(Bloomberg) -- China's economy has leaned on industrial production to keep growing this year, and data in the coming week will provide clues on how strong that support remains.

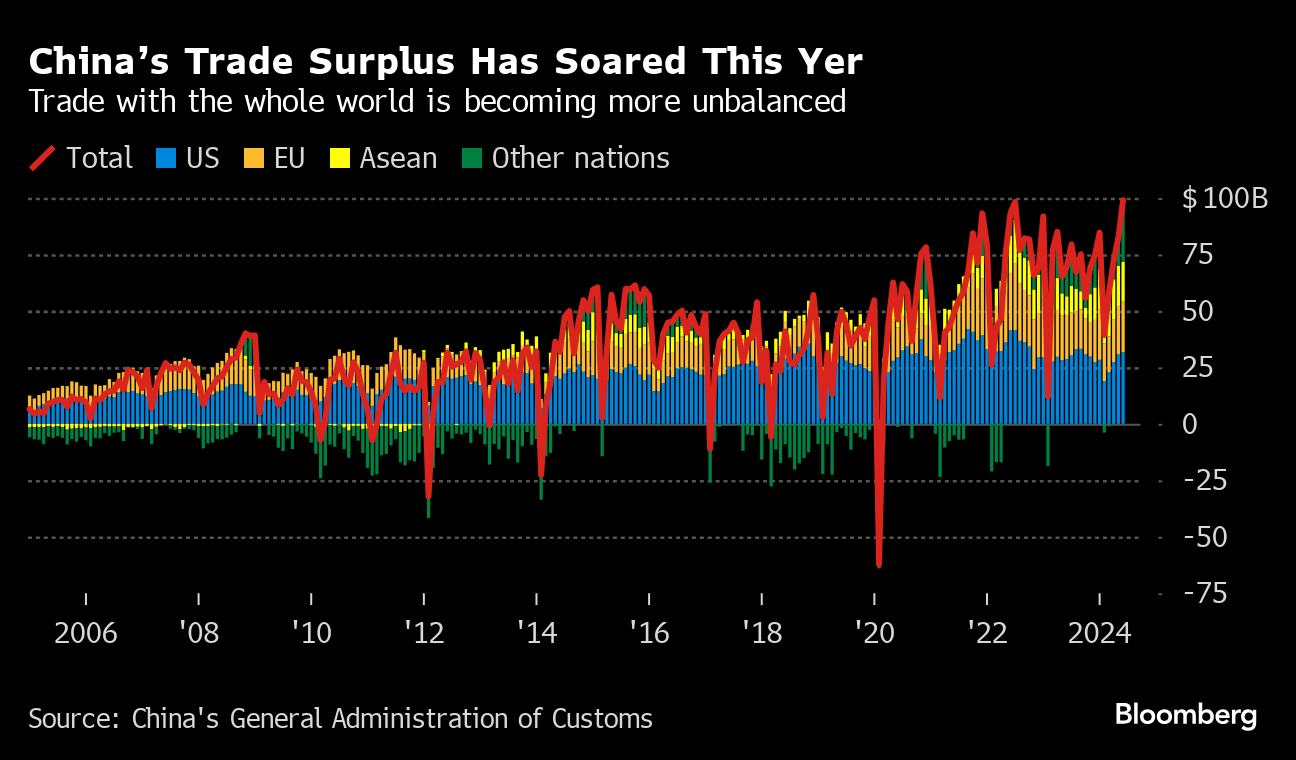

Export figures due on Wednesday may show some strengthening in July, underscoring how trade has been a rare bright spot.

Shipping volume from China's ports in the first half was 8.5% higher than 2023, with container freight rates surging by a factor of four, according to NCFI. Exports - from cars to steel to consumer goods - soared.

The picture looks less clear going forward. Manufacturing survey data has been shaky, with a decline in overall activity at factories. Most concerning was one measure — the Caixin index, with a relatively higher weighting of private firms and exporters — which contracted unexpectedly for the first time in nine months.

It's a worrying sign, especially after Chinese officials made clear in July that there would be limited aid to spur domestic consumption, a piece that's been visibly missing from the economic growth pie since the real estate bubble burst.

Exporters may also be seeing diminishing returns. While trade volumes are rising, Chinese companies aren't necessarily profiting, because they're also cutting prices. As a result, the total value of goods exports has barely budged this year, up only about 0.4%.

Later in the week, inflation figures are set to remain soft, with producer prices contracting for the 22nd straight month.

Analysts are taking note. Citi economists downgraded their forecast for this year's Chinese growth to 4.8% from 5%, while UBS economist Wang Tao now sees some downside risk to a 4.9% growth forecast.

What Bloomberg Economics Says:

“China's exports probably grew more quickly in July, aided by a favorable comparison with soft year-earlier figures. It won't be enough to drive faster GDP growth. So far, 3Q looks set to repeat the pattern of the prior quarter, when weak domestic spending outweighed export gains. For overall growth to meet the official 5% target in 2024, more stimulus is needed to stoke domestic demand.”

—For full analysis, click here

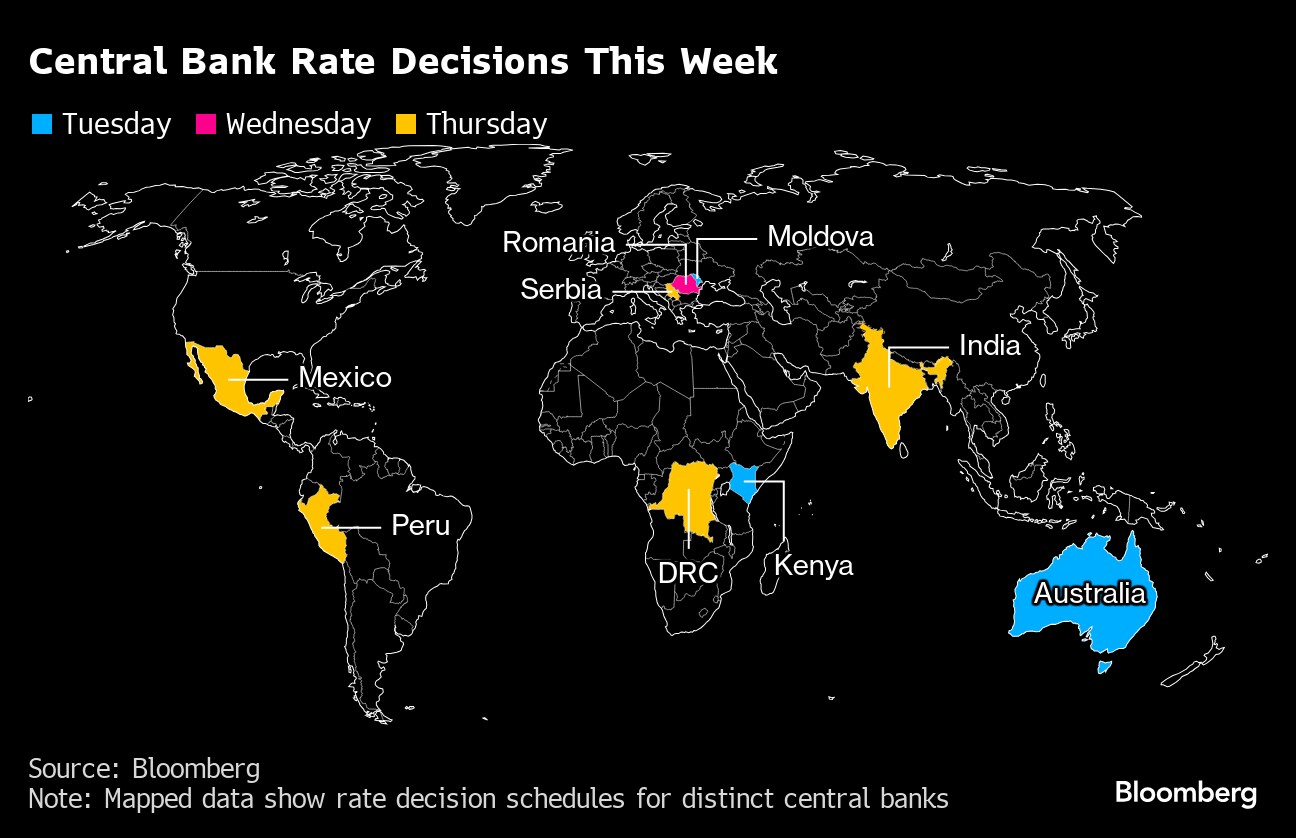

Elsewhere, US services activity likely grew just slightly in July, German data may show if the country's industrial slump is continuing, and central banks from Australia to India to Mexico will set interest rates.

Click here for what happened in the past week, and below is our wrap of what's coming up in the global economy.

US and Canada

Following Friday's monthly jobs report that showed a marked slowing in payroll growth and stoked recession concerns, the US economic calendar lightens up considerably.

The Institute for Supply Management will release its services index on Monday, and economists project modest growth in July.

Investors on Thursday will focus on weekly jobless claims data. Applications for jobless benefits in the week ended Aug. 3 are expected to have eased only slightly from an almost one-year high. The figures will provide clues into whether the labor market is at greater risk of backsliding.

The number of Federal Reserve officials making appearances is also sparse after the central bank left rates unchanged on Wednesday. But investors will hear from a few, including regional Fed bank presidents Mary Daly of San Francisco and Thomas Barkin of Richmond, both FOMC voters in 2024, and Austan Goolsbee of Chicago.

Meanwhile, a labor strike that would shut down six out of 10 of the busiest ports in the US just weeks before the presidential election is looking increasingly likely.

Further North, the Bank of Canada will release a summary of the deliberations that led to its July 24 cut in the policy rate to 4.5%, and its signal of further easing ahead. The document may provide insight into the likelihood of a third straight cut in September. Statistics Canada will also release its labor force survey for July, which is likely to show that job gains continue to lag explosive population growth.

- For more, read Bloomberg Economics' full Week Ahead for the US

Asia

In Asia, two key central banks are seen standing pat on policy, with attention focused on whether they soften their rhetoric.

The Reserve Bank of Australia is expected to hold its cash rate target at 4.35% on Tuesday after core inflation unexpectedly cooled in the second quarter and economic growth slowed more than expected in the first three months of 2024.

Two days later, the Reserve Bank of India is seen holding its benchmark rate at 6.5% while tweaking its language to convey a neutral pause instead of a hawkish hold, as more officials fret over growth prospects.

Elsewhere, Japan's cash earnings figures for June may show the swiftest pace of gains in a year as the fastest wage increases in more than 30 years start to kick in.

Trade figures are also due in the Philippines and Taiwan.

Second-quarter economic growth in the Philippines is projected to accelerate year on year while slowing to 1% versus the prior period, while the nation's July price gains may pick up after typhoons pushed food prices higher.

- For more, read Bloomberg Economics' full Week Ahead for Asia

Europe, Middle East, Africa

Germany will release key manufacturing-related data for three days in a row, starting on Tuesday with factory orders and then followed by exports and finally industrial production for June.

That latter measure is predicted by economists to have increased by 1% on the month, partially retracing a far bigger drop in May, when the level of output reached its lowest level since the first year of the pandemic.

- Read more: Euro Zone's Big Growth Laggard Has a Lot of Cheery Consumers

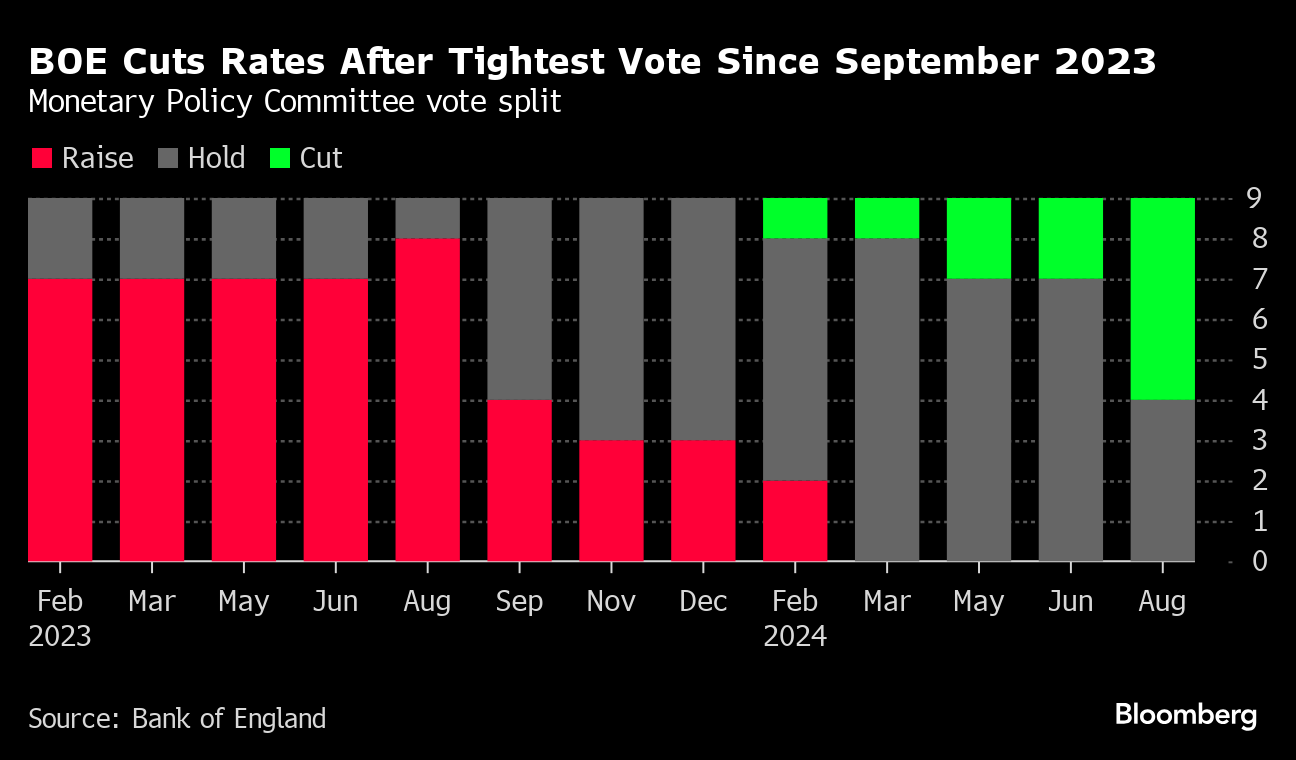

In the UK, where the Bank of England delivered a close-run rate cut on Thursday, the calendar will be notably quieter. The central bank is scheduled to release a quarterly report on its quantitative easing program on Tuesday.

Turning to Russia, data on Friday will likely show growth slowed in the second quarter from the prior three months. The economy remains overheated, however, with accelerating inflation forcing the central bank to raise rates sharply for the first time this year.

A number of consumer-price releases are scheduled:

- Turkish inflation on Monday may have slowed to 62% from 72% a month earlier. That would be another signal that the central bank has gotten a grip on prices and that Turkey is past the worst of its cost-of-living crisis.

- Egyptian authorities on Thursday will hope inflation slowed for a fifth straight month. The gauge fell to 27.5% in June, just before the country got a huge UAE- and IMF-led bailout that seems to have ended its foreign-exchange crisis.

- And on Friday in Norway, both the headline and underlying measures of inflation are predicted to show a slight uptick. The central bank has said it expects to keep its key rate at the highest since 2008 until some time in 2025.

- Final German and Italian inflation data for July will be published the same day.

Three key rate decisions are scheduled around the wider region this week:

- On Tuesday, Kenya's central bank may keep benchmark borrowing costs at 13% amid ongoing anti-government demonstrations that have shuttered businesses and led to renewed currency pressures after the government scrapped a plan to raise as much as 346 billion shillings ($2.7 billion) in taxes.

- The next day, Romania's central bank may consider a further rate cut, and officials will also debate and approve a quarterly inflation report to be presented by Governor Mugur Isarescu, probably on Friday.

- Serbia's central bank decision on Thursday may deliver more easing after two consecutive rate cuts, or else take a break to assess remaining price pressures.

- For more, read Bloomberg Economics' full Week Ahead for EMEA

Latin America

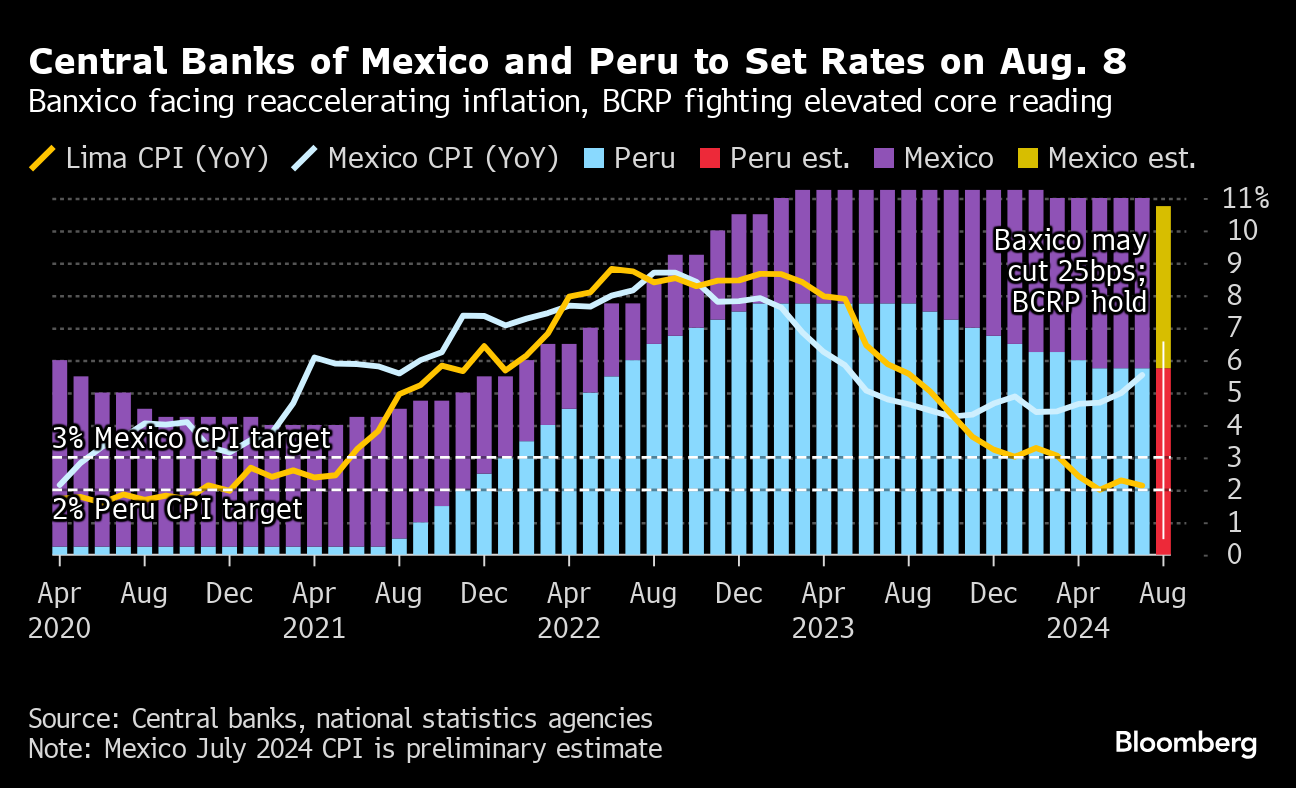

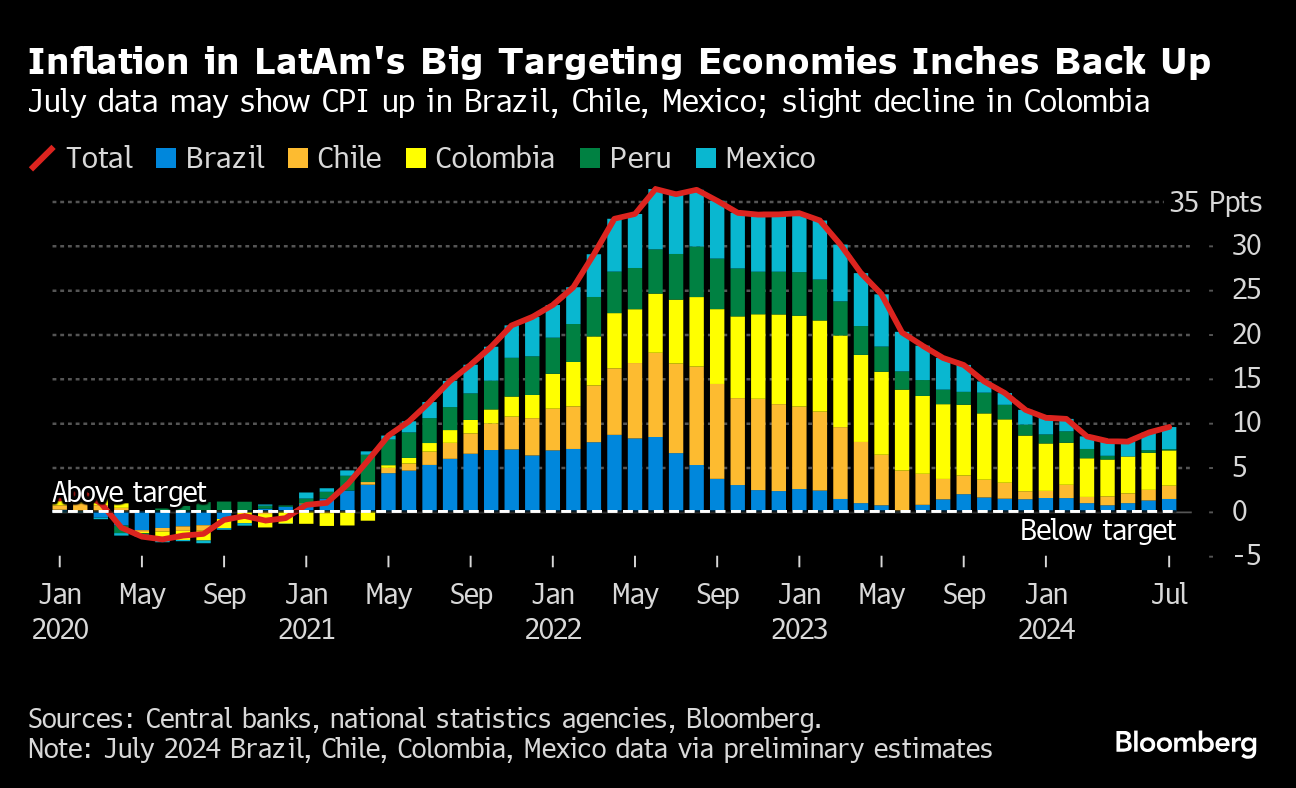

Disinflation has stalled across much of Latin America, with the exception of Colombia, sidelining or at least slowing central bank easing cycles.

Banco de Mexico and Banco Central de Reserva del Perú hold their August rate meetings on Thursday, and the consensus among analysts is Banxico will trim borrowing costs by a quarter point, to 10.75%, while BCRP holds at 5.75%.

Banco Central do Brasil on Tuesday posts minutes from its July 31 decision to keep the key rate at 10.5% for a second meeting. Analysts are slowly coming around to traders' thinking that a rate hike could be on the cards this year, though the post-decision statement provided no strong guidance to that effect.

Colombia's central bank also posts the minutes of its July 31 meeting, at which policymakers looked past gathering upside risks to inflation and delivered a fourth straight half-point cut, to 10.75%.

Consumer price data from four of Latin America's bigger economies will likely show a further increase last month above the 3% targets in Brazil, Mexico and Chile, while easing just below 7% in Colombia from 7.18% in June.

Mexico's July inflation data are released hours before Banxico winds up its rate meeting, and some analysts see an annual print of 5.5% or higher, up from 4.98% in June.

- For more, read Bloomberg Economics' full Week Ahead for Latin America

--With assistance from Brian Fowler, Robert Jameson, Laura Dhillon Kane, Piotr Skolimowski, Paul Wallace and Kira Zavyalova.

(Updates with US dockworkers in US, Canada section, Germany in EMEA section)

More stories like this are available on bloomberg.com

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.