Investors have a challenge in betting on the usual stock market rally that tends to arrive after a presidential election: With the S&P 500 Index on track for one of its best ever starts to a year, history can't be a guide this time.

Buying US stocks into year-end following a vote is the classic trading playbook. Historically, the S&P 500 has posted a median return of 5% from Election Day in November to the end of the year, according to data compiled by Deutsche Bank AG. Even the riskiest pockets like small-capitalization companies typically catch a bid in the rising tide.

But this is hardly a classic election year. The S&P 500 is up 25% in 2024 after leaping 24% in 2023, putting the index on pace for its first back-to-back years of more than 20% gains since the late 1990s. As a result, share prices are high, with the S&P 500 trading at more than 22 times projected 12-month earnings, compared with an average reading of 18 in the last decade. And positioning data shows traders are already heavily invested in equities.

Meanwhile, familiar foes from the past few years, rising bond yields and the threat of persistent inflation, loom in the background. All of which has the stock market set up for a potentially quiet holiday season — as opposed to the ragers of election years past.

“With valuations elevated and the S&P 500 already near 6,000, the market will creep higher from here,” said Eric Beiley, executive managing director of wealth management at Steward Partners. “But I don't see a big year-end rally because rising yields will keep investors at bay.”

No Hurry

The Federal Reserve has lowered interest rates twice since September. But recently, central bankers indicated that they aren't in a hurry to go further.

At the same time, Treasury yields have jumped to multi-month highs after US president-elect Donald Trump's election victory ignited bets that his economic plans like large import tariffs and mass deportations of low-wage undocumented workers could stoke inflation and hurt growth, possibly reducing the Fed's scope to cut interest rates. This explains why Wall Street strategists have been dialing back their rate reduction expectations since Trump's election victory.

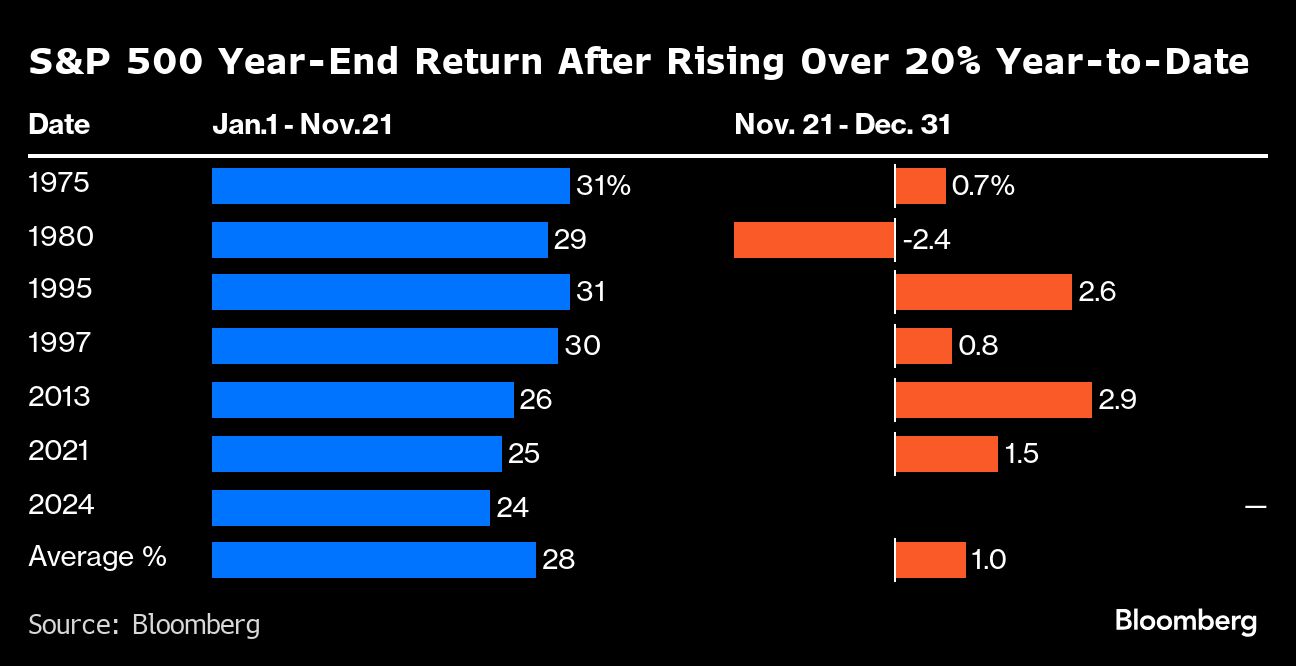

The six months from November to April are historically the best part of the year for US equities because companies and pension plans tend to increase their stock buying starting on Nov. 1, according to the Stock Trader's Almanac. However, those year-end rallies typically aren't as robust when the S&P 500 has already risen at least 20%. In that case, since the 1970s the average return from now to Dec. 31 has been roughly 1%, according to data compiled by Bloomberg.

Of course, this bull-market rally has gone far beyond these levels, with the S&P 500 up almost 70% since bottoming in October 2022. That will curb gains into late December, according to Savita Subramanian, head of US equity and quantitative strategy at Bank of America Corp.

“Sentiment and positioning based on at least five indicators have grown dangerously bullish, leaving less room for positive surprises,” she wrote in a note to clients on Nov. 15.

Heavy Hedging

Already, some of the riskiest parts of the market are showing signs of weakness. Small-cap stocks, for instance, have erased most of their post-election rally as concern grows about the Fed's rate path. And uncertainty over higher borrowing costs is prompting investors to hedge against sharp declines. Demand for far out-of-the-money put options on the S&P 500, technology-heavy Nasdaq 100 Index and small-cap Russell 2000 Index has risen to levels last seen during the heavy volatility ahead of the election, according to Kevin Brocks of 22V Research.

That said, the rally isn't necessarily in jeopardy simply because there's growing speculation that the market has run too far. Valuations and investor sentiment can stay frothy for weeks — even months — before stocks suffer a significant drop, said Max Kettner, chief multi-asset strategist at HSBC Bank Plc, adding that there are “very few reasons to suggest a year-end rally has already been front-loaded.”

Indeed, investors keep funneling money into stocks: They put $16.4 billion into US equities in the week through Nov. 20, marking the seventh consecutive weekly inflow, according to a Bank of America note citing EPFR Global data.

The optimism isn't entirely surprising. Looking at history, the S&P 500's advance over the past two years isn't even half of the 143% average gain in the 16 prior bull runs since 1945, according to Birinyi Associates.

What investors most want to see when judging the rally's strength is the gains broadening beyond the megacap tech that have been powering indexes higher on enthusiasm for artificial intelligence. It's starting to happen, as the S&P 500 Equal Weight Index is outperforming the regular market-cap weighted version of the benchmark since Election Day, with financials, energy and consumer discretionary shares leading the way.

In the end, however, it may be the bond market that sends the loudest signal for stock prices. If Treasury yields stay high and the Fed stands pat, there are serious risks to betting on significant further gains in equities.

“A broadening rally is crucial but the one thing standing in the way of a strong advance for stocks the rest of the year is the bond market,” said Jamie Cox, managing partner at Harris Financial Group. “That may ultimately put a lid on a hefty year-end rally.”

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.