(Bloomberg) -- Wall Street traders found little encouragement to keep pushing the stock market higher at the start of a week that will bring the last inflation figures before the next Federal Reserve decision.

Equities edged lower on Monday, with investors awaiting more clues on whether the recent uptick in consumer prices was just a blip or an indication that the disinflationary trend has hit a roadblock. After closing at record highs 16 times this year, the S&P 500 is showing signs of overheating, spurring warnings about a near-term consolidation.

“It would be natural to expect some fly in the ointment, some monkey in the wrench, to bring investor expectations back to Earth,” said Jason De Sena Trennert at Strategas. “Stock prices, credit spreads, and the price of gold and Bitcoin suggest that monetary conditions are far from restrictive.”

The S&P 500 closed around 5,118. Boeing Co. extended its 2024 slump to over 25% on a US criminal probe. Meta Platforms Inc. slid almost 4.5%. Tesla Inc. rebounded. In late hours, Oracle Corp. reported strong sales with growth in its closely-watched cloud computing business stabilizing.

Treasuries fell, with traders bracing for another flurry of high-grade corporate debt sales. Bitcoin hit $72,000.

US consumer expectations for inflation over the next three years climbed in February — and increased even more sharply for the five-year horizon, according to a Fed Bank of New York survey. Those figures came ahead of data expected to show inflation probably abated only gradually last month — illustrating why US officials are in no rush to cut rates.

A survey conducted by 22V Research shows 45% of investors expect the market reaction to Tuesday's consumer price index will be “risk-off.” While most are still betting CPI is on a Fed-friendly glide path to 2%, the share of those who think financial conditions would need to tighten rose to 36% from 22%.

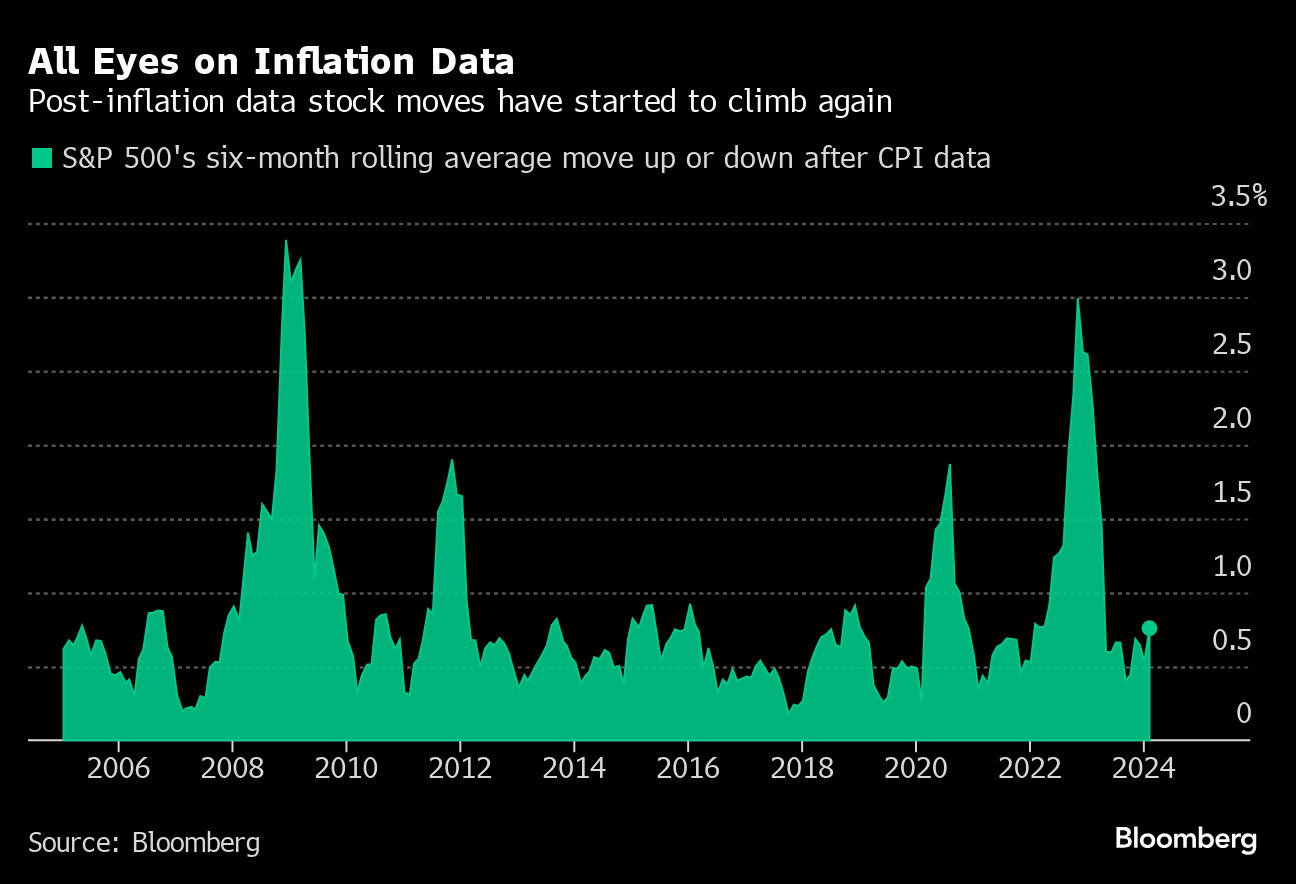

While the S&P 500 has fallen on just four CPI reporting days in the past 12 months, volatility is picking up in those sessions this year. Over the past six months, the equity gauge has moved about 0.8% in either direction on the day CPI has been released, according to data compiled by Bloomberg. That's the most since April and up from less than 0.5% in September.

“Expect more volatility around those releases as investors continue to determine the direction of interest rates,” said Paul Nolte at Murphy & Sylvest Wealth Management.

That sense of wariness has also been amplified by signs of an overstretched market. Not surprisingly, a handful of sentiment indicators are pointing to a growing level of “frothiness,” according to Sam Stovall at CFRA

Among those, he cites the American Association of Individual Investors' survey showing an “unusually high” level of bullishness and the CNN Fear/Greed Indicator that recently registered “extreme greed.”

“Even though the S&P 500 is due for, and would benefit from, a digestion of recent gains, history suggests not waiting too long before adding to holdings,” Stovall added.

To Anthony Saglimbene at Ameriprise, investors are likely already incorporating a lot of good news into stock prices and moving ahead of incoming data that supports the soft-landing narrative.

“Stocks are likely overdue for some consolidation or even an extended period of modest declines at some point in the year,” he noted. “Without a meaningful shift in the fundamental picture, we suspect investors would welcome such a downdraft and treat the event as a buying opportunity.”

Moreover, the rally in US equities that began last year doesn't reflect conditions seen in prior boom-and-bust cycles, such as big gaps between share prices and their values, or the significant use of leverage, according to Bank of America Corp.'s strategists led by Savita Subramanian.

“Sentiment has warmed up on equities since mid-2023, driving our slightly lower level of conviction in an up market, but is nowhere near bullish levels of prior market peaks,” they wrote. “In our view, this bull market has legs.”

Another aspect is that robust profits from some of the tech behemoths have also brought down sky-high valuations. They remain relatively stretched — but are still well below prior peaks.

The “Magnificent Seven” tech stocks, for example, trade near their average price-to-earnings ratio since 2015, data compiled by Bloomberg show. The group comprises Apple Inc., Alphabet Inc., Amazon.com Inc., Meta Platforms Inc., Microsoft Corp., Nvidia Corp. and Tesla Inc.

And the ranks of Wall Street strategists playing down concerns around a bubble in US technology megacap stocks only keeps growing.

The team at JPMorgan Chase & Co. was the latest to flag that valuations of the seven tech giants that have led the record-breaking rally on Wall Street are currently lower relative to the rest of the S&P 500 than the average of the past five years.

“There is a concern over the very strong outperformance of the Magnificent 7, but we note that the group is currently trading less stretched than a few years ago, given earnings delivery,” strategist Mislav Matejka wrote in a note.

For investors questioning how much further the S&P 500 can be powered by that narrow group of shares, breadth in the US stock market has actually been improving. While tech remains in the leadership position, an equal-weighted version of the S&P 500 — where the likes of Nvidia Corp. carry the same heft as Dollar Tree Inc. — has recently hit a record.

“Market action last week pointed to a broadening of investor appetite for stocks,” said John Stoltzfus at Oppenheimer Asset Management. “This brought a mix of some profit-taking among sectors that have performed exceptionally well since the start of the year in addition to a rotation and rebalancing into sectors, market capitalizations, and styles that have lagged in performance.”

To Trennert at Strategas, given the high market's valuations and relatively low 10-year Treasury yields, it is difficult to know how much incremental stock performance can be achieved from current levels.

“We continue to be ‘bullish until the bill comes due' — which we define as higher long-term Treasury yields.”

A bond selloff in February — which pushed Treasury yields to their highs of the year — was due in part to January's hot consumer price data, which showed surprising strength in core services, an area of concern for the US central bank. Since then, traders have once again stepped up their rate cut bets as economic data reinforced the view the Fed may be able to start lowering interest rates later this year.

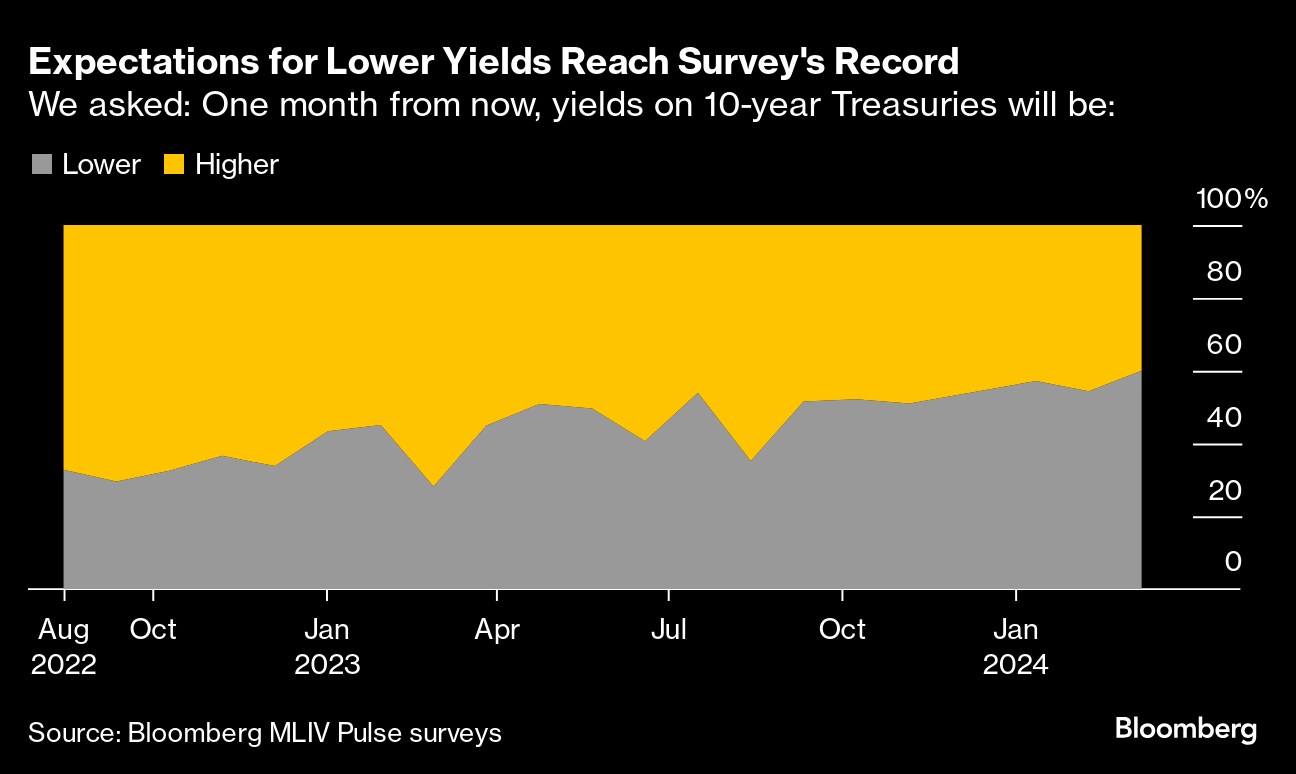

The positive outlook for bonds reached a record high in a Bloomberg's weekly client survey.

Yields on 10-year Treasuries will be lower in a month, according to 60% of 238 respondents in the latest MLIV Pulse poll. That's the strongest vote on bonds since the survey first started asking the question in August 2022. The survey was conducted March 4-8 but closed before the nonfarm payroll data on Friday.

Corporate Highlights:

- Boeing Co.'s crisis of confidence gathered pace, with the shares slumping after the Justice Department opened a criminal investigation into an accident that has thrown the company into disarray.

- MicroStrategy Inc. bought another 12,000 Bitcoin for $821.7 million, the second-largest purchase by the enterprise-software maker since it began acquiring the cryptocurrency almost four years ago.

- Reddit Inc. disclosed further details of what is set to be one of the year's biggest initial public offerings, with the company and some existing shareholders seeking to raise as much as $748 million.

- US natural gas producer EQT Corp. agreed to buy back former unit Equitrans Midstream Corp. for about $5.5 billion in stock, the latest in a flurry of deals in the oil and gas pipeline industry.

Key events this week:

- Japan PPI, Tuesday

- UK Financial Policy Committee quarterly meeting, attended by Bank of England Governor Andrew Bailey, Tuesday

- EU finance ministers meet in Brussels, Tuesday

- ECB Governing Council Member Robert Holzmann, Tuesday

- US CPI, Tuesday

- Eurozone industrial production, Wednesday

- ECB Governing Council member Yannis Stournaras speaks, Wednesday

- Volkswagen, Adidas earnings, Wednesday

- US PPI, retail sales, initial jobless claims, business inventories, Thursday

- China property prices, Friday

- Japan's largest union federation announces results of annual wage negotiations, just ahead of Bank of Japan policy meeting, Friday

- Bank of England issues inflation survey, Friday

- US industrial production, University of Michigan consumer sentiment, Empire Manufacturing, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 fell 0.1% as of 4 p.m. New York time

- The Nasdaq 100 fell 0.4%

- The Dow Jones Industrial Average rose 0.1%

- The MSCI World index fell 0.3%

Currencies

- The Bloomberg Dollar Spot Index was little changed

- The euro fell 0.1% to $1.0927

- The British pound fell 0.4% to $1.2810

- The Japanese yen was little changed at 146.95 per dollar

Cryptocurrencies

- Bitcoin rose 3.7% to $72,021.16

- Ether rose 3.3% to $4,035.31

Bonds

- The yield on 10-year Treasuries advanced two basis points to 4.09%

- Germany's 10-year yield advanced four basis points to 2.30%

- Britain's 10-year yield was little changed at 3.97%

Commodities

- West Texas Intermediate crude rose 0.1% to $78.10 a barrel

- Spot gold rose 0.1% to $2,181.41 an ounce

This story was produced with the assistance of Bloomberg Automation.

--With assistance from Jessica Menton, Matt Turner, Alexandra Semenova and Kasia Klimasinska.

More stories like this are available on bloomberg.com

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.