(Bloomberg) -- Stocks kept pushing higher, adding to a rally from August lows that's already topped $3 trillion amid bets the Federal Reserve will signal it's ready to start cutting interest rates.

All major groups in the S&P 500 rose, with the gauge up for an eighth straight day — the longest winning streak since November. While technology shares led gains on Monday, an equal-weighted version of the US equity benchmark — one that gives Target Corp. as much clout as Microsoft Corp. — hit an all-time high amid hopes the advance will broaden beyond the megacap space. The Russell 2000 of smaller firms added 1.2%.

A bumpy stretch for investors in the dog days of July and August hasn't tempered their zest for equities, with allocations still robust despite a bout of recent volatility. Momentum traders and a surge in corporate buybacks promise to drive a US stock rally over the next four weeks, according to Goldman Sachs Group Inc.'s trading desk.

“The pain trade for equities is higher and the bar for being bearish at the beach into a Labor Day barbecue party is high,” Goldman's Scott Rubner wrote.

Stock volume has been trending lower since the trading spike during the early-August selloff as traders await the Fed's Jackson Hole economic symposium this week and Nvidia Corp.'s earnings on Aug. 28. About 10 billion shares changed hands on US exchanges Monday, 14% below the one-month average.

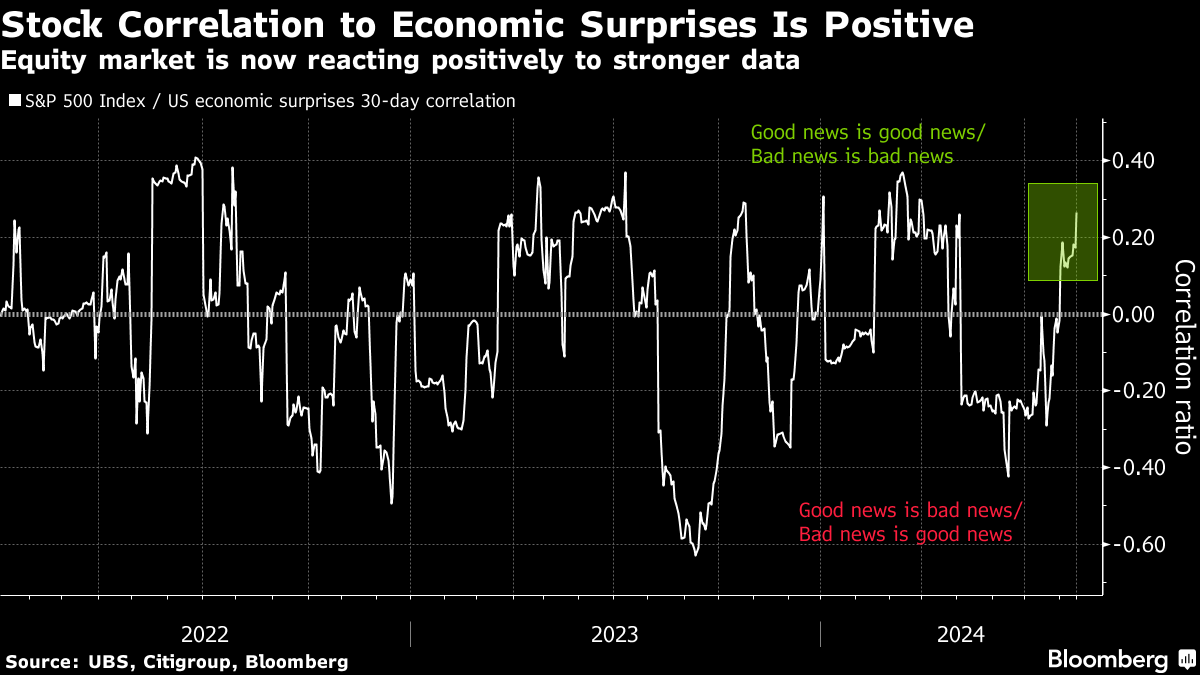

With the central bank approaching a crucial pivot point, it's difficult to overstate how much attention markets will be paying to Jackson Hole. For starters, they're looking for confirmation from Jerome Powell that rates will drop in September. But more drama surrounds what happens after that and the pace of additional cuts over the next several months as the Fed confronts the dual risks to both inflation and employment.

The Fed is unlikely to “out-dove” the market, but as long as growth is “OK,” equities can withstand a less-dovish central bank, according to Ohsung Kwon at Bank of America Corp.

“Stocks just need a nod that growth is going to be supported,” Kwon said. “While our view is that risk is to the upside, we do not believe that Jackson Hole will spur the large equity moves that it has in the past when the Fed used it as forum to telegraph upcoming policy decisions.”

Treasury 10-year yields fell one basis point to 3.87%. The dollar hit the lowest since March. Oil sank 3%. US Secretary of State Antony Blinken said Israeli Prime Minister Benjamin Netanyahu has accepted a cease-fire proposal to halt the war in Gaza and the next step is for “Hamas to say yes.”

To Neil Dutta at Renaissance Macro Research, the Fed is cutting in September, the only question is by how much.

“I don't think Powell is going to greenlight a big move, but he won't torpedo the idea entirely either,” Dutta said. “Powell is likely to acknowledge that the balance of risks has changed, dramatically since the June Summary of Economic Projections. Removing optionality in such a situation is not prudent.”

“So, in this regard, I think the fabled ‘Powell Put' makes a comeback this week,” Dutta said.

All told, Dutta notes the equity market seems “a bit too enthusiastic” relative to the tone of the incoming economic information. Looking ahead, there is good reason to assume the pace of consumers' spending slows, he concluded.

“Investors ‘climbed a wall of worry' as the stock-market relief rally gained momentum,” said Craig Johnson at Piper Sandler. “Equities will likely consolidate ahead of Fed commentary at Jackson Hole this week.”

Equity positioning is back up to moderately overweight, a week after sliding to underweight, according to Deutsche Bank AG strategists including Parag Thatte and Binky Chadha, who said exposure remains well below the mid-July highs at the top of the historical band.

Recent economic data and earnings readouts have reinvigorated confidence among JPMorgan Chase & Co. traders that US stocks can rally into the end of the year.

“While upside appears to be more muted than when we adopted this stance earlier this year, there remains material upside,” the team led by Andrew Tyler wrote.

The trajectory for stocks is likely to be dictated by the week-to-week cadence of macroeconomic data until August's key jobs report, due in the first week of September, according to Morgan Stanley strategists led by Michael Wilson.

“The true test for the market will be the August jobs report,” they wrote. “A strong jobs report that reverses July's softness will provide confidence that growth risks have subsided for now. Another weak report would likely lead to growth concerns resurfacing.”

“While we do remain generally bullish, we don't see a straight line up in the market, as the economy is slowing and there will likely be a mix of conflicting economic data points over the coming months, which is set to continue this recessionary debate,” said Greg Marcus at UBS Private Wealth Management.

Marcus believes the Fed is on track to cut interest rates by 25 basis points in September, barring a significant shock to the downside between now and then.

“Investors should be extending duration with their cash holdings in preparation for rate cuts,” he said. “It's important to diversify within US stocks and prepare for a broadening out in the market, as we believe this broadening of market participation is likely to include value stocks and small caps.”

In past rate-cut cycles, growth stocks have a better rate of outperformance over value across both large and small caps — but on median, they've fallen more, according to Bloomberg Intelligence strategists Gina Martin Adams and Michael Casper.

Likewise, defensive sectors have had the edge over cyclicals. Measuring Fed rate cut cycles from the date of the first cut to that of the last one shows large-cap value posting a median 2.4% drop versus a 24.5% decline for growth — though the latter led in four of five instances. In the Russell 2000, value posted a median 2.7% gain to growth's 21.5% drop, again with the latter ahead in three of five cut cycles.

However, across each cut cycle, S&P 500 staples, health care and communications had the most consistent performance while energy and industrials struggled most often. Russell 2000 communications and health care fared best while real estate and energy struggled.

Corporate Highlights:

- Palo Alto Networks Inc. rose after issuing a quarterly profit outlook that beat Wall Street's expectations and boosting its share buyback program.

- Advanced Micro Devices Inc. agreed to buy server maker ZT Systems in a cash and stock transaction valued at $4.9 billion, adding data center technology that will bolster its efforts to challenge Nvidia Corp.

- Estée Lauder Cos. is forecasting annual revenue growth below analysts' expectations, a sign that the cosmetics company's long-awaited recovery has hit another roadblock.

- Sonder Holdings Inc. soared after the alternative-lodging company reached a series of deals to raise capital and integrate its brand into Marriott International Inc.'s system.

- Kroger Co. is seeking to block the Federal Trade Commission's in-house case against its proposed purchase of rival grocer Albertsons Cos., claiming the proceeding is unconstitutional.

- General Motors Co. is cutting more than 1,000 software engineers as the automaker moves to lean up its software and services organization, said a person familiar with the matter.

- Circle K operator Alimentation Couche-Tard Inc. made a proposal to take over much larger rival and 7-Eleven owner Seven & i Holdings Co., in what would be the biggest foreign takeover of a Japanese company. A merger would create the world's top operator of roughly 100,000 convenience stores.

Key events this week:

- China loan prime rates, Tuesday

- Eurozone CPI, Tuesday

- US Fed minutes, BLS preliminary annual payrolls revision, Wednesday

- Eurozone HCOB PMI, consumer confidence, Thursday

- ECB publishes account of July rate decision, Thursday

- US initial jobless claims, existing home sales, S&P Global PMI, Thursday

- Japan CPI, Friday

- Bank of Japan Governor Kazuo Ueda to attend special session at Japan's parliament to discuss July 31 rate hike, Friday

- US new home sales, Friday

- Fed Chair Jerome Powell speaks at Jackson Hole symposium in Wyoming, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 rose 1% as of 4 p.m. New York time

- The Nasdaq 100 rose 1.3%

- The Dow Jones Industrial Average rose 0.6%

- The MSCI World Index rose 1%

- Bloomberg Magnificent 7 Total Return Index rose 1.7%

- The Russell 2000 Index rose 1.2%

Currencies

- The Bloomberg Dollar Spot Index fell 0.5%

- The euro rose 0.5% to $1.1083

- The British pound rose 0.4% to $1.2990

- The Japanese yen rose 0.7% to 146.65 per dollar

Cryptocurrencies

- Bitcoin fell 1.4% to $58,958.52

- Ether fell 2.2% to $2,606.68

Bonds

- The yield on 10-year Treasuries declined one basis point to 3.87%

- Germany's 10-year yield was little changed at 2.25%

- Britain's 10-year yield was little changed at 3.92%

Commodities

- West Texas Intermediate crude fell 2.9% to $74.41 a barrel

- Spot gold was little changed

This story was produced with the assistance of Bloomberg Automation.

--With assistance from Lu Wang, Natalia Kniazhevich, Michael Msika, Cecile Gutscher and Matthew Burgess.

More stories like this are available on bloomberg.com

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.