011123-2.jpg?downsize=773:435 "HDFC Bank's Slower Loan Growth Could Be A Risk To Estimates, Say Analysts Ahead Of Q2 Results")

HDFC Bank's pre-earnings business update for the quarter ended September has raised concerns of a softer loan growth among analysts. However, they await the bank's September-quarter numbers before any rerating.

According to provisional numbers disclosed to exchanges, the lender's gross advances for the quarter ended September witnessed a rise of 1.3% on quarter and 7% year-on-year to Rs 25.2 lakh crore. Deposits, which have been lagging credit growth, grew 3.1% on quarter and 15.4% on year to Rs 23.5 lakh crore.

Nomura, Morgan Stanley, and Jefferies have maintained their rating and kept their target prices unchanged. Nomura has a 'neutral' rating for the stock with an unchanged target of Rs 1,720, implying a 3.8% upside; Jefferies has a 'buy' with target of Rs 1,682.15, implying a 1.5% upside, and Morgan Stanley has an 'overweight' rating with target of Rs 1,850, implying an upside of 11.6%.

Jefferies' report said loan growth was modest at 7% on annual basis and 1% sequentially, reflecting slower growth & securitisation; this may be risk to estimates. At the same time, it added, "We feel sector deposit growth has improved at end of quarter aiding better growth for most banks."

According to Nomura, the moderation in loan growth was led by the wholesale segment and retail loan growth was relatively better at 15% year-on-year. "The commercial and rural banking segment continued to be the key driver of loan growth," it said.

It added that the bank's return on equity improvement will be a gradual process, and will come at the cost of loan growth, and that it sees limited upside.

The brokerage's medium-term outlook for the bank is expected to stay soft as it factors in soft loan growth of 8%/10.5% over FY25-26. "FY27 loan to deposit ratio at 91% in our estimates continues to be higher than the 85-87% seen pre-merger (which is the bank's stated medium-term target)," it added.

Morgan Stanley noted some of the downside risks for its call including a sharp slowdown in economic growth weighing on loan growth and resulting in higher non performing loans, weaker-than-expected progression on deposits growth/margins, and a higher-than-expected impact of the ECL and LCR guidelines.

"We await more details from the financial results — scheduled for 19 October 2024 — on margins, term deposit progression (retail vs. wholesale), and asset quality," it said.

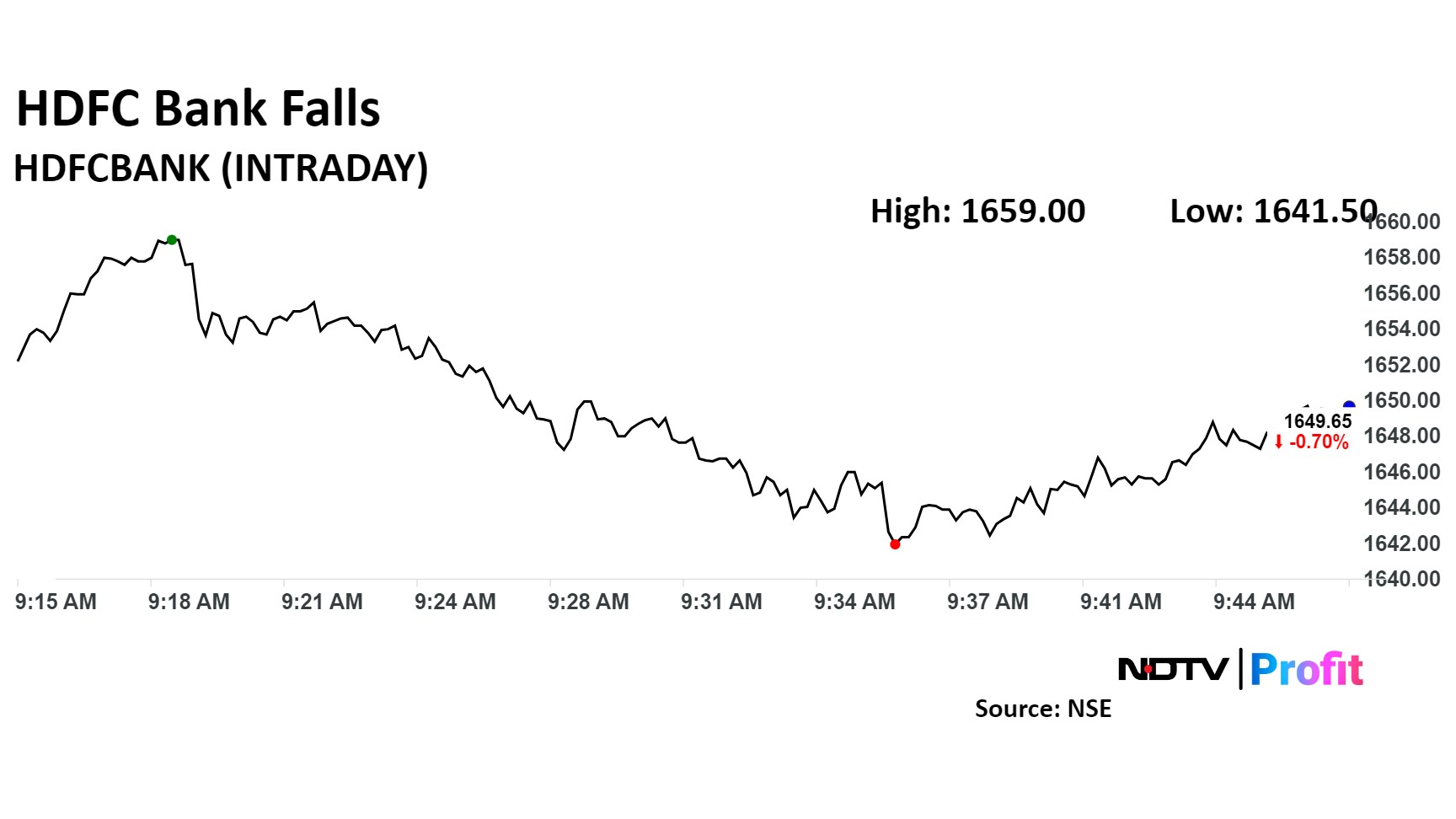

HDFC Bank share price fell as much as 0.97% to Rs 1,641.50 apiece, the lowest level since Sept. 11. It pared losses to trade 0.5% lower at Rs 1,649.25 apiece, as of 9:49 a.m. This compares to a 0.1% advance in the NSE Nifty 50 Index.

It has fallen 3.5% on a year-to-date basis and risen 11.7% in the last 12 months. Total traded volume so far in the day stood at 0.42 times its 30-day average. The relative strength index was at 39.42 .

Out of the 47 analysts tracking the company, 38 maintain a 'buy' rating, and nine recommend a 'hold', according to Bloomberg data. The average 12-month consensus price target implies an upside of 8.5%.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.