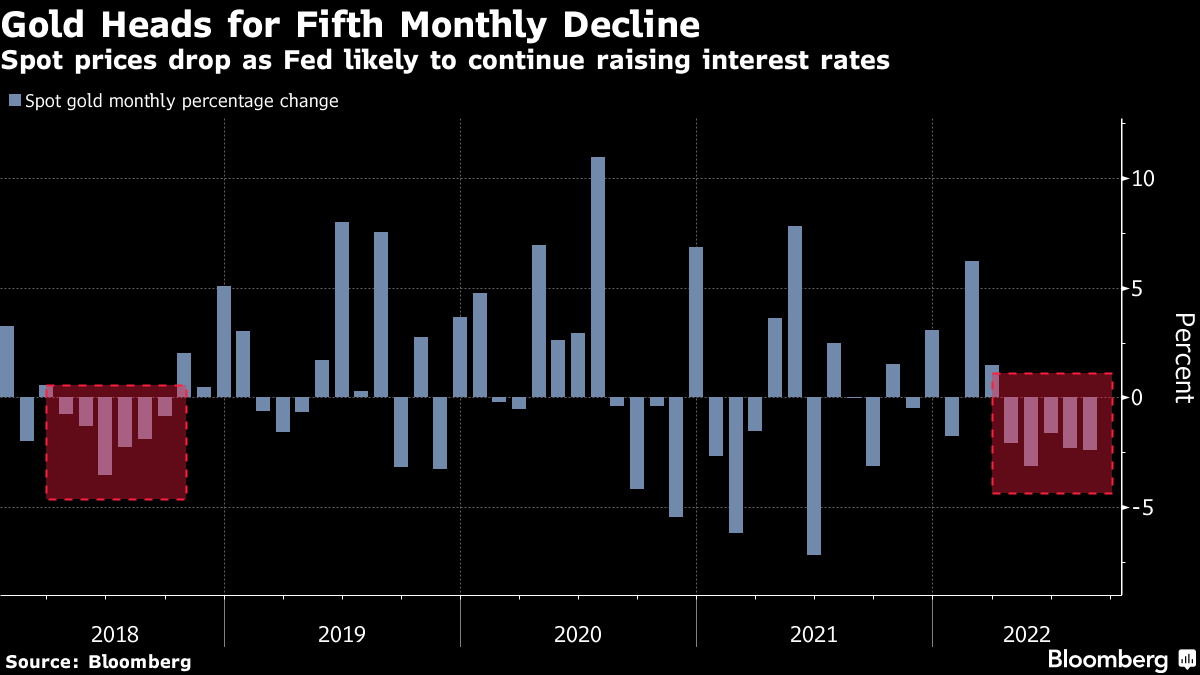

(Bloomberg) -- Gold headed for a fifth straight monthly drop, the longest losing run in four years, as speeches by Federal Reserve officials indicate the central bank will keep monetary policy tight for some time.

The metal briefly pared losses Wednesday as the greenback fell back after ADP Research Institute showed US companies had the smallest increase in private payrolls since the start of 2021.

Gold has been extending a run of losses since a speech last week by Fed Chair Jerome Powell, which stressed the central bank's commitment to reining in inflation. Gold is now down more than 6% in 2022, having come close to a record high when Russia's invasion of Ukraine stoked demand for haven assets.

Other officials struck a similarly hawkish tone. New York Fed chief John Williams said Tuesday interest rates probably need to advance above 3.5% at some point to contain price pressures. Separately, Richmond Fed President Thomas Barkin said the central bank will “do what it takes” to curb inflation.

Meanwhile, Atlanta counterpart Raphael Bostic called the duty to curb inflation “unshakable,” but also said he'd be open to dialing back the pace of increases if prices cooled.

Officials have been vague on how big their policy move will be at the rate decision meeting in September. There are fresh signs of robustness in the economy, with job openings and a consumer confidence gauge both topping forecasts, pointing to strength in household and labor demand that risks sustaining inflationary pressures and raises the prospects for a third straight 75 basis point interest rate hike.

The ADP Research Institute's national employment report showed 132,000 jobs added in August, significantly lower than economists' median forecast. The data will be kept in mind ahead of the government's nonfarm payrolls report on Friday.

Spot gold headed for a fourth-day straight drop, 0.8% down to $1,710.09 an ounce as of 3:57 p.m. in New York after earlier touching the lowest since July 21. Gold is poised to end down 3% in August. Gold futures fell 0.6% to settle at $1,726.20 on the Comex in New York.

The Bloomberg Dollar Spot Index was little changed. Silver fell to the lowest since July 2020, while palladium and platinum edged lower.

Aluminum and copper extended their biggest declines in at least a month as concerns about global growth gripped markets. Both metals fell amid a broad sell-off in commodities that gripped everything from crude oil to agricultural products. Anxiety is high that Europe's energy crisis, tighter monetary policy by the Federal Reserve and China's Covid Zero strategy will hit demand for industrial metals.

Top Copper Nation Extends Supply Slump as Chile Mines Struggle

Aluminum settled 1.3% lower at $2,359.00 a metric ton on the London Metal Exchange as of 5:53 local time. Copper reduced its losses as world's top producer Chile reported a disappointing 8.6% decline in July production from a year ago. The metal fell 0.8% in London to $7,802.00 a ton. Zinc, lead and tin also declined.

(Updates prices)

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.