Even as Tata Motors Ltd.'s shares rose to a record high after its proposal to split the passenger and commercial vehicle units, analysts say that the spinoff is unlikely to boost valuations in the short term.

The demerger into two separate listed companies may not result in any immediate change in the street's valuation approach, according to Nomura. This is because commercial vehicles, Jaguar Land Rover and passenger vehicle divisions are already "well run and have good disclosures".

The research firm, however, sees the two businesses pursuing their respective strategies with greater freedom in the medium term.

Investec also does not foresee a "significant impact on the valuation". According to JPMorgan, however, the demerger might lead to better value discovery.

The move is aimed at unlocking value as the company's EV push will require more investments, analysts told NDTV Profit after the announcement. Passenger vehicles, including British luxury carmaker Jaguar Land Rover, accounted for 79% of the company's Rs 3,41,544 crore revenue in FY23, while commercial vehicles contributed 21%.

For every share held in Tata Motors, investors will get one share each of the new listed entities.

"This is a part of the ongoing process that street has already identified the potential of the individual business," said Abhishek Gaoshinde, deputy vice presidente of research at Sharekhan told NDTV Profit. "Each business will stand on its own merit and provide sufficient flexibility to investors, ensuring that no business acts as a burden on others."

Ajay Srivastava, managing director at Dimensions Consulting believes this to be a great move and a good news for retail investor. "Once they spilt we will see the real value of the business. The real re-rating will happen in the PV vehicle space," he said.

Here's What Brokerages Have To Say

JPMorgan

JPMorgan has maintained an 'overweight' rating on the stock with a target price of Rs 1,000 apiece, implying an upside of 1.29%.

The research firm anticipates better-than-expected margin and free-cash-flow delivery at Jaguar Land Rover.

Global luxury OEMs are prioritising profitability over volumes, which should benefit Jaguar Land Rover as well.

Tata Motor's market share in Indian PVs has been resilient despite competitor launches. CV margins have hit double digits (as guided), and JP Morgan expects this trend to continue as the company focuses on mix and value growth instead of volume market share.

Furthermore, balance sheet deleveraging should reduce earnings per share volatility and lead to a potential re-rating.

This is another step in simplifying structure and creating value.

"We would seek more clarity on PV business synergies," the note said.

Investec

The research firm has a 'hold' rating on stock, with a target price of Rs 900 apiece, implying a downside of 8.8%.

The valuation of each business is valued separately, and the research firm values the CV business at 12x EV/Ebitda (Dec'26), implying a 20% premium to Ashok Leyland Ltd.

Investec does not expect a significant re-rating of the CV business from here on, especially as there is a fear of CV growth slowdown on the back of the downcycle and dedicated freight corridor coming online.

Nomura

The research firm has a 'buy' rating on the stock with a target price of Rs 1,057 apiece.

Tata Motor's PV business has more potential to create value over the next few years. Its PV business has seen a remarkable turnaround after 2020, with market share ramping up from mid-single digits to 13.5% as of 9MFY24.

"This, in our view, has been driven by its focus on safety, attractive design, and feature-rich vehicles," it said.

The CV industry may experience some more re-rating in the future as a result of its expanding market share and profitability.

There can be potential upside from success in e-Buses and e-LCVs, to which we do not assign any value currently.

Motilal Oswal Financial Services

Motilal Oswal Financial Services has downgraded Tata Motors' to 'neutral', with a target price of Rs 1,000 apiece.

While the demerger seems to be a step in the right direction, Motilal Oswal does not foresee any need to revisit our target price.

"Moreover, despite factoring in most of the positive triggers in our estimates, we get limited upside given the recent sharp run-up in the stock," it said.

In the India PV business, Motilal Oswal factored in 8.5% volume growth in FY25E/FY26E each after 4.5% growth in FY24E vs. management/industry growth guidance of low single digits in FY25.

In the India CV business, the research firm factors in 6% volume growth in FY25E/FY26E each after 1% volume decline in FY24E vs. management/industry growth guidance of near-term weakness in FY25.

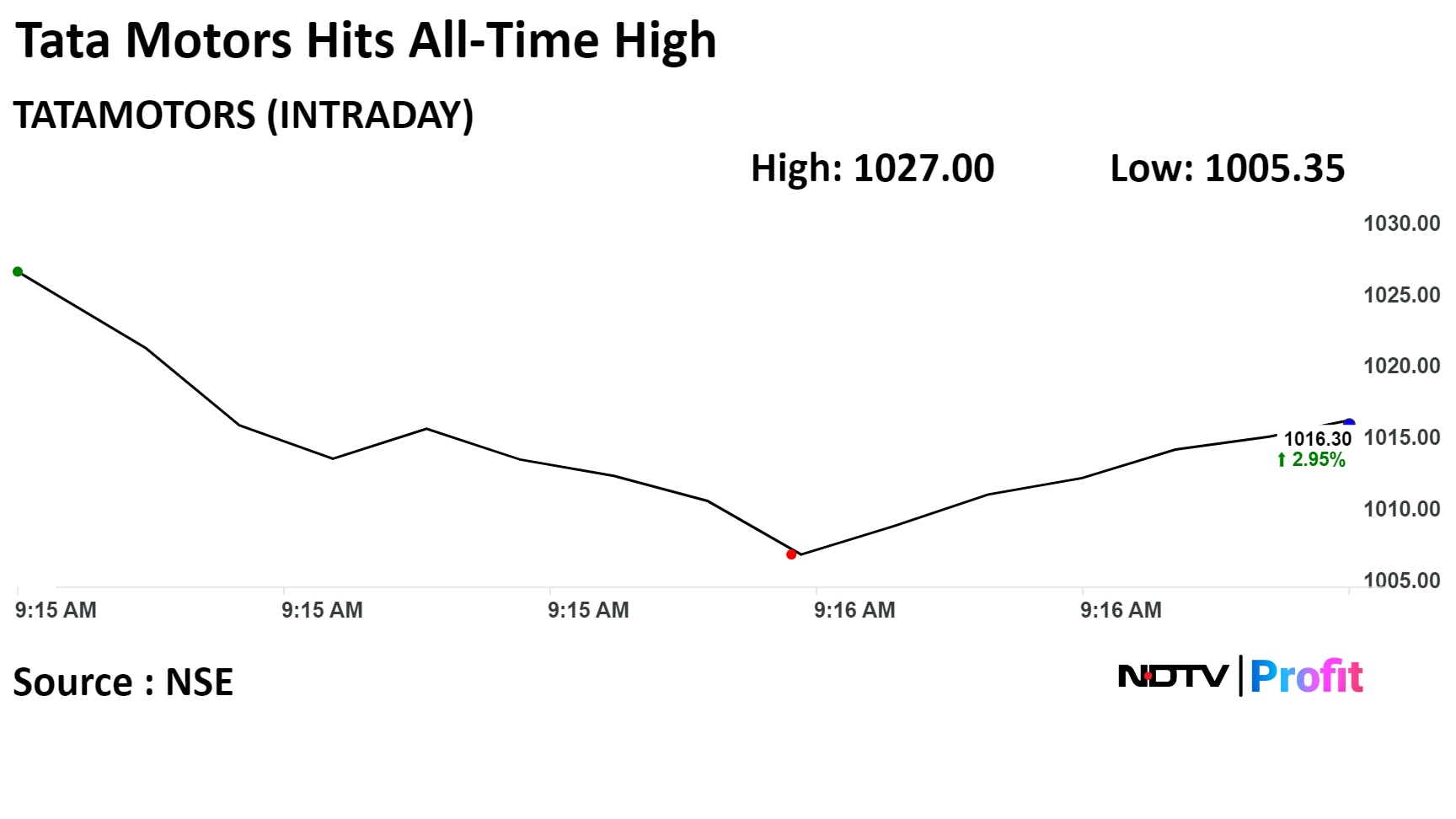

Shares of Tata Motors rose to as much as 4.03% to an all-time high of Rs 1,027 apiece on the NSE. The stock is trading 3.58% higher at Rs 1,022 per share, compared to a 0.24% decline in the benchmark Nifty 50 at 9:15 a.m.

The relative strength index was at 75, indicating that stock may be overbought.

Of the 34 analysts tracking the company, 26 maintain a 'buy', five recommend a 'hold,' and three suggest a 'sell', according to Bloomberg data. The average 12-month consensus price target implies a downside of 3.6%

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.