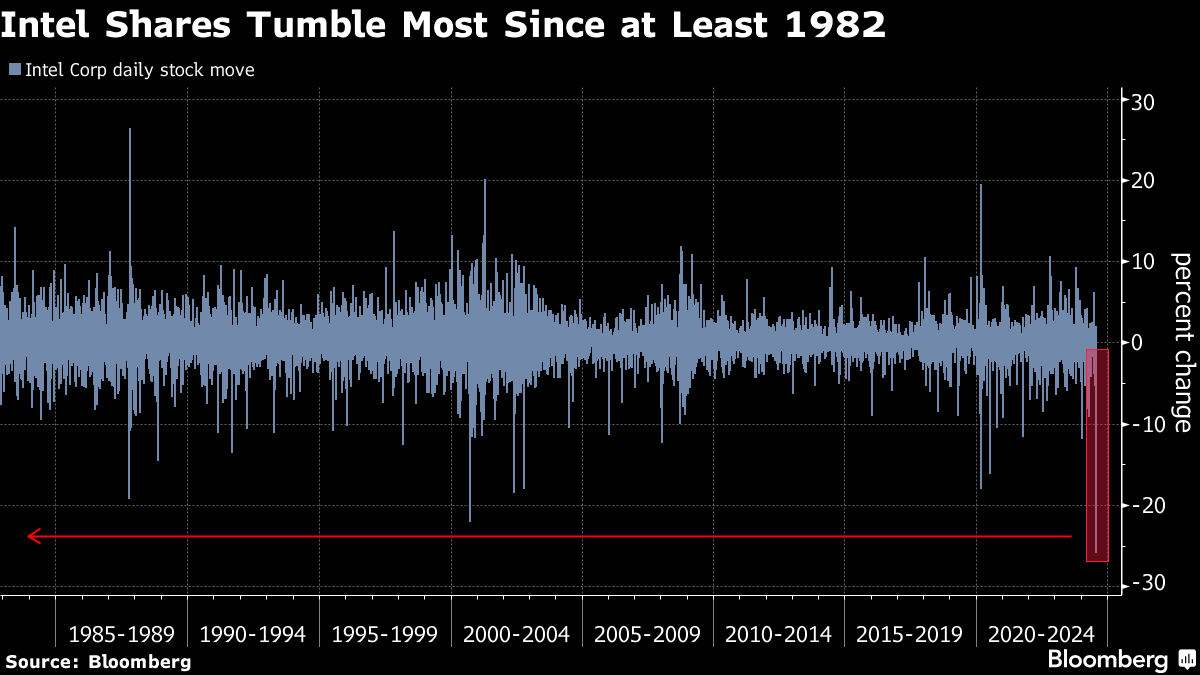

(Bloomberg) -- Intel Corp. shares suffered their largest decline in over 40 years after the company gave a grim growth forecast and laid out plans to slash 15,000 jobs, signaling that the chipmaker is ill-equipped to compete in the artificial intelligence era.

The shares fell more than 26% after trading opened in New York on Friday, wiping out about $32 billion in market value. This marks the stock's biggest biggest intraday drop since since at least 1982, according to data compiled by Bloomberg.

Sales for the current quarter will be $12.5 billion to $13.5 billion, the company said Thursday. Analysts had projected $14.38 billion on average, according to data compiled by Bloomberg. Intel will have a loss of 3 cents a share, excluding certain items, versus expectations for a profit of 30 cents.

Intel said it plans to cut more than 15% of its workforce of around 110,000 people. It's also suspending dividend payments to shareholders starting in the fourth quarter, and will continue that until “cash flows improve to sustainably higher levels,” according to the statement. The company has paid a dividend since 1992.

“I have no illusions that the path in front of us will be easy,” Chief Executive Officer Pat Gelsinger said in a memo to employees. “You shouldn't either.” He called the moves “some of the most consequential changes in our company's history.”

Gelsinger, despite a massive spending plan to restore Intel to industry prominence, is struggling to improve the company's products and technology fast enough to retain customers. The results underscore a dramatic decline for Intel, which dominated the semiconductor industry for decades and is now forced to tout cost cutting measures and give reassurances that it can fund growth plans.

How US Missed a Chance to Lead in Chipmaking Tech: QuickTake

“Revenue is not where we want it to be,” said Chief Financial Officer Dave Zinsner in an interview. “Financials weren't where we want them to be.” The job cuts were needed “to get us to a place where we have a more sustainable model for the business going forward.”

In the second quarter, the company had a profit of 2 cents a share, excluding certain items, and revenue of $12.8 billion, down 1%. Analysts had estimated a profit of 10 cents a share and sales of $12.95 billion. Wall Street is projecting a modest increase in overall sales this year from 2024, still leaving the company more than $20 billion below its peak in 2021.

Competitors who specialize in artificial intelligence are winning over some of Intel's customers. Nvidia Corp. now has more than twice its former nemesis' quarterly sales. Once a struggling rival, Advanced Micro Devices Inc. is valued more than $100 billion higher by investors and Taiwan Semiconductor Manufacturing Co. is widely recognized as having the industry's best production.

Gelsinger remains confident that Intel is on the right track in the long run. He's argued that Intel's vital manufacturing is on course to catch and pass those of rivals and that'll attract outside customers, and justify the string of new plants Intel is building. He thinks Intel has paid what it needs to catch up to the industry, and now can focus on its finances.

Some of Intel's best chips are manufactured by others. Over time, the company hopes to shift more of its chip manufacturing to its own plants, which are being upgraded. The company is also working to accelerate improvements in chips for AI PCs. But for now, the expenses are squeezing gross margins, Zinsner said.

Gross margin, or the percentage of sales remaining after deducting the cost of production, was 35.4% in the quarter. That measure will stay flat in the current quarter. At its peak, Intel regularly reported gross margin of well above 60%.

The company is reducing its spending on new plants and equipment in 2024 by more than 20%, and is now budgeting between $25 billion and $27 billion. Next year, expenses will range between $20 billion and $23 billion.

Most of the job reductions, needed also to remove bureaucracy and speed up decision making, will be completed by the end of the year, Gelsinger told staff.

“Our costs are too high, our margins are too low,” he wrote in the memo, saying he would take employee questions at an internal meeting. “We need bolder actions to address both — particularly given our financial results and outlook for the second half of 2024, which is tougher than previously expected.”

Intel was forced to reduce its sales expectations in May after the US government revoked its license to supply chips to China's Huawei Technologies Co., part of Washington's push to cut off that company for what it alleges are national security risks.

The chipmaker is reporting earnings for the second time under a new business structure that shows the financial performance of its manufacturing operations. Gelsinger has said the restructuring was a necessary step to make operations more efficient and competitive.

The company reports revenues divided between product groups and its manufacturing operations, with factories undergoing a massive upgrade and a build-out program that's weighing heavily on profits.

Revenue is improving at what it calls its Foundry unit, gaining 4% from a year earlier to $4.32 billion. PC chips also posted growth, up 9% from the same period a year earlier.

Sales at the crucial data center unit, once the most profitable, again lost ground, declining 3% to $3 billion. That unit hasn't yet achieved anything like the market presence of Nvidia in accelerator chips used in artificial intelligence systems. AI is proving a gold mine, and cutting into spending on the type of processor Intel makes.

--With assistance from Subrat Patnaik.

(Updates share price and stock chart, and adds market-value loss.)

More stories like this are available on bloomberg.com

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.