Country's foray into international debt markets may consist of little more than sound and fury, as the nation struggles to shed decades of trepidation about borrowing in foreign currencies.

A fanfare announcement in the July budget has been followed by the removal of the official driving the sale, objections from the prime minister's office, and finally an admission from Finance Minister Nirmala Sitharaman that no work has been done on the mooted $10 billion offering.

Country's first venture into the overseas bond market would shift part of its 7-trillion-rupee ($100 billion) borrowing abroad, and enable it tap a wider pool of funds. But fears that it may increase the nation's reliance on foreign borrowing has brought together an array of opponents arguing that currency volatility and elevated debt costs would ruin the country.

"India has a historical aversion to issuing in foreign currency, and this has been institutionalized over time," said Bryan Carter, London-based head of emerging-market debt at BNP Paribas Asset Management. Policymakers "see it as an unnecessary risk to open up to foreign capital flows and subject themselves to the mercy and whims of international investors."

The fear is that India may tread the well-worn paths of other developing countries such as Argentina and Greece who were saddled with sizable foreign borrowings after they failed to balance their budgets.

"The biggest benefit of the sale is the confidence that it signals to the world at large about India being confident of opening its economy," said Duvvuri Subbarao, a former governor of the Reserve Bank of India. "But the fear and concern that strike me are that this will become a thin end of the wedge. Once we see that it has become very successful, we might keep on doing it and get into pressure situations needlessly."

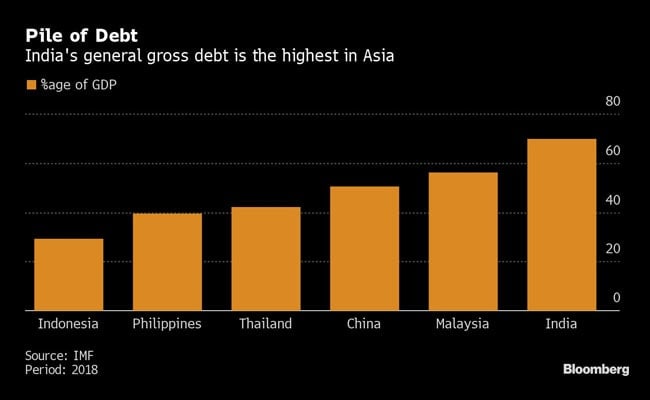

While India has enjoyed average annual growth of 7.5 per cent in the past decade, it has a combined fiscal deficit of about 8 per cent of gross domestic product. The federal government spends about 20% per cent of its annual budget servicing domestic debt.

All of that means former central bank officials and a key political ally of Prime Minister Narendra Modi have spent the past weeks criticizing the debt sale plan. Borrowing from overseas will not only increase the risk of higher inflation and currency volatility, but also boost debt costs on dollar bonds when the rupee weakens, they argued.

The rupee has depreciated in seven of the past 10 years.

Proponents for the sale point to a foreign-exchange buffer which is near a record $430 billion and a government which is widely perceived to be the most politically stable in three decades. Also, tight control over foreign inflows into onshore markets means India has fewer worries about capital flight than peers like Indonesia.

Additionally, country may have pricing power given the dearth of upcoming emerging-market issuance and the rising pile of negative-yielding debt worldwide.

"The scarcity of such an asset will likely result in demand that is multiples of the planned issuance amount," said Abbas Ameli-Renani, a portfolio manager for EM bonds at Amundi Asset Management in London.

According to estimates by QuantArt Market Solutions, India would need to offer 7.5 per cent interest on the overseas sale of rupee-denominated debt, an alternative that has been mooted. That compares with 2.7 per cent for US-dollar bonds, and yields of as low as 0.5 per cent for the euro and the yen.

Recent Samurai debt sales by Indonesia and the Philippines offered yields of 1.17 per cent and 0.6 per cent respectively, while their dollar-denominated debt was sold at 3.45 per cent and 3.78 per cent.

Once hedging costs are included though, a rupee-denominated debt sale would be cheaper, according to Samir Lodha, managing director and forex hedging strategist at QuantArt.

There are also worries that Asia's third-biggest economy may come under pressure during bouts of risk aversion, especially given the current backdrop of slowing global growth.

"India has refrained from a foreign issuance up till now" due to multi-fold risks involved, and the main one being foreign-exchange gyrations, said Rini Sen, an economist in Bengaluru at Australia & New Zealand Banking Group Ltd. "When markets are in turmoil, debt issued overseas will be worse hit than onshore bonds as the latter can be repaid by printing more domestic currency."

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.