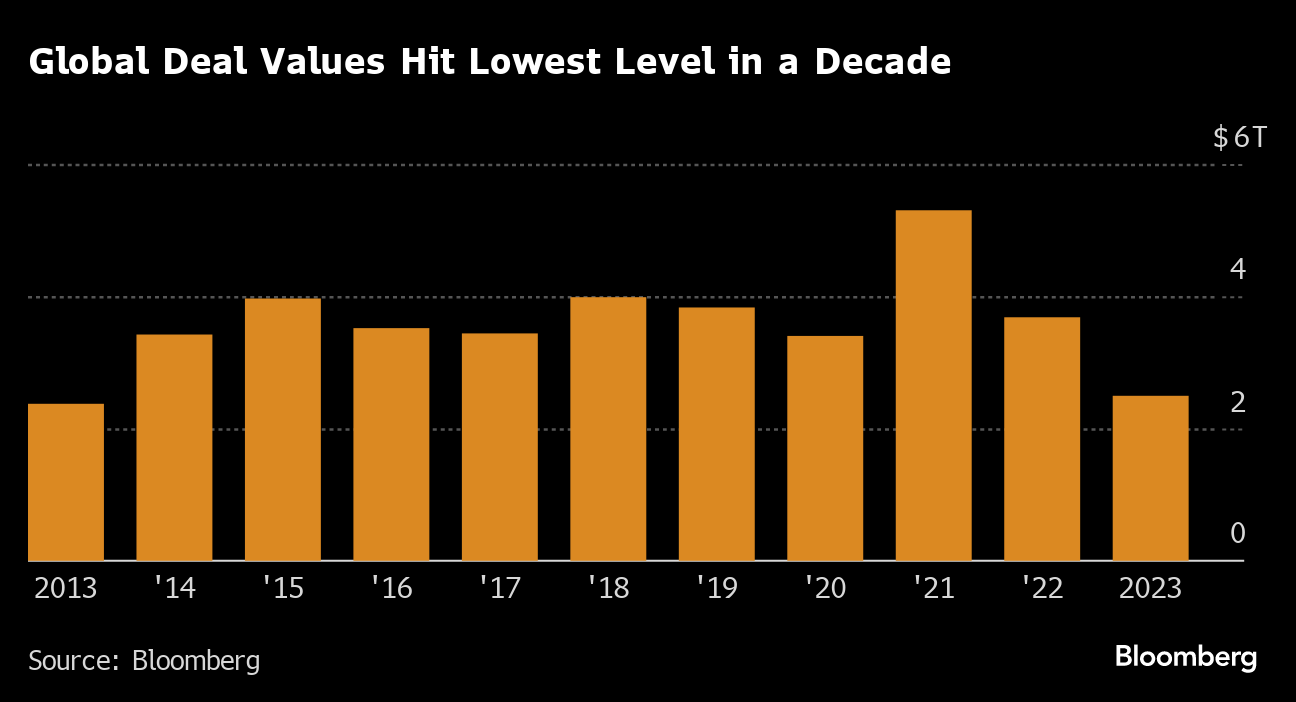

(Bloomberg) -- Dealmakers are coming to the end of their worst year for mergers and acquisitions in a decade, having seen hopes of any meaningful recovery choked off by reluctant lenders and geopolitical flare-ups.

The value of M&A and related transactions is down roughly a quarter this year to $2.7 trillion going into the holiday period, data compiled by Bloomberg show. That's the lowest annual total since 2013, which was also the last time deal values failed to hit $3 trillion in a calendar year, the data show.

The slump leaves investment bankers facing a bleak bonus season and more job cuts if things don't improve in 2024. And with interest rates and geopolitical tensions still running high, challenges to dealmaking remain, according to Jay Hofmann, co-head of M&A for North America at JPMorgan Chase & Co., who likened current conditions to those experienced during the dot-com crash in 2001.

“It has just been a lot harder to get things done this year and people have looked for reasons not to do deals. I don't really see that changing very much right now,” Hofmann said. “People aren't inclined to look past challenging issues to get deals through.”

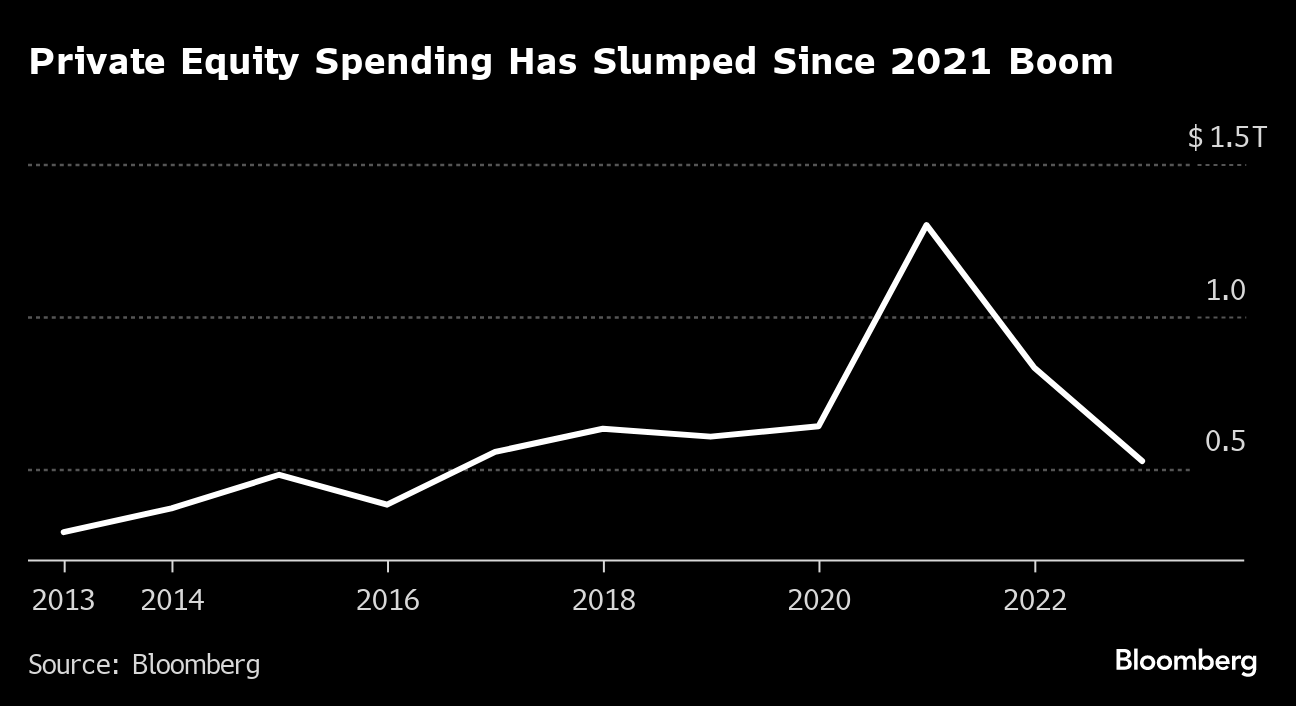

A lack of activity by private equity firms has again been one of the major drags on deal-flow in 2023. Buyout firms have spent 36% less on acquisitions this year, compared with 2022, amid struggles in securing debt financing for big deals and price disagreements with sellers — even when offering hefty premiums.

While some major transactions, including KKR & Co.'s long-trailed acquisition of Telecom Italia SpA for more than $20 billion and GTCR LLC's purchase of an $11.7 billion majority stake in payments firm Worldpay, have been announced, plenty of others have either stalled or run into hesitant sellers.

“Private equity activity will pick up meaningfully once we have more alignment between buyers and sellers on valuation. That is starting to happen now but we think it will take another six months or so,” said Majid Ishaq, co-head of UK at Rothschild & Co. “Buyout firms continue to look at take-private opportunities but they are difficult deals to execute, notwithstanding public market valuations having fallen, given that debt has become more expensive.”

Misplaced Optimism

There had been optimism about M&A moving into the final quarter of the year, on indications that markets were pricing in the end to rate-hiking cycles and banks were becoming more comfortable backing large buyouts. There was also a flurry of major deals across natural resources and health care, including the year's two biggest transactions: Exxon Mobil Corp.'s near $60 billion purchase of Pioneer Natural Resources Co. and Chevron Corp.'s acquisition of Hess Corp. for $53 billion.

But fresh uncertainty stemming from the war between Israel and Hamas dampened some of this new-found enthusiasm for dealmaking.

“I felt differently about the market every few weeks,” said William Aaronson, M&A partner at law firm Davis Polk & Wardwell LLP in New York. “A flurry of new deals did not always result in a ramp-up of sustained activity and processes tended to be more erratic.”

During the Covid-19 pandemic, company boards and private equity firms got out their check books and sent M&A values to record highs, driven in part by the belief that dealmaking in a downturn often yields the best results. This time around, there is less evidence that buyers are worried about letting bargains slip by, according to John Collins, global head of M&A at Morgan Stanley.

“Unlike the go-go market of 2021, there's not a great deal of FOMO (fear of missing out) among buyers,” Collins said. “Many buyers feel like they have a bit more time and are prepared to wait it out for things to stabilize further.”

How long they will have to wait for that stability will depend in no small part on the decisions of central bankers and the voting public in 2024.

Regarding interest rates, traders have been betting that the steepest global tightening cycle in a generation is over and monetary easing will begin from the middle of next year — something that will give buyers the confidence to start doing deals, said Melissa Sawyer, global head of law firm Sullivan & Cromwell LLP's M&A group.

“People are predicting that the central banks are not going to raise rates again so we seem to have reached the peak of the arc of rate increases,” Sawyer said. “As people have a sense that rates have stabilized, people will be ready to fire up the M&A engines again and get back to work.”

Election Year

On the geopolitics front, 2024 is offering a new source of potential turbulence from multiple leadership changes around the world. Starting with Taiwan in January and running through the high-stakes US presidential election in November, the year will bring 40 national votes.

“I'm not sure that there will be a takeoff point just because there will be a lot of geopolitical and domestic political debate discussion as the election year unfolds,” JPMorgan's Hofmann said. “I do think we can get back to kind of the run rate of activity levels seen in 2018 or 2019.”

Global deal values fell just shy of $4 billion in both of those years, Bloomberg-compiled data show.

Larry Grafstein, deputy chairman of the RBC Capital Markets global investment bank, is also optimistic. “2024, we think, should be a little better than 2023,” he said. “US presidential election years are usually pretty good years in the market.”

Read more: Familiar Names Throw Their Hats in 2024 IPO Market Revival Ring

--With assistance from Matthew Monks and Dinesh Nair.

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.